Table of Contents >> Show >> Hide

- Why Record Highs Feel Like a Horror Movie (Starring Your Portfolio)

- Why All-Time Highs Are Normal (And Usually Expected)

- How Often Do All-Time Highs Actually Happen?

- What Usually Happens After a Market Hits a New High?

- The Real Reason All-Time Highs Are Scary: Drawdowns Are Normal Too

- When New Highs Are a Red Flag (And When They’re Just a Flag)

- So What Should You Do When Markets Hit All-Time Highs?

- Common “All-Time High” Mistakes (And the Simple Fixes)

- Conclusion: Scary + Normal = Investable

- of “All-Time High” Experiences (That Weirdly Keep Repeating)

- SEO Tags

The market at an all-time high is like walking into a party where everyone’s laughing a little too loudly.

You’re happy to be invited… but also wondering who’s about to spill something expensive on the carpet.

If you’ve ever stared at a chart hitting a fresh record and thought, “Cool cool cool… so THIS is the top,”

congratulations: your brain is working exactly as designed. Humans are great at spotting danger, terrible at

distinguishing “danger” from “new information.” The good news? Record highs aren’t a rare glitch in the system.

They’re a feature of a growing economy, compounding returns, and markets that spend a lot of their time climbing.

Let’s talk about why all-time highs feel spooky, why they’re completely normal, and what smart investors do when

the market looks like it’s trying to touch the sun.

Why Record Highs Feel Like a Horror Movie (Starring Your Portfolio)

1) The “I bought the top” boogeyman

Nothing haunts investors like the idea of being the person who shows up precisely one second before the trap door

opens. You don’t just fear losing moneyyou fear being wrong on the internet. That’s a special kind of pain.

2) Your brain treats new highs like cliff edges

Behavioral finance has a simple summary: we feel losses more intensely than gains. So when prices rise, we

don’t think “progress,” we think “how far can this fall?” Add nonstop headlines, hot takes, and doomscrolling,

and suddenly an all-time high feels less like achievement and more like a suspense soundtrack.

3) “All-time high” sounds like “all-time risky”

The phrase itself is a PR disaster. “All-time high” is just a timestamped fact: the price is higher than it’s ever been.

It does not automatically mean “overvalued,” “bubble,” or “imminent crash.” Sometimes it does! Often it doesn’t.

The label is about the past, not a prophecy about the future.

Why All-Time Highs Are Normal (And Usually Expected)

Markets have an upward bias over long periods

Over time, businesses innovate, improve productivity, reach new customers, and (ideally) grow earnings.

Stock prices don’t move in a straight line, but the long-run direction for diversified equity markets has historically

leaned upward because the underlying enginecorporate cash flowstends to expand.

On top of that, inflation exists. A dollar in the future often buys less than a dollar today, so “nominal” priceslike

index levelstend to rise over long horizons. Add reinvested dividends (often overlooked in casual chart-gazing),

and you’ve got a recipe for a lot of new highs over decades.

Indexes quietly “upgrade” themselves

Broad indexes aren’t museums. They evolve. Companies fall out, new leaders enter, and the index gradually tilts toward

what’s working in the economy. That doesn’t eliminate risk (hello, tech bubbles), but it helps explain why a diversified

index can keep making new highs even though individual companies come and go.

