Table of Contents >> Show >> Hide

- Introduction: Gold Is Beautiful, but My Portfolio Is Not a Jewelry Box

- Gold Has a Strong Reputationand It Earned Part of It

- The Main Reason I Don't Own Gold: It Does Not Produce Anything

- Gold Is Hard to Value Without Telling a Story

- The Inflation Hedge Argument Is Not as Clean as It Sounds

- Gold Can Be Volatile, Even When It Is Called “Safe”

- Physical Gold Comes With Real-World Friction

- Gold ETFs Are Easier, but They Still Do Not Solve My Core Problem

- Taxes Can Make Gold Less Attractive

- I Prefer Productive Assets Over Defensive Objects

- The Opportunity Cost Is Too High for Me

- But I Do Understand Why Some People Own Gold

- My Personal Experiences With Not Owning Gold

- Conclusion: Gold Can Shine Without Belonging in My Portfolio

Note: This article is written for educational publishing purposes and reflects a personal investing perspective, not individualized financial advice. It synthesizes real information commonly discussed by reputable U.S. financial sources, including investor education materials, market research firms, brokerage commentary, tax guidance, and long-term return data.

Introduction: Gold Is Beautiful, but My Portfolio Is Not a Jewelry Box

Gold has a talent for making people feel dramatic. Stocks have earnings calls. Bonds have yields. Real estate has tenants, roofs, and surprise plumbing bills. Gold, meanwhile, just sits there glowing like it knows a secret.

For centuries, gold has been treated as money, treasure, emergency insurance, inflation protection, and the ultimate “just in case civilization gets weird” asset. It has survived empires, wars, recessions, currency scares, and more than a few uncle-at-Thanksgiving investment speeches. So why don’t I own any gold?

The answer is not that gold is useless. It is not. Gold can help diversify a portfolio. It can perform well during periods of financial stress. It can protect purchasing power in certain environments. It can also make people feel calmer when markets look like a toddler got hold of a red marker.

But for my own financial plan, gold does not earn a permanent seat at the table. It produces no income, is difficult to value, can be expensive to store or trade, receives less favorable tax treatment in some cases, and often depends on someone else being more worried tomorrow than I am today. That is not my favorite investment thesis.

This article explains why I don’t own any gold, why many investors still like it, and why I prefer productive assets, broad diversification, cash reserves, and a strategy that does not require me to polish bullion in the basement like a dragon with Wi-Fi.

Gold Has a Strong Reputationand It Earned Part of It

Before criticizing gold, it is only fair to admit why people love it. Gold has a long history as a store of value. It is scarce, durable, globally recognized, and not directly tied to the promise of any single company or government. Unlike a stock certificate, a gold coin does not depend on a CEO making smart decisions. Unlike a bond, it does not require a borrower to pay you back. Unlike a trendy app, it will not be ruined by one bad software update.

Gold also tends to attract attention during uncertain times. When inflation rises, currencies weaken, banks wobble, wars escalate, or investors lose confidence, gold often becomes the financial equivalent of a flashlight in a power outage. People may not know exactly what comes next, but they want something tangible.

Central banks also hold gold as part of their reserves. That fact gives gold a certain dignity. If major institutions still keep it around, it is hard to argue that gold is just a shiny rock with excellent marketing. Gold has a role in the global financial system, and for some investors, a small allocation can provide psychological comfort and diversification.

Still, “gold has a role” is different from “I need to own it.” A fire extinguisher has a role too, but I do not invest 10% of my net worth in fire extinguishers.

The Main Reason I Don’t Own Gold: It Does Not Produce Anything

My biggest issue with gold is simple: it does not create cash flow. Gold does not pay dividends. It does not pay interest. It does not reinvest earnings. It does not invent new products, raise rents, build factories, or return capital to shareholders. It just exists.

That is not automatically bad. Sometimes “just existing” is useful. Emergency savings do the same thing. But when I invest for long-term growth, I prefer assets that have an internal engine. A profitable company can increase revenue, improve margins, pay dividends, buy back shares, and compound over time. A bond can pay interest. Real estate can generate rent. Even a savings account, humble little thing that it is, can pay a yield.

