Table of Contents >> Show >> Hide

- A quick “what should I carry?” map

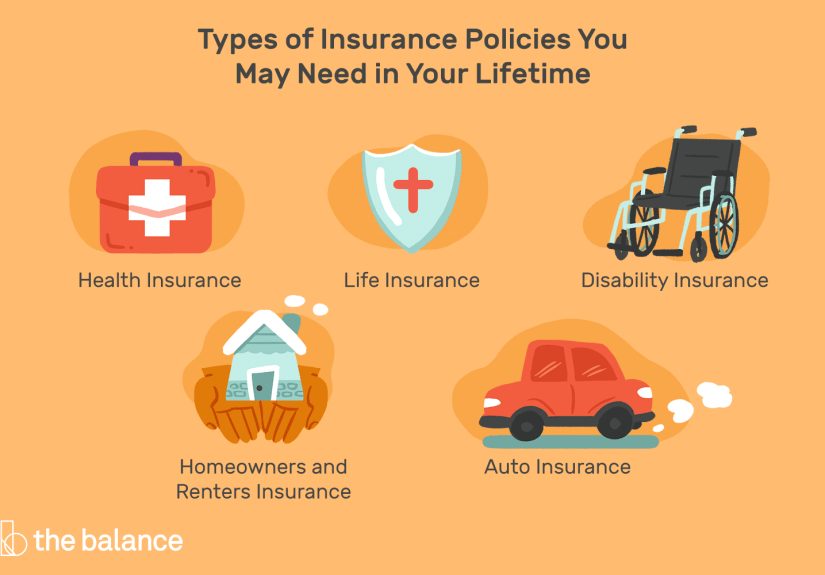

- 1) Health insurance: protects your body and your budget

- 2) Auto insurance: protects you from “one crash = one lawsuit”

- 3) Homeowners or renters insurance: your stuff + your liability

- 4) Life insurance: if someone would struggle financially without you

- 5) Disability insurance: protects the paycheck that pays for everything else

- 6) Umbrella liability insurance: extra protection when normal limits aren’t enough

- 7) Long-term care: plan now so “later you” doesn’t panic-buy options

- 8) “Depends on your life” insurance types

- How to build your insurance stack (without buying everything)

- Common mistakes (a.k.a. how people accidentally pay twice)

- Real-world experiences: what people learn after the fact (about )

- 1) The renter who thought the landlord’s policy covered everything

- 2) The “minimum coverage” car accident that didn’t stay minimal

- 3) The gig worker who discovered their income had no backup plan

- 4) The young family who got life insurance “later”… until later showed up early

- 5) The traveler who learned medical evacuation is its own category

- Final thoughts: buy protection, not panic

Insurance is basically a “financial seatbelt.” You hope you never need it, but if life slams the brakes,

you’ll be glad it’s there. The trick is not buying every policy with a glossy brochure and a smiling

mascotit’s building a smart set of coverage that protects your health, your income, your stuff, and your future.

This guide breaks down the most important types of insurance in the United States, who typically needs each one,

and how to pick coverage levels without paying for “deluxe anxiety.”

A quick “what should I carry?” map

Usually essential (for most adults)

- Health insurance (because hospitals don’t accept “good vibes” as payment)

- Auto insurance (if you drive)

- Homeowners or renters insurance (if you own or rent)

- Disability insurance (if you rely on your paycheck)

Often important (depending on family and finances)

- Life insurance (if someone depends on you financially)

- Umbrella liability insurance (if you have assets/income worth protecting)

- Long-term care planning (more relevant as you age)

Situational “add-ons”

- Flood/earthquake insurance (location-driven)

- Travel insurance (trip-driven)

- Pet insurance (pet + budget-driven)

- Business insurance (if you own a business or do substantial freelance work)

- Identity theft coverage (know what it really doesand doesn’tcover)

1) Health insurance: protects your body and your budget

Health insurance is the foundation because medical bills can become “life-changing” at record speed.

In the U.S., coverage may come from an employer plan, the Marketplace, Medicare, Medicaid, or other programs.

Key terms that actually matter

- Premium: what you pay each month to keep coverage active.

- Deductible: what you pay for covered services before your plan starts sharing costs (not always for preventive care).

- Copay/coinsurance: your share when you get care.

- Out-of-pocket maximum: the most you’ll pay in a year for covered in-network services (then the plan pays more).

Here’s a practical way to choose: don’t shop only by premium. Shop by your total annual risk:

premium + the most you could realistically pay out-of-pocket if the year goes sideways.

Example

If Plan A saves you $90/month ($1,080/year) but has a much higher out-of-pocket maximum, you might “win” in a healthy year

and lose badly in an unlucky one. If you have chronic meds, frequent care, or a smaller emergency fund,

a slightly higher premium with better cost-sharing can be cheaper in real life.

2) Auto insurance: protects you from “one crash = one lawsuit”

If you drive, auto insurance is usually required by your state and/or lender. But “required” and “adequate” are not the same.

Minimum limits can be far too low to cover a serious accident.

The building blocks

- Liability coverage (bodily injury and property damage): pays for injuries/damage you cause to others.

