Table of Contents >> Show >> Hide

- Why Inflation Changes the Whole Conversation

- Real Estate: Tangible, Powerful, and Not Nearly as Passive as It Sounds

- Stocks: The Growth Engine With the Emotional Roller Coaster Attached

- Bonds: The Calm, Useful, Occasionally Underappreciated Middle Child

- Quick Comparison: Real Estate vs. Stocks vs. Bonds vs. Inflation

- So Which One Wins?

- The Smarter Strategy: Build for the World You Actually Live In

- Real-World Experiences: What This Debate Looks Like in Everyday Life

- Conclusion

- SEO Metadata

Inflation is the financial party crasher nobody invited. It shows up quietly, eats your purchasing power, and somehow leaves your grocery bill looking like it just got a promotion. That is why comparing real estate, stocks, and bonds without talking about inflation is like reviewing umbrellas without mentioning rain. You can do it, sure, but you will miss the whole point.

For most investors, the real question is not, “Which asset is best?” It is, “Which asset gives me the best chance of growing wealth after inflation, while still letting me sleep at night?” That is where things get interesting. Real estate can build equity and produce income, but it is expensive, illiquid, and occasionally dramatic. Stocks have historically been strong long-term growth engines, but they can act like caffeinated squirrels in the short run. Bonds can provide stability and income, yet inflation can nibble away at their real value with surprising enthusiasm.

So let’s sort this out in plain English. Here is how real estate, stocks, and bonds compare when inflation enters the chat, what each asset does well, where each one struggles, and how real people can think about building a smarter, more durable portfolio.

Why Inflation Changes the Whole Conversation

Inflation is not an investment you buy, but it behaves like a force that affects every investment you own. If inflation rises, the same dollar buys less food, less gas, less housing, and fewer Friday-night takeout victories. That means your investments do not just need to grow. They need to grow faster than inflation if you want your money to maintain or increase its purchasing power.

This is why the phrase real return matters so much. A nominal return tells you how much your portfolio gained on paper. A real return tells you what that gain was worth after inflation took its cut. If your investment earns 5% but inflation runs at 3%, your real return is much less exciting than the headline number suggests. It is still a gain, but it is wearing a smaller cape.

Inflation also affects asset classes differently. Some investments can adapt because prices, rents, revenues, or earnings may rise over time. Others are more rigid. A bond paying fixed interest does not magically become more generous because eggs got expensive again. That is why comparing assets in an inflationary environment is really about flexibility, resilience, income, and time horizon.

Real Estate: Tangible, Powerful, and Not Nearly as Passive as It Sounds

Real estate has a natural appeal because it is physical. You can see it, improve it, rent it out, refinance it, or complain about the roof with confidence. That tangibility makes it feel safer than a ticker symbol dancing across a screen. And in some cases, real estate can be a useful inflation hedge. Property values and rents often rise over time, which can help owners keep pace with increasing prices.

There is also the leverage factor. A buyer who uses a fixed-rate mortgage may benefit if inflation and wages rise over the years while the monthly principal-and-interest payment stays relatively predictable. In that situation, inflation can actually make yesterday’s debt feel easier to carry tomorrow. It is one of the rare times inflation plays nice.

But real estate has plenty of catches. First, it is not just one thing. A primary residence, a rental duplex, a commercial property, and a REIT are all “real estate,” but they behave differently. Your home may build equity and offer stability, yet it is also a place to live, not just an investment. A rental can produce cash flow, but it comes with vacancies, repairs, taxes, insurance, and the occasional plumbing surprise timed perfectly for a holiday weekend.

Second, real estate is illiquid. You cannot sell half a kitchen when you need quick cash. Buying and selling property also involves transaction costs, closing costs, maintenance, and often higher borrowing costs than investors expect. Even a strong housing market does not erase the practical hassles. Real estate can build wealth, but it tends to do it in work boots, not loafers.

There is a tax angle too. Homeowners may benefit from favorable tax treatment when selling a primary residence if they meet the requirements, and investors may find deductions or depreciation useful in the right setup. Still, tax perks do not rescue a bad property bought at the wrong price with the wrong financing. A tax break is a side dish, not a miracle.