Gold’s return depends mostly on price appreciation. In plain English, I only make money if someone later pays more for it than I did. That can happen, and sometimes it happens spectacularly. But it feels less like owning a productive asset and more like making a long-term bet on fear, scarcity, inflation, or demand from future buyers.

Gold Is Hard to Value Without Telling a Story

Another reason I don’t own any gold is that valuing it is strangely slippery. With stocks, investors can study earnings, cash flow, margins, growth rates, debt, and valuation ratios. With bonds, they can calculate yield, duration, credit risk, and maturity. With real estate, they can compare rent, expenses, cap rates, and location.

Gold gives you fewer tools. There is no earnings report. No dividend policy. No management team. No coupon payment. No rent roll. To decide whether gold is cheap or expensive, investors often look at macro factors: inflation expectations, real interest rates, currency trends, geopolitical risk, central bank demand, ETF flows, mining supply, and investor sentiment.

Those factors matter, but they are hard to convert into a fair price. If gold rises 40%, is it overvalued or finally being properly valued? If it falls 25%, is it a bargain or a warning? Smart people can argue both sides, usually with charts impressive enough to make everyone else feel underdressed.

That uncertainty does not make gold bad. It just makes it less comfortable for my investment style. I like investments where I can explain the reason for owning them without needing a fog machine and a macroeconomic prophecy.

The Inflation Hedge Argument Is Not as Clean as It Sounds

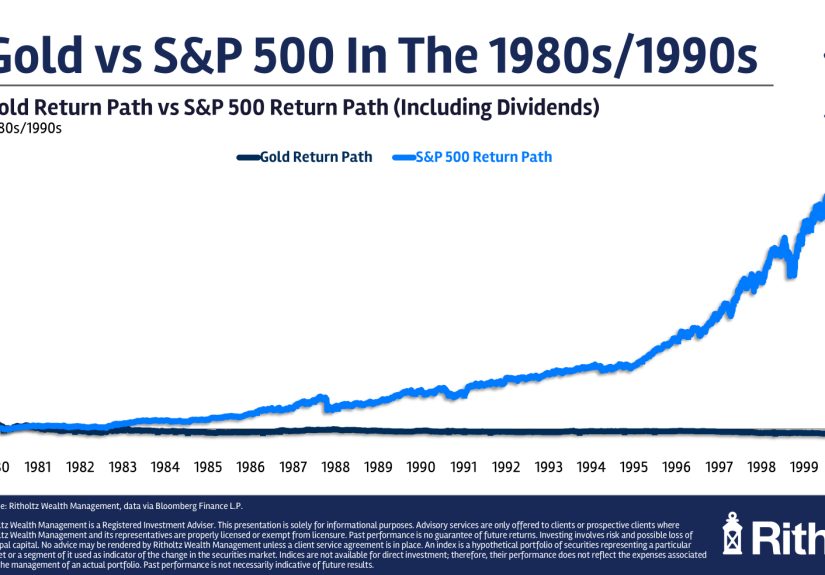

One of the most common reasons people buy gold is inflation protection. The logic sounds reasonable: if paper money loses purchasing power, gold should hold its value. Historically, gold has performed very well in some inflationary periods, especially when investors lost confidence in currency stability.

But gold is not a perfect inflation hedge. It can go up during inflation, but it can also disappoint. In some high-inflation years, gold has produced weak or even negative real returns. In 2022, for example, U.S. inflation was high, but gold did not deliver the kind of dramatic protection many people expected. Other factors, including interest rates and the strength of the U.S. dollar, also influenced its price.

For inflation protection, I prefer a broader toolkit: Treasury Inflation-Protected Securities, short-term cash reserves, diversified equities with pricing power, real assets through broad funds, and career income that can adjust over time. That combination is less glamorous than a gold bar, but it is also less dependent on one metal doing exactly what the brochure promised.

Gold Can Be Volatile, Even When It Is Called “Safe”

Gold is often described as a safe-haven asset, and in certain crises it has acted like one. But “safe haven” does not mean “safe from price swings.” Gold can be volatile. It can surge when investors panic, then drift sideways or fall when confidence returns. It can spend years underperforming stocks, bonds, or even boring cash.