- Collision: helps pay to repair/replace your car after a crash (often with a deductible).

- Comprehensive: helps cover non-collision damage (theft, hail, falling objects, etc.).

- Uninsured/underinsured motorist: helps protect you if the other driver has little or no coverage.

- Medical payments/PIP (varies by state): helps with medical expenses after an accident.

How to pick limits without getting fancy

Start with liability. Ask: “If I accidentally hurt someone, do I have enough coverage to protect my savings and future income?”

Then consider collision/comprehensive based on your car’s value and whether you could replace it out of pocket.

If your car is financed or leased, the lender often requires collision and comprehensive.

Example

A driver with only state minimum liability hits a newer SUV and causes injuries. Repairs and medical costs can exceed minimum limits quickly.

If your policy limits run out, the remaining bill can become your problem.

3) Homeowners or renters insurance: your stuff + your liability

Whether you own or rent, this is one of the highest “value per dollar” coverages because it typically combines

property protection and liability protection.

Homeowners insurance (if you own)

Standard homeowners policies commonly include coverage for the structure, personal belongings, liability protection,

and additional living expenses (like hotel bills if your home becomes unlivable after a covered loss).

Renters insurance (if you rent)

Renters insurance can cover personal property (your belongings), liability (if someone is injured or you damage someone else’s property),

and additional living expenses after certain covered events. Your landlord’s insurance generally covers the buildingnot your belongings.

Don’t miss this: floods (and often earthquakes) are separate

Many homeowners and renters are surprised to learn that flood damage typically isn’t covered under standard homeowners/renters policies.

Flood coverage often requires a separate policy, such as through the National Flood Insurance Program (NFIP) or a private insurer.

4) Life insurance: if someone would struggle financially without you

Life insurance is less about you (sorry) and more about the people who would be left paying the bills if you died.

If no one depends on your income and you have no co-signed debts, you may not need much (or any) life insurance.

Term vs. permanent (simple version)

- Term life: coverage for a set number of years (often the most affordable way to get meaningful coverage).

- Permanent life (like whole life): can last longer and may build cash value, but typically costs more.

How much life insurance do you need?

A practical approach is to total the financial needs that would continue after your death: income replacement for a period of time,

paying off a mortgage, funding childcare/education, and covering final expenses.

If you’re thinking, “That’s a lot of math,” yesand that’s also why term coverage is so popular: it can cover the big stuff at a lower cost.

Example

Two parents with a mortgage and young kids often prioritize enough term coverage to replace income, pay the mortgage,

and cover childcare/education needs. A single renter with no dependents may only want enough to cover final expenses and small debts.

5) Disability insurance: protects the paycheck that pays for everything else

If you’re working, your ability to earn income is probably your biggest asset. Disability insurance helps replace a portion of income

if illness or injury prevents you from doing your job.

Short-term vs. long-term disability

- Short-term disability: may cover weeks to months (often offered through employers, varies widely).

- Long-term disability: can cover longer periods, sometimes years, depending on policy terms.

Important: disability insurance is not the same as Social Security disability

Social Security has a strict definition of disability and generally pays only for total disability, not partial or short-term disability.

That’s why many workers look at employer disability benefits or private coverage as a separate layer of protection.

What to look for

- Definition of disability (for example, “own occupation” vs. “any occupation” language)

- Benefit amount (often a percentage of income, up to a cap)

- Elimination period (how long you wait before benefits start)

- Benefit period (how long benefits can last)

6) Umbrella liability insurance: extra protection when normal limits aren’t enough

Umbrella insurance is like the “overflow buffer” for liability. It generally kicks in after you’ve reached the liability limits

on your auto/home/renters policy. It can also cover certain claims not covered by underlying policies (depending on terms),

such as some personal injury claims like libel or slander.

Who should consider it?

- Homeowners with meaningful equity

- Higher earners (future wages can be a target in lawsuits)

- People with teen drivers, frequent guests, pools/trampolines, or other higher-liability lifestyles

- Anyone who simply wants more liability protection at a relatively low cost compared to increasing limits everywhere

7) Long-term care: plan now so “later you” doesn’t panic-buy options

Long-term care is help with everyday activitiesbathing, dressing, eating, moving aroundprovided at home, in assisted living,

or in a nursing facility. Many people assume Medicare will cover long-term custodial care. Typically, it does not.

Options people use

- Self-funding: building savings specifically for potential care costs.

- Traditional long-term care insurance: coverage designed for long-term care needs.

- Hybrid policies: sometimes life insurance with long-term care riders (details vary widely).

- Medicaid planning: for those who may qualify based on income/assets (rules vary by state).

8) “Depends on your life” insurance types

Flood insurance (location-driven)

Flooding is common and can be financially brutal. Standard homeowners/renters policies typically exclude flood damage,

so you may need separate flood coverage. If you live in a flood-prone areaor even a “not usually, but sometimes” areaask about your options.

Travel insurance (trip-driven)

Travel insurance can include trip cancellation/interruption, travel medical coverage, and emergency medical evacuation.

It can be especially useful for expensive prepaid trips, international travel, cruises, or remote destinations where medical evacuation could be costly.

