Table of Contents >> Show >> Hide

- The Headline Isn’t Just “Valuations Up.” It’s “Access Down.”

- Why Higher Valuations and Lower Deal Counts Can Happen at the Same Time

- Seed Wasn’t Dead. It Was Just Meaner.

- Series A and B: Better Prices, Tougher Promotion

- The Real Market Story: A Bifurcation, Not a Broad Recovery

- What Founders Should Do in a Market Like This

- What Investors and LPs Should Watch

- So, Is VC “Back” in 2025?

- Field Notes From the 2025 Fundraising Trenches

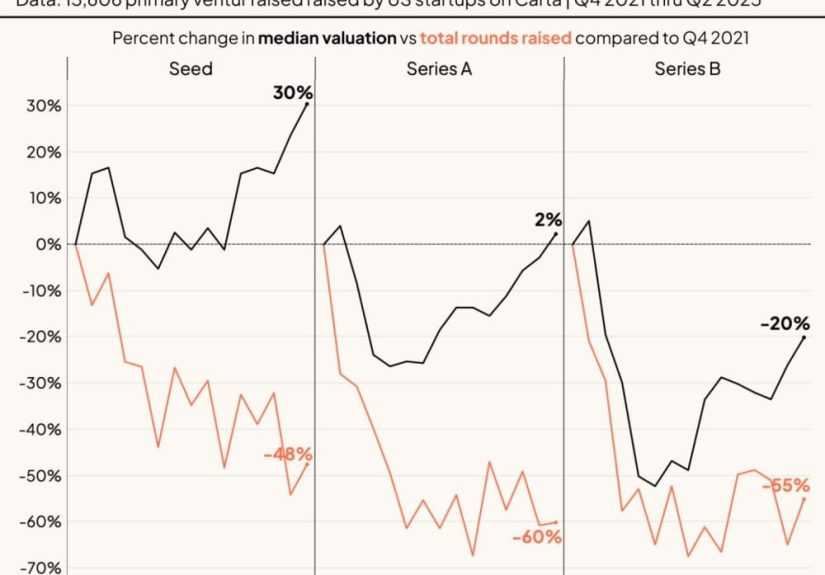

Venture capital in 2025 has entered its most venture-capital phase yet: the prices are higher, the guest list is shorter, and everyone keeps pretending this is perfectly normal while quietly refreshing their data dashboards like caffeinated raccoons. If Carta’s mid-2025 snapshot gave founders emotional whiplash, that is because it captured a market doing two opposite things at once. Valuations at the better end of the startup spectrum were up sharply, often by roughly 15% to 25% depending on stage. But actual deal counts? Down. Seed felt the squeeze. Series A was tighter. Series B was selective. Everywhere you looked, there were fewer checks being written.

On paper, that sounds contradictory. In practice, it makes perfect sense. Venture is not a calm, evenly distributed market where capital floats politely to all deserving founders. It is a power-law casino wearing a Patagonia vest. When investors believe a smaller number of startups will produce most of the returns, they do not spread money around. They crowd into the perceived winners, pay up for those companies, and ignore a huge chunk of the rest. That is exactly what 2025 looked like.

The Headline Isn’t Just “Valuations Up.” It’s “Access Down.”

The fastest way to misunderstand 2025 venture data is to look only at price. Yes, the better companies were getting better numbers. Carta’s data showed seed and Series A valuations climbing to record or near-record levels, even while total round counts declined. That is not a broad bull market. That is a narrow one. It is the venture version of a restaurant with a two-hour wait and half the tables removed.

In plain English, the market did not get easier. It got pickier. The companies that cleared the quality bar often received aggressive competition, better pricing, and sometimes faster decisions. The companies that did not clear that bar were left in the fundraising equivalent of airport limbo: lots of walking, bad snacks, and no clear departure time.

That is why the title matters so much. “Valuations are up” is true, but incomplete. “Deals are down everywhere” is the part that tells you how the market actually feels on the ground. Founders do not raise “median valuations.” They raise actual rounds, from actual investors, in actual meetings where someone says, “We love what you’re building, but we’re being very disciplined right now,” which is investor code for, “You are good, but not good enough for me to embarrass myself in Monday’s partner meeting.”

Why Higher Valuations and Lower Deal Counts Can Happen at the Same Time

1. Investors Are Concentrating Capital, Not Expanding It

The cleanest explanation is concentration. By 2025, more venture dollars were flowing into fewer companies, especially those tied to AI, infrastructure, developer tools, defense, robotics, and other sectors investors believed could produce outsized returns. When that happens, average and median valuations can rise even if the number of funded startups falls.

