Table of Contents >> Show >> Hide

- Why communication has become the industry’s make-or-break skill

- The regulatory reality: clarity isn’t optional

- Where communication usually breaks down

- A practical playbook for more effective investment communication

- Start with the client’s question, not your product

- Translate risk into outcomes (and use ranges like an adult)

- Make fees and conflicts a first-class topic

- Fix performance communication: fair, comparable, and honest about what it is

- Use behavioral coaching language during volatility

- Write like a human: plain English, scannable layout, and fewer throat-clearing paragraphs

- Specific examples that upgrade your communication immediately

- Internal communication: the part clients never see but always feel

- How to measure whether your communication is actually working

- Conclusion: in a noisy world, being understood is a competitive advantage

- Real-World Experiences: What Works (and What Backfires)

In the investment business, you can build a brilliant portfolio and still lose a clientsimply because the client didn’t

understand what you built, why you built it, or what it was supposed to do when markets inevitably do their best impression

of a roller coaster. The problem isn’t that investors are “too emotional.” The problem is that the industry often communicates

like it’s trying to win a vocabulary contest instead of a trust contest.

And trust is the real currency here. Performance matters, of course. But performance is experienced through communication:

statements, reviews, emails, webinars, disclosures, social posts, quarterly letters, and the “quick call” that becomes a

forty-minute therapy session when the S&P has a bad week. Better communication doesn’t just make clients feel goodit can

reduce bad decisions, improve retention, lower compliance risk, and strengthen long-term outcomes.

Why communication has become the industry’s make-or-break skill

Investing has gotten more complex (more products, more data, more headlines, more “hot takes”), while attention spans have gotten

shorter. Meanwhile, the competition isn’t only the advisor down the streetit’s also an app that can rebalance a portfolio at

2 a.m. without asking anyone how they feel about inflation.

In that environment, communication isn’t a “soft skill.” It’s a core business system. If clients can’t clearly answer:

“What am I paying?”, “What risks am I taking?”, “What does success look like?”, and “What happens next if markets drop?”then the

relationship is fragile, no matter how polished the pitch deck is.

The regulatory reality: clarity isn’t optional

U.S. regulators have been nudging (and sometimes shoving) the industry toward clearer, more comparable information for years.

This isn’t just about being nice; it’s about being fair, accurate, and not misleadingespecially with retail investors.

Regulation Best Interest and Form CRS: the “plain talk” expectation

Regulation Best Interest (Reg BI) and Form CRS were designed to help retail investors better understand and compare services,

fees, and conflictsand make more informed choices about their relationships with firms.[1] The point is simple:

if your client needs a decoder ring to figure out how you’re compensated or what you actually do, something is broken.

Advertising, websites, and social media: communication that can become evidence

Modern marketing channels multiply the impact of every sentencegood and bad. Rules like the SEC’s investment adviser marketing

rule and FINRA’s communications rules set expectations around what firms can claim, how performance is presented, and how

testimonials/endorsements are handled. In plain English: if you communicate publicly, you’re doing regulated communication,

even if it’s “just a quick post.”[2][3]

Client statements, confirmations, and the everyday paperwork that drives trust

Investors experience the truth of your service through routine documents: confirmations, periodic statements, fee schedules,

and explanations of activity. When those documents are confusing, clients don’t just get annoyedthey get suspicious. Investor

education resources emphasize that investors should understand confirmations, statements, and fees because these documents

reveal what actually happened and what it cost.[4][5]

Where communication usually breaks down

1) Jargon replaces meaning

“Duration,” “tracking error,” “basis points,” “Sharpe,” “convexity,” “dispersion”these can be useful terms among professionals,

but they’re often used with clients as a substitute for explaining consequences. Jargon is the financial version of texting:

“Per my last email…” and then wondering why nobody likes you.

2) Numbers show up without context

Clients see performance percentages, but they want answers to human questions: “Does this change my retirement date?”