This creates a behavioral problem. Many people buy gold after it has already gone up, usually because headlines have become scary. Then, when fear fades or other assets recover, gold may stop shining. The investor who bought for safety suddenly owns an asset that feels less like protection and more like a very expensive paperweight.

For a disciplined investor, a small gold allocation may work if it is rebalanced regularly. But that requires patience. It also requires buying when nobody is excited and selling when everyone is nervous. That sounds easy in a spreadsheet and much harder when cable news is breathing into a megaphone.

Physical Gold Comes With Real-World Friction

If I were going to own gold, physical gold would be the most emotionally satisfying version. There is something undeniably cool about holding a coin or bar. It feels solid. It feels ancient. It feels like the kind of thing a pirate would respect.

But physical gold also comes with practical headaches. You have to buy it from a trustworthy dealer. You may pay a premium above the spot price. You may face a spread when selling it. You have to store it securely. You may need insurance. If you keep it at home, you worry about theft. If you keep it in a safe deposit box, you introduce access limits and fees. If you tell too many people you own it, congratulations: you have converted your investment strategy into a security problem.

There is also the issue of liquidity. Yes, gold is globally recognized, but selling physical gold is not always as frictionless as clicking “sell” in a brokerage account. Depending on the product, dealer, condition, authenticity verification, and market demand, the process can take time and involve costs.

Gold ETFs Are Easier, but They Still Do Not Solve My Core Problem

Gold exchange-traded funds make ownership much simpler. Instead of storing coins or bars, investors can buy shares that track the price of gold. ETFs are generally more liquid than physical bullion, easier to trade, and more convenient for portfolio management.

If someone wants gold exposure, I understand why a low-cost gold ETF may be more practical than hiding coins in a sock drawer next to expired coupons. But ETFs do not change the basic nature of gold. The fund still tracks an asset that does not produce income. There may be expense ratios. There may be tracking differences. There may be tax considerations. And the investor is still relying on the price of gold rising or serving a diversification purpose.

For me, convenience does not fix the bigger concern: I would rather own assets that can compound from business activity, interest payments, or productive use.

Taxes Can Make Gold Less Attractive

Taxes are another reason I avoid gold. In the United States, physical precious metals are generally treated as collectibles for federal tax purposes. Long-term gains on collectibles can be taxed at a higher maximum rate than the long-term capital gains rate applied to many stocks and funds. Some physically backed gold ETFs may receive similar collectible-style tax treatment.

That does not mean gold is always tax-inefficient for every investor. Tax situations vary, retirement accounts have their own rules, and some gold-related investments are structured differently. But the potential for less favorable tax treatment is enough to make me pause.

When two investments already compete for a place in my portfolio, tax simplicity matters. Broad stock index funds are easy to understand, easy to hold, and often tax-efficient. Gold, by comparison, can make the tax conversation more complicated than I want it to be.

I Prefer Productive Assets Over Defensive Objects

The heart of my investing philosophy is ownership of productive assets. I want to own pieces of businesses, diversified funds, income-producing securities, and cash reserves for flexibility. That approach is not flashy. It will not impress anyone at a dinner party unless the dinner party is hosted by accountants. But it fits my goals.

Stocks represent ownership in companies that sell products, hire workers, build technology, improve logistics, serve customers, and generate profits. Bonds represent lending arrangements that pay income. Cash provides optionality. Real estate, when owned directly or indirectly, can generate rents and appreciate over time.

Gold does not fit neatly into that framework. It is more like insurance against certain bad outcomes. Insurance can be valuable, but I do not want too much of my financial life built around things going badly. I would rather build around growth, income, adaptability, and resilience.

The Opportunity Cost Is Too High for Me

Every dollar invested in gold is a dollar not invested somewhere else. That “somewhere else” matters. Over long periods, broad stock markets have historically rewarded investors for owning productive companies. Bonds have historically provided income and stability. Cash has provided liquidity. Gold has had impressive stretches, but it has also had long periods of underperformance.

When I think about portfolio construction, I ask: what job does this asset do, and is there another asset that does the job better?

For emergency liquidity, I prefer cash. For long-term growth, I prefer stock funds. For income and stability, I prefer bonds or bond funds. For inflation protection, I prefer a mix of TIPS, equities, cash management, and real-world earning power. For psychological comfort, I prefer a written financial plan and not checking markets 14 times before lunch.