Always read exclusionstravel policies often have very specific “covered reasons.”

Pet insurance (pet + budget-driven)

Pet health insurance generally reimburses for covered veterinary care (depending on deductibles, reimbursement rates,

and limits). It can make big vet bills more manageable, but it’s not a magic wandpreexisting condition rules and exclusions matter.

Business insurance (if you own a business or freelance seriously)

Even a small side hustle can create liability. Common business coverages include general liability, professional liability,

commercial property coverage, and workers’ compensation (requirements vary). If you have clients, employees, inventory,

or deliver products/services, it’s worth a focused conversation with a licensed agent.

Identity theft coverage (know what you’re buying)

Identity theft “insurance” often doesn’t reimburse stolen money. It may help cover certain recovery-related costs and provide support services.

Many policies also won’t pay if the loss is already covered elsewhere. If you’re considering it, read the fine print with your eyebrows raised.

How to build your insurance stack (without buying everything)

- Start with legal and lender requirements (auto liability, homeowners for a mortgage, etc.).

- Protect catastrophic risks first: big medical bills, major liability lawsuits, loss of income.

- Match coverage to what you can’t afford to replace: income, housing, essential transportation, core possessions.

- Choose deductibles you can actually pay without using a credit card as a life raft.

- Set liability limits based on assets and risk, then consider umbrella coverage for extra protection.

- Review annually and after life changes (marriage, baby, home purchase, new car, new job, business launch).

Common mistakes (a.k.a. how people accidentally pay twice)

- Buying the minimum limits and hoping everyone you might hit is extremely forgiving and medically invincible.

- Calling it “full coverage” without knowing what it includes. (That phrase is more vibe than contract.)

- Ignoring disability insurance even though your paycheck funds your entire lifestyle.

- Not updating beneficiaries after major life events.

- Assuming water damage = flood coverage. Insurance definitions are picky, and water has many “personalities.”

- Underinsuring the home by confusing market value with rebuild cost.

Real-world experiences: what people learn after the fact (about )

Here are a few “this actually happens” scenarios that show why the right mix of insurance matters. Names are fictional,

but the lessons are painfully real.

1) The renter who thought the landlord’s policy covered everything

Maya rented a third-floor apartment and assumed the building’s insurance would cover her belongings if something happened.

Then a kitchen fire in a neighboring unit filled her place with smoke and water. The building got repairedbut her laptop,

clothes, and furniture were on her dime. The surprise wasn’t just the property loss; it was the temporary living costs.

Renters insurance would have helped replace belongings and covered certain extra living expenses while the unit was unlivable.

Her takeaway: “I was paying for streaming services I barely used, but not for the policy that would’ve saved me thousands.”

2) The “minimum coverage” car accident that didn’t stay minimal

Jordan carried the state minimum auto liability because it was the cheapest option and he was “a careful driver.”

One rainy day, he hydroplaned into another car, causing injuries and significant repairs. The total claim value exceeded his limits.

Even if you’re careful, roads and physics don’t always cooperate. His takeaway: minimum limits can be a legal checkbox,

not a financial shield. He later increased liability limits and added uninsured/underinsured motorist coverage because he realized

other drivers can be underinsured too.

3) The gig worker who discovered their income had no backup plan

Serena freelanced full-time. When she broke her wrist, the medical care was covered by her health plan, but her income stopped cold.

Bills didn’t. She had assumed disability insurance was only for “dangerous jobs,” but disability can happen from illness,

injury, or surgery recovery. Her takeaway: health insurance pays doctors; disability insurance helps pay rent.

She later set up an emergency fund and explored disability coverage designed for self-employed workers.

4) The young family who got life insurance “later”… until later showed up early

Chris and Dani had a new baby and a mortgage, and they kept saying they’d buy life insurance after “things calmed down.”

Spoiler: things never calm down. When Dani’s employer cut hours and benefits, they realized how exposed they were.

They chose term life coverage to protect the mortgage and provide income replacement for childcare and essentials.

Their takeaway: life insurance isn’t about predicting tragedy; it’s about protecting the people who would have to rebuild without you.

5) The traveler who learned medical evacuation is its own category

On an international trip, Luis needed urgent care far from major hospitals. His U.S. health plan had limited coverage overseas,

and the cost of getting transported to an appropriate facility was the real shock. He’d assumed “travel insurance” was just for lost luggage.

His takeaway: travel medical and emergency evacuation benefits can matter more than trip delay snacks.

Now he matches coverage to the tripdomestic weekend: maybe nothing; international adventure: definitely a closer look.

The big pattern across all these stories is simple: insurance works best when it covers the risks that would otherwise force you into debt,

drain your savings, or derail your life plans. The goal isn’t perfectionit’s resilience.

Final thoughts: buy protection, not panic

The “right” insurance mix is personal. But most people do well when they start with health insurance, auto (if they drive),

renters/homeowners, and disability coveragethen add life insurance if they have dependents, umbrella coverage as their assets and income grow,

and long-term care planning as they approach later decades.

When in doubt, ask a licensed agent to explain coverage in plain English, compare quotes apples-to-apples,

and read exclusions like you’re trying to beat a final boss.