“Can I still afford my kid’s college?” “Should I stop checking my account at midnight?” If reports don’t connect returns to

goals, investors fill the gap with anxietyand anxiety loves dramatic headlines.

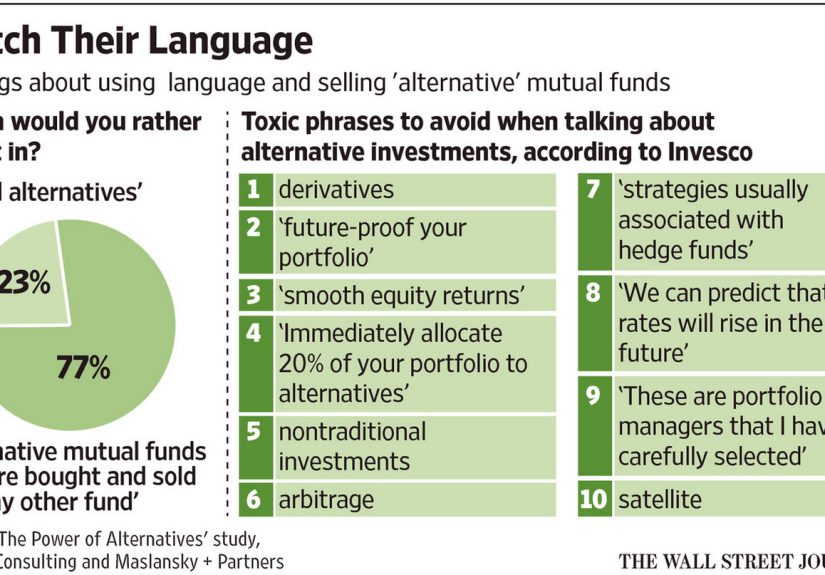

3) Fees and conflicts are disclosed but not understood

The industry often treats disclosure like a box to check instead of a conversation to complete. Yet investor-focused guidance

repeatedly stresses that fees and expenses can materially affect outcomes and should be understood upfront, with questions

encouraged.[5] Ethical standards and professional codes also emphasize disclosure and management of conflicts as a

foundational trust issuenot an appendix.[6][7]

4) Volatility communication is reactive, not proactive

Many firms wait until markets drop to talk about risk. That’s like buying smoke detectors after the kitchen fire. When clients

haven’t been prepared for normal drawdowns, a routine downturn feels like a personal betrayal.

A practical playbook for more effective investment communication

Start with the client’s question, not your product

People don’t wake up craving a “diversified multi-asset solution.” They wake up worried about whether they’re on track. Make

every communication answer one of these:

- What’s happening? (facts, not drama)

- Why is it happening? (simple drivers, no lecture)

- What does it mean for me? (goals-based impact)

- What are we doing about it? (plan-aligned actions)

Translate risk into outcomes (and use ranges like an adult)

Clients can understand “your portfolio could be down 12% in a rough year” more easily than “this strategy targets a volatility

of 9.” Use plain ranges, historical context, and scenario language. If you can’t describe downside in one or two clear

sentences, the risk story probably isn’t ready for a client.

Make fees and conflicts a first-class topic

Many investors underestimate how fees compound over time, which is why investor education resources emphasize asking direct

questions about total costs and comparing alternatives.[5] Don’t hide this in page 47. Put it early, repeat it

simply, and tie it to value:

Example wording (plain, direct):

- “All-in, you’ll pay about 1.10% per year for advice and the underlying investments. On a $500,000 portfolio, that’s roughly $5,500 a year, plus or minus market changes.”

- “If we recommend a product where we’re compensated differently, we’ll explain that conflict and why the recommendation still fits your goals.”

Professional standards and fiduciary frameworks emphasize acting in the client’s best interest and fully disclosing material

conflictscommunication is how that duty becomes real to a client, not just true on paper.[7]

Fix performance communication: fair, comparable, and honest about what it is

Performance reporting is where trust either grows or evaporates. Ethical performance presentation standards emphasize being

fair, accurate, and completeand performance presentation frameworks like GIPS focus on fair representation and full

disclosure.[8][9] In practice, that means:

- Show net-of-fees where relevant, and be explicit about what’s included.