When Real Estate Shines

Real estate tends to look strongest when you want inflation sensitivity, income potential, and an asset you can actively manage. It can work well for patient investors who understand local markets, financing terms, tenant risk, and the true cost of ownership.

When Real Estate Struggles

It can disappoint when interest rates are high, affordability is poor, rent growth slows, or maintenance costs jump. It also struggles for investors who need liquidity, hate paperwork, or consider “surprise furnace replacement” a personal attack from the universe.

Stocks: The Growth Engine With the Emotional Roller Coaster Attached

Stocks represent ownership in businesses, and that matters in an inflationary world. Companies can sometimes respond to rising costs by increasing prices, improving efficiency, or expanding into more profitable markets. That adaptability is one reason stocks have historically been one of the better long-term tools for outpacing inflation.

In plain terms, stocks give you access to growth. Not guaranteed growth, of course. This is investing, not wizardry. But over long periods, a diversified stock portfolio has generally offered more upside than cash and more inflation-fighting potential than many fixed-income investments. For younger investors or anyone with a long time horizon, that makes stocks difficult to ignore.

Still, the short term can be messy. Stocks are highly liquid, which is wonderful when you need flexibility and terrible when you keep checking prices every eleven minutes. Inflation can hurt stocks too, especially when it is high enough to squeeze corporate margins, push interest rates upward, or scare consumers into cutting spending. Some sectors hold up better than others, but the overall market can still wobble.

That is why time horizon is everything. Stocks are not ideal if you need the money next year for a down payment, tuition bill, or retirement withdrawal plan. They are far better suited for goals that are years away, where short-term volatility becomes background noise instead of a full-body panic experience.

Another advantage is simplicity. Broad stock index funds and ETFs can offer diversification across many companies at relatively low cost. Compared with buying a rental property, owning a total-market fund involves dramatically less midnight stress. Nobody calls you because the S&P 500 has a leaking water heater.

When Stocks Shine

Stocks are strongest when the goal is long-term growth, inflation-beating potential, and liquidity. They are especially useful for investors who can stay invested through market swings and avoid making fear-based decisions.

When Stocks Struggle

They can struggle during recessions, inflation shocks, rising-rate periods, or anytime investor sentiment decides to become theatrical. The biggest risk is often not the asset itself but the investor reaction to volatility.

Bonds: The Calm, Useful, Occasionally Underappreciated Middle Child

Bonds rarely get the glamorous treatment. Nobody brags at dinner about a well-structured bond ladder with quite the same energy as a rental property or a hot stock pick. But bonds play a crucial role in a portfolio because they can provide income, lower volatility, and help fund near-term spending needs.

At their core, bonds are loans. You lend money to a government, municipality, or company, and in return you receive interest payments and the return of principal at maturity, assuming the issuer does not default. That structure makes bonds more predictable than stocks in many cases, especially high-quality bonds.

But bonds have a major inflation problem: many of them pay fixed income. If inflation rises, those future payments buy less in real terms. Rising inflation also often leads to rising interest rates, and when rates rise, existing bond prices typically fall. So while bonds can dampen volatility, they are not automatically safe from inflation pain.

This is where bond selection matters. Shorter-duration bonds generally carry less interest-rate risk than longer-duration bonds. High-quality bonds may offer stability when stocks fall. Treasury Inflation-Protected Securities, or TIPS, were designed specifically to help guard against inflation by adjusting principal based on inflation measures. They are not perfect, but they are one of the clearest bond tools for investors worried about purchasing power.

Bonds are especially valuable when your goal is capital preservation, income, or stability. A retiree drawing from a portfolio, for example, often benefits from having bonds available to fund spending during stock market downturns. That can reduce the need to sell stocks when they are temporarily down. In other words, bonds may not win the performance trophy every year, but they often help the whole team function better.

When Bonds Shine

Bonds tend to shine when investors need income, lower volatility, or a buffer against stock market turbulence. They are also helpful for short- and medium-term goals where preserving capital matters more than chasing maximum growth.