This is not new in spirit, but it was unusually obvious in 2025. The winners were not just winning. They were vacuuming up capital with industrial-strength suction. A small group of startups accounted for a wildly disproportionate share of dollars raised, while everyone else got the pleasure of hearing that “the market is still active for great companies.” Technically true. Emotionally unhelpful.

2. AI Changed the Math

AI did not just create a hot sector. It bent the entire venture market’s averages. If one bucket of companies commands more investor urgency, raises larger rounds, and justifies richer multiples because everyone thinks it might become the next platform layer, then that bucket can lift the headline numbers even while the rest of the market remains stubbornly selective.

That matters because many founders heard “venture is back” and assumed the recovery was broad. It was not. It was broad only in the way a flood is broad: very noticeable if you are in the water, much less helpful if you are standing three blocks away.

3. Fewer Deals Means Less Price Discovery

When fewer rounds happen, the companies that do raise carry more weight in the data. And if those companies are stronger, more efficient, or more AI-adjacent than average, valuations will look healthier than the lived experience of the whole market. In other words, the funded cohort becomes more elite, and the market stats start reflecting the survivors instead of the full applicant pool.

4. Founders Are Leaner, So the Best Ones Need Less Capital

Another subtle shift: some early-stage companies in 2025 were able to do more with smaller teams and better tooling. AI-assisted development, faster prototyping, and tighter operating discipline meant a startup could show more progress before raising. That strengthened the best fundraising stories. Ironically, needing less money often made those founders more valuable. Venture logic is weird like that. The founder who says, “We only need a modest round because we are already efficient,” often gets a warmer reception than the founder who says, “We need a huge round so we can become efficient later.”

Seed Wasn’t Dead. It Was Just Meaner.

Seed remained active in 2025, but the temperament changed. Investors still wanted early access to breakout companies, especially in AI and technical categories. At the same time, they cut back on the number of bets, lengthened diligence on borderline opportunities, and leaned harder into conviction-driven investing. Instead of writing three smaller checks, many firms would rather write one bigger check into the company they believed could dominate.

That creates a strange seed market. For the strongest founders, especially those with serious product velocity or unusually credible technical teams, fundraising can look surprisingly healthy. For everyone else, seed feels less like “let’s back a promising team” and more like “please provide enough evidence to satisfy a suspicious jury.”

This is also why so many seed founders in 2025 felt confused by headlines. They would read that valuations were holding or rising, then go out to market and find that investor response rates looked like an empty group chat. Both things could be true. Pricing improved for companies that made it into the winner’s circle. Access worsened for everyone trying to get past the velvet rope.

Series A and B: Better Prices, Tougher Promotion

Series A and Series B looked healthier on valuation charts than they felt in boardrooms. Carta’s numbers showed Series A valuations rising strongly, yet actual cash raised and deal activity remained under pressure. That tells a familiar story: firms were willing to pay more for the few companies that had undeniable traction, but they were not relaxing standards across the board.

The promotion problem became central. Seed companies were still being created, but graduating from seed to Series A remained tough. Series A companies were still being funded, but clearing the bar for growth capital demanded stronger evidence. Founders had to demonstrate not just growth, but quality of growth. Not just AI messaging, but AI leverage. Not just revenue, but efficiency. Not just a nice deck, but a business that could survive if the next round took longer than planned.

That is why 2025 felt less like the wild optimism of 2021 and more like a refined, selective market in which discipline finally got invited to the party. Venture had not become cheap. It had become choosy.

The Real Market Story: A Bifurcation, Not a Broad Recovery

If you need one word for the 2025 VC market, use bifurcation. The gap between top-tier startups and the rest widened. The gap between AI and non-AI widened. The gap between headline funding totals and broad deal activity widened. Even the gap between optimism and actual accessibility widened.

That is why broader market reports kept landing on the same conclusion from different angles. One set of data showed fewer deals. Another showed mega-rounds getting larger. Another showed AI taking an outsize share of funding. Another showed fund managers themselves having a harder time raising new vehicles. Add it all up, and the venture ecosystem looked less like a rising tide and more like a very powerful hose pointed at a few specific companies.

For founders, this means the wrong lesson is “money is flowing again, so I should raise because the window is open.” The better lesson is “money is flowing to companies that can prove they deserve it faster, more clearly, and more efficiently than last year.” The window is open, but it is not open for everybody. It is more like a nightclub door run by a bouncer with strong opinions about burn multiple.