- Explain benchmarks like you’re talking to a smart friend, not defending a dissertation.

- Discuss time periods honestly (1-year results are drama; 5–10 year context is reality).

- Separate “plan success” (funding goals) from “market success” (beating an index).

Use behavioral coaching language during volatility

Research and industry guidance often highlight that investor behaviorpanic selling, performance chasing, headline-driven

movescan create a return gap between what investments deliver and what investors actually earn. Morningstar’s “Mind the Gap”

work is frequently cited in this context, and investor behavior resources stress the real-world impact of poor timing.[10]

Advisors and firms also publish coaching approaches that focus on keeping clients aligned with long-term goals during market

stress.[11][12]

The best volatility communication usually has three ingredients:

- Empathy: “This feels scary. You’re not wrong to feel that way.”

- Perspective: “Drawdowns happen. The plan assumed this could occur.”

- Action: “Here’s what we’re doing now (and what we’re not doing).”

Example “market drop” message clients actually read:

“Your portfolio is down about 8% this quarter. That’s unpleasantand also within the normal range we planned for. The purpose

of your bond and cash positions is to keep your short-term spending secure so we don’t have to sell stocks at a bad time.

Unless your goals changed, our best move is to stay aligned with your plan. If you want, we can review your 12-month cash

needs and confirm your risk level still feels right.”

Write like a human: plain English, scannable layout, and fewer throat-clearing paragraphs

Plain-language guidance has long argued that clear writing improves investor relationships and reduces confusion and

frustration, and regulators have repeatedly emphasized understandable disclosure.[13][14] In practice:

- Use short sentences. Use active voice. Use headings that answer questions.

- Replace “utilize” with “use” (your clients will survive).

- Put key points up top, then details below.

- Use simple charts with one message per visual.

Specific examples that upgrade your communication immediately

A “what we do” explanation that doesn’t sound like fog

“We help you set goals, choose an investment mix that matches your timeline and comfort with risk, keep costs reasonable,

manage taxes when possible, and keep you from making big decisions based on scary headlines.”

A fee explanation that reduces unpleasant surprises

“You’ll see three main cost categories: the advisory fee, the internal fund expenses, and transaction or account fees if they

apply. We’ll review each one, and you’ll see them reflected in your statements and confirmations.”[4][5]

A quarterly performance paragraph that adds context

“Stocks fell this quarter as investors reassessed interest-rate expectations. Your portfolio declined too, but it declined less

than an all-stock portfolio because your mix includes bonds and cash for stability and spending needs. The plan is still funded

for your target retirement range, and we’re keeping the allocation aligned rather than chasing what just went up.”

A simple “if the market drops 20%” plan clients can remember

- We revisit your cash needs (so you’re not forced to sell at a low point).

- We check whether your allocation still fits your risk tolerance and timeline.

- We rebalance thoughtfully if it helps you stay aligned with the plan.

- We do not redesign your entire strategy based on one scary month.

Internal communication: the part clients never see but always feel

Clients can tell when a firm’s teams don’t communicate. The signs are subtle but loud: inconsistent answers, delays, paperwork

errors, and “I’ll have to check with someone” becoming the unofficial company slogan.

The fix isn’t more meetings; it’s clearer handoffs and shared language:

- One source of truth for fees, services, and disclosures (so marketing, advisors, and operations stop improvising).

- Approved language libraries for common topics (performance, risk, conflicts, volatility).

- Feedback loops from client-facing teams to product and operations (because confusion is data).

Effective internal communication also supports compliance. When rules govern public communications and advertising, clarity and

consistency across channels become risk controlsnot just brand preferences.[2][3]

How to measure whether your communication is actually working

“We sent a newsletter” is not a metric. Try measuring outcomes that indicate understanding and trust:

- Comprehension checks: In reviews, ask clients to summarize the plan in their own words (gently, not like a pop quiz).