When Bonds Struggle

They struggle most when inflation is rising quickly, rates are climbing, or investors rely too heavily on long-duration bonds and expect them to do a job they were not built to do.

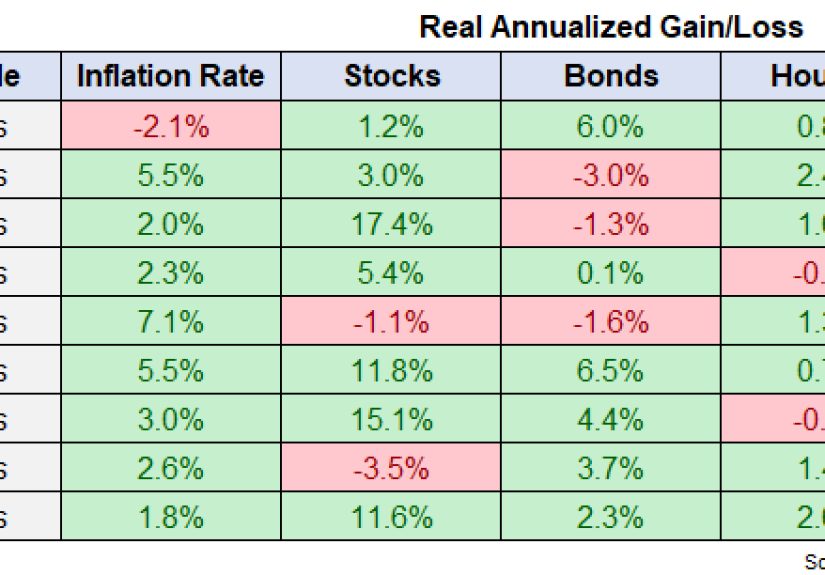

Quick Comparison: Real Estate vs. Stocks vs. Bonds vs. Inflation

| Asset | Main Strength | Main Weakness | Inflation Defense | Liquidity | Best For |

|---|---|---|---|---|---|

| Real Estate | Income, equity building, tangible asset | Illiquidity, high costs, management burden | Often decent over time, especially with rents and fixed-rate debt | Low | Patient investors who can handle complexity |

| Stocks | Long-term growth potential | High short-term volatility | Often strong over long periods | High | Long-term wealth building |

| Bonds | Income and stability | Inflation and interest-rate sensitivity | Usually weaker unless using inflation-linked bonds like TIPS | High to medium | Capital preservation and portfolio balance |

| Inflation | None for investors; it is the challenge to manage | Reduces purchasing power | Not an asset, just the villain of the story | Not applicable | A reminder to invest with real returns in mind |

So Which One Wins?

The annoying but honest answer is: it depends on the job. Stocks usually win the long-term growth contest. Bonds usually win the “please help me sleep during market chaos” contest. Real estate can win when you want income, leverage, and inflation sensitivity, but only if you understand the math and the maintenance. Inflation wins only when investors leave too much money sitting idle for too long.

If you are in your 20s, 30s, or 40s and investing for goals far down the road, stocks usually deserve a large role because growth matters most. If you are nearing retirement or already taking withdrawals, bonds often deserve more attention because stability becomes more valuable. If you have extra capital, patience, local market knowledge, and tolerance for complexity, real estate may make sense as part of a broader plan.

The real winner is often a diversified approach. Instead of trying to crown one asset class king of all seasons, many investors are better served by mixing growth assets, stabilizers, and inflation-aware tools. That might mean stocks for long-term appreciation, bonds for ballast, and real estate or REIT exposure for diversification and potential inflation resilience. Not flashy, perhaps, but effective beats flashy more often than the internet would like to admit.

The Smarter Strategy: Build for the World You Actually Live In

Good investing is not about predicting every twist in inflation, rates, housing, or the stock market. It is about building a portfolio that can handle multiple economic climates without requiring you to become a part-time prophet. That usually means matching assets to goals, keeping costs under control, diversifying thoughtfully, and rebalancing when your mix drifts too far from plan.