What Founders Should Do in a Market Like This

Build for selection, not for average conditions

Do not model your fundraising plan around the median market. Model it around what gets you chosen. In a concentrated market, the reward goes to companies that make investor conviction easy. Tight narrative, fast product proof, efficient growth, and category clarity matter more when deal count is shrinking.

Raise before you “need” to, not after the market votes

Because time between rounds stretched in 2025, founders needed more runway and more realistic timing. The market was full of companies that assumed they could raise in six weeks and discovered that modern diligence moves at the speed of cautious optimism.

Use AI carefully in the pitch

Being AI-adjacent is not enough. Investors heard thousands of AI claims in 2025. The strongest pitches showed how AI made the product better, the team faster, or the economics stronger. The weakest pitches treated “AI” like glitter: applied heavily, difficult to clean up, and mostly distracting.

Expect better terms only if you earn them

The good news is that some deal terms remained more founder-friendly than many people expected. The bad news is that friendliness was not evenly distributed. In this market, good companies could still get solid outcomes. Average companies often got process, delay, and a crash course in selective enthusiasm.

What Investors and LPs Should Watch

For investors, 2025 raised an uncomfortable question: are higher valuations at the top a sign of recovery, or a sign that too much money is chasing too few names? The answer may be both. If AI truly creates a new platform cycle, the best companies could justify seemingly expensive entry prices. If not, some of those rounds may age like room-temperature sushi.

For LPs, the tension is just as sharp. Startup funding headlines improved, but venture fundraising remained difficult, distributions were still uneven, and managers had to prove they could source differentiated deals in a concentrated market. In other words, the startup market looked more optimistic than the fund market beneath it. That is a fancy way of saying the party was visible from outside, but many people still could not get in.

So, Is VC “Back” in 2025?

Yes and no. Yes, because capital was available, valuations improved, and exits began to show signs of life. No, because the recovery was uneven, concentrated, and far less forgiving than broad bull-market headlines suggest. Venture was back for excellence. It was back for AI. It was back for companies that could make a partner say, “We have to win this one.”

For everybody else, 2025 was a reminder that the market never really disappeared. It just became brutally selective. And that is the real lesson hiding behind the Carta numbers. Higher valuations did not mean easier fundraising. They meant the market was paying more for fewer opportunities. In venture, that is not a contradiction. That is the business model wearing nicer shoes.

Field Notes From the 2025 Fundraising Trenches

If you want to understand the lived experience of this market, stop staring only at the charts and listen to how founders described fundraising in 2025. The most common feeling was not panic. It was confusion. A founder could open the news, see that startup valuations were rising, hear that AI deals were massive, read that exits were thawing, and reasonably assume the fundraising climate had become friendlier. Then that same founder would send thirty investor emails and get six polite replies, three meetings, one serious follow-up, and a master class in how many different ways a venture firm can say, “Interesting, but not for us right now.”

That mismatch between headlines and reality shaped behavior. Teams became more deliberate. Founders spent more time tightening metrics before launching a process. Many pushed harder for early revenue, cleaner retention, or stronger product engagement before raising. Others realized the old playbook of “get a warm intro, build momentum, and let fear of missing out do the rest” was no longer reliable. Fear of missing out still existed in 2025, but mostly around the top few companies. For everyone else, fear of making a mediocre bet was stronger.

There was also a notable emotional split between categories. Founders building in hot sectors often experienced a strange version of speed dating with term sheets. If they had a credible technical story, real product momentum, and some AI leverage that felt authentic instead of decorative, investors could move fast. Not always, but fast enough to remind the rest of the market that capital was absolutely available. Meanwhile, founders outside those favored lanes often felt like they were pitching into weather. Not bad weather exactly, but the kind where the forecast keeps changing and everyone is advised to bring an umbrella just in case.

Operators adapted. They raised smaller rounds by choice. They extended runway. They treated capital efficiency as part of the product story rather than a sad finance appendix. Boards asked tougher questions. Investors dug deeper on what growth looked like without endless paid acquisition or giant hiring plans. Teams got leaner not only because they had to, but because the best of them discovered leaner could actually be better. In that sense, 2025 did something healthy: it punished fluff. The downside, of course, is that it also punished many perfectly decent companies that might have been fundable in a broader market.

The experience of 2025, then, was less “venture is dead” and more “venture now behaves like an honors program.” Admission still exists. The rewards are still real. But the acceptance rate feels lower, the standards are higher, and everybody is suddenly pretending they always loved discipline. Founders who understood that early had a better year. They told tighter stories, built stronger evidence, and raised with intention instead of hope. In a market where fewer deals get done, the best strategy is not to complain about selectivity. It is to become obviously selectable.