- Behavior signals: Fewer panic-driven trades or “sell everything” requests during drawdowns.

- Service friction: Lower call volume about statements, fees, or basic account mechanics.

- Engagement quality: Fewer clicks, more time-on-page, more replies with thoughtful questions.

- Retention and referrals: Because people don’t recommend relationships that feel confusing.

Conclusion: in a noisy world, being understood is a competitive advantage

The investment business will always involve uncertainty. That’s not a bug; it’s the product. The industry’s job is to turn

uncertainty into a plan clients can followthrough clear explanations, honest expectations, and consistent communication that

respects both the client’s goals and the regulatory standards meant to protect them.

Better communication doesn’t mean watering down expertise. It means translating expertise into decisions clients can live with.

The firms that do this well won’t just reduce complaints and improve satisfactionthey’ll help investors stay the course, avoid

costly mistakes, and actually experience the benefits of long-term investing.

Real-World Experiences: What Works (and What Backfires)

The following are composite scenariospatterns commonly reported across advisors, investment teams, and client-service groups.

They’re not about one magical script; they’re about repeatable habits that make communication sturdier when markets and emotions

get wobbly.

Experience #1: “Panic Tuesday” and the power of a pre-written volatility message

A sharp market drop hits, and the inbox fills up with versions of the same message: “Should we sell?” The teams that struggle

tend to answer every note from scratch, with slightly different wording each time. That inconsistency becomes its own stress

multiplierclients compare responses, advisors second-guess themselves, and someone eventually promises something that sounds

like a guarantee (which is where compliance starts sweating).

The teams that handle it well usually have an approved, plain-English “volatility playbook” ready to go: a short explanation of

what happened, what the plan assumed, what actions are being taken (if any), and an invitation to talk through personal

circumstances. When clients receive a calm, consistent message early, many never make the panic call at all. The win isn’t

clevernessit’s preparedness.

Experience #2: The “fee surprise” that could have been a non-event

A client notices a fee on a statement and feels blindsided: “Why am I paying this?” Even if the fee was disclosed, surprise

damages trust because it feels like a secret. The best fix usually isn’t a technical explanationit’s a timeline.

Firms that reduce fee shock talk about costs in layers: at onboarding (big picture), after implementation (where to see it on a

statement), and in the first quarterly review (what it totaled and why it exists). They use simple dollar examples, not just

percentages, and they encourage questions before the client feels embarrassed for asking. When a client understands fees early,

they’re more likely to evaluate value fairly instead of emotionally.

Experience #3: A performance chart that accidentally taught the wrong lesson

Performance reports can unintentionally train clients to chase short-term resultsespecially when the biggest visual on the page

is a one-year return ranking. Some investors will treat the report like a scoreboard, not a plan checkpoint. The next step is

predictable: “Why aren’t we in the fund that did best last quarter?”

Strong communicators redesign the narrative: they lead with progress toward goals, then show performance in a longer time frame,

then explain what drove results and what’s expected from each piece of the portfolio. When clients learn that different assets

have different “jobs,” underperformance becomes less scandalous and more understandable. The result is fewer reactionary

portfolio changes and more plan-following behavior.

Experience #4: Marketing that sounded impressive… until it sounded misleading

A firm publishes a flashy case study on its websitebig numbers, strong claims, glowing praise. The intent is credibility, but

if the communication isn’t balanced and compliant, it can backfire. The issue isn’t that marketing is “bad.” The issue is that

marketing is regulated communication, and the audience is primed to interpret bold statements as promises.

The firms that do this right use plain explanations, clear assumptions, and careful performance language. They align marketing,

compliance, and advisor teams so the public message matches what a client hears in a review. Consistency is persuasive. It’s

also safer.

Across these experiences, the common theme is simple: clients don’t need less informationthey need information that is

organized, honest, and tied to decisions they can make. When communication improves, outcomes improve, because investors are

more likely to stick with the plan they actually understand.