Gold may help diversify, but in my portfolio, its job is already covered by other tools I understand better.

But I Do Understand Why Some People Own Gold

Not owning gold does not mean I think gold owners are wrong. Some investors have different goals, risk tolerances, cultural backgrounds, and financial concerns. A person who worries deeply about currency risk may value gold more than I do. Someone with a large portfolio may use gold as a small diversifier. A retiree may appreciate its crisis behavior. A collector may enjoy coins for reasons beyond investment returns.

There is also an emotional component that should not be dismissed. Money is not purely mathematical. If a small gold allocation helps someone stay calm and avoid panic-selling stocks during market crashes, that may have real value. The best portfolio is not always the one that looks perfect in theory. It is the one an investor can actually hold through ugly markets without turning into a financial raccoon.

My argument is not “gold is bad.” My argument is “gold is not necessary for me.”

My Personal Experiences With Not Owning Gold

I have had plenty of moments when gold looked tempting. Every time markets get shaky, gold starts appearing in headlines like a celebrity making a dramatic entrance. Friends talk about it. Analysts debate it. Advertisements make it sound as though buying gold is the only responsible adult decision left, somewhere between wearing sunscreen and changing the smoke alarm batteries.

The temptation usually arrives when uncertainty is high. Inflation rises, stocks fall, central banks make confusing speeches, or the economy feels fragile. At those moments, gold seems emotionally satisfying. It offers a simple story: the world is unstable, so own something permanent. That story is powerful. It is also incomplete.

My experience has taught me that the moment I most want to buy gold is often the moment I am reacting emotionally, not planning rationally. I am not thinking, “This asset improves my long-term expected return profile.” I am thinking, “The news is loud and I would like a shiny panic blanket.” That is not how I want to make investment decisions.

I have also watched people buy physical gold and discover the small annoyances later. One person is thrilled to own coins until they realize the dealer premium matters. Another likes the idea of storing gold at home until they start worrying about security. Someone else buys because prices are rising, then becomes frustrated when gold moves sideways while stocks recover. The metal did not betray them. Their expectations were just too magical.

Meanwhile, my own approach has become more boring and more peaceful. I keep emergency savings. I invest through diversified funds. I focus on asset allocation, expenses, taxes, and time horizon. I accept that markets will fall sometimes. I do not try to own every asset that might do well in every possible scenario. That last part is important. A portfolio cannot be a museum of every investment idea that ever sounded smart.

Not owning gold has also saved me from decision clutter. I do not have to decide whether to buy coins, bars, mining stocks, futures, or ETFs. I do not have to monitor premiums, storage costs, or collectible tax rules. I do not have to wonder whether gold is rising because inflation is coming, because real rates are falling, because central banks are buying, or because everyone collectively got nervous on a Tuesday.

Most importantly, avoiding gold keeps my strategy aligned with my personality. I like investments that are understandable, liquid, diversified, and tied to productive economic activity. I like knowing why I own something. I like boring systems that can run even when I am busy living my life. Gold may be timeless, but my attention span is not.

Could gold outperform my portfolio during certain periods? Absolutely. Could I regret not owning it during a major crisis? Maybe. But every investment choice involves trade-offs. I am comfortable missing some gold rallies in exchange for a cleaner, simpler, more growth-oriented plan. I do not need my portfolio to win every headline. I need it to serve my goals.

Conclusion: Gold Can Shine Without Belonging in My Portfolio

Gold is fascinating. It has history, beauty, scarcity, and global appeal. It can diversify a portfolio and may perform well when investors fear inflation, currency weakness, or geopolitical stress. For some people, a small gold allocation makes sense.

But I don’t own any gold because it does not match how I prefer to build wealth. It does not generate income. It is hard to value. It can be volatile. Physical ownership brings storage and security issues. ETFs add convenience but not productivity. Taxes may be less favorable than many investors expect. And the opportunity cost of holding gold instead of productive assets is too high for my personal plan.

Gold may be a store of value, but I want my portfolio to be more than a storage unit. I want it to be a machineimperfect, sometimes noisy, occasionally stressful, but designed to grow through earnings, income, innovation, and time. Gold can keep glowing on its own. I am happy admiring it from a distance.