It also means understanding what each asset is supposed to do. Stocks are for growth. Bonds are for stability and income. Real estate can be for income, diversification, and inflation sensitivity. Cash is for flexibility, emergencies, and short-term needs, not for winning a decade-long race against inflation.

If inflation stays moderate, stocks and diversified portfolios may do fine. If inflation flares up, TIPS, carefully chosen real estate, and companies with pricing power may look more appealing. If growth slows and fear rises, high-quality bonds can regain their charm. A smart plan does not assume one environment forever. It prepares for several.

Real-World Experiences: What This Debate Looks Like in Everyday Life

Here is where the topic stops being theoretical and starts sounding like actual human behavior. Imagine three friends.

The first buys a rental property because “real estate always goes up.” At first, the numbers look solid. The rent helps cover the mortgage, and inflation nudges market rents higher. Then the property needs a new HVAC system, the tenant leaves, insurance rises, and the city adds fresh fees just for fun. This investor learns the classic real-estate lesson: a property can be a good investment and still be a lot of work. Real estate rewards discipline, patience, and local-market knowledge, but it absolutely does not reward fantasy math.

The second friend invests steadily in stock index funds through good markets, bad markets, weird markets, and those months when financial headlines seem written by caffeinated doomsday poets. This person experiences volatility up close. There are years when the account balance looks heroic and years when it looks mildly insulting. But by continuing to invest, reinvest dividends, and avoid panic selling, this investor learns a different lesson: stocks often do their best work slowly, then suddenly, and almost never on the emotional timeline people prefer.

The third friend loves bonds because they feel orderly. There is a rate, a maturity, and a nice sense of structure. For a while, bonds seem wonderfully civilized. Then inflation rises, rates move higher, and older bond prices fall. Suddenly, the “safe” part of the portfolio is not exactly fun anymore. But over time, this investor discovers that bonds were never meant to be exciting. Their purpose is to support the portfolio, provide income, and reduce the need to sell riskier assets at bad moments. That is less glamorous than chasing returns, but in retirement planning, boring can be beautiful.

There is also the homeowner experience, which sits somewhere between lifestyle and investing. Many people buy homes primarily for stability, family needs, or personal freedom, not because they are trying to outperform an index fund. Over time, they may build equity and benefit from appreciation, especially if they locked in a fixed-rate mortgage before rates rose. But they also learn that a house is not a spreadsheet. It has taxes, repairs, maintenance, and emotional gravity. It can be a wealth-building tool, yes, but it is also where the dishwasher chooses random Tuesdays to become philosophical and stop working.

Then there is the inflation experience itself. Almost everyone notices inflation first in daily life, not in the portfolio. Groceries cost more. Insurance premiums get bolder. Rent or housing costs creep up. That pressure often pushes people into one of two mistakes: hoarding cash because markets feel scary, or chasing whatever asset class recently looked invincible. Neither move is ideal. Cash loses ground over time when inflation persists, and performance chasing is just fear wearing running shoes.

The better experience, though less cinematic, is usually the investor who accepts that no single asset class will shine every year. They own stocks for growth, bonds for balance, maybe some real estate exposure for diversification, and they keep enough liquidity for real-life needs. They rebalance, stay patient, and remember that investing is less like winning a sprint and more like managing a long road trip with changing weather. The best vehicle is not the one that looks coolest in the driveway. It is the one that still gets you where you want to go when the road turns rough.

That is the heart of the real estate vs. stocks vs. bonds vs. inflation debate. It is not a cage match. It is a job interview. Each asset class has a role. The goal is not to pick the loudest candidate. The goal is to build a team that can work together while inflation keeps trying to eat everyone’s lunch.

Conclusion

Real estate, stocks, and bonds each respond to inflation in different ways, and none of them deserves a permanent crown. Stocks usually offer the strongest long-term growth potential. Bonds can stabilize a portfolio and support income needs, though inflation can weaken their real value. Real estate can provide income, leverage, and inflation sensitivity, but it is complex and expensive to own. For most people, the smartest move is not choosing one asset class forever. It is building a balanced plan that fits your goals, time horizon, and tolerance for risk. Inflation may be relentless, but a thoughtful portfolio can still make it work a lot harder for the win.