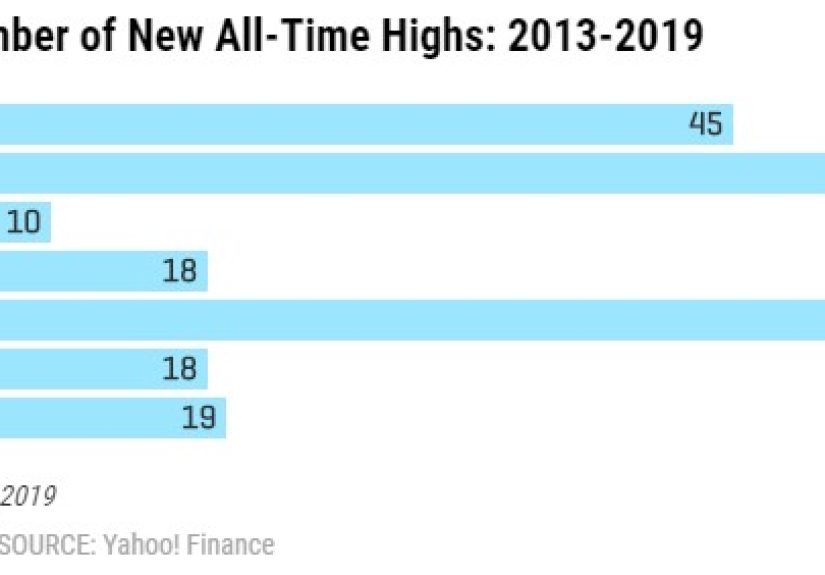

How Often Do All-Time Highs Actually Happen?

Here’s the part that calms people down: all-time highs are common. Not “daily,” but frequent enough that acting

surprised every time is like being shocked that your phone needs charging.

- In one strong recent stretch, U.S. equities logged 23 new all-time highs in a single quartermore than

one out of every three trading days. - For longer-term context, the historical average since 1950 has been closer to about five new all-time highs per quarter.

- In a typical year, new highs are still “under 10% of trading days”not constant, but absolutely part of normal market weather.

- And yes, markets can stack highs: one major U.S. index recorded dozens of record closes in a single year recently.

Records also arrive with headlines. Big round-number milestones (the kind that make TV anchors sit up straighter)

tend to show up when optimism is strongsometimes because earnings are solid, sometimes because investors are betting

hard on a new technology wave, sometimes because interest-rate expectations shift.

What Usually Happens After a Market Hits a New High?

This is the question behind the question. You’re not really asking “what is an all-time high?” You’re asking:

“If I invest now, am I about to regret having eyes?”

On average, returns after highs have been… normal

Long-term market history has a mildly annoying message: investing after record highs has often led to returns that look

a lot like investing at other times. In one large analysis of U.S. market data going back to 1950, the average

12-month return after an all-time high was essentially the same as other 12-month periodsmeaning the market did

not treat “record high” as a reliable sell signal.

Short-term vs. long-term: the nuance most hot takes skip

Another deep dive comparing forward returns found something surprising: over 1-, 3-, and 5-year windows, average returns

starting from an all-time high were slightly higher than starting from “non-high” days. But over much longer windows

(like 10 and 20 years), the “all-time high” entry points underperformed non-high entry points on average.

Two important notes so nobody tattoos the wrong takeaway on their investing plan:

- “Underperformed” doesn’t mean “lost money.” It means the average was lower versus other starting points.

That’s a very different claim than “don’t invest.” - Averages hide drama. Even if the average outcome is fine, the path can include ugly drawdowns, multi-year slumps,

and moments that make you question your hobbies.

The Real Reason All-Time Highs Are Scary: Drawdowns Are Normal Too

New highs and pullbacks are not opposites. They’re roommates.

A standard definition of a market correction is a decline of more than 10% (but less than 20%).

A bear market is typically 20% or more. Those drops feel like the sky is fallingespecially when they arrive right

after the market just set a record and you finally told your friend you were “getting into investing.”

But corrections aren’t rare events reserved for historic documentaries. They happen periodically, and they can happen

without a recession, without a crisis, and without the financial system turning into a flaming tumbleweed.

Sometimes the market simply gets ahead of itself and then… takes a breath.

When New Highs Are a Red Flag (And When They’re Just a Flag)

All-time high + stretched valuations can mean lower future returns

If valuations are elevated, future returns can be more muted. That doesn’t mean “panic sell.” It means

“calibrate expectations.” If the market has been ripping higher, it’s reasonable to expect more volatility and a

less magical ride.

Concentration risk is real

Sometimes records are driven by a narrow group of mega-companies. When a small slice of the index is doing most of the

heavy lifting, the headline “the market is up” can hide fragility underneath. A few stocks sneezing can make the whole

index catch a cold.

Hype cycles can create potholes

New technology waves can boost marketsand sometimes create “bubble” anxieties. Huge investment booms (think chips,

data centers, or whatever the next thing is) can lead to real productivity gains… or disappointment if profits don’t

show up on schedule. Markets price stories quickly. Cash flows take longer.

So What Should You Do When Markets Hit All-Time Highs?

Here’s the practical playbook. It’s not glamorous. It will not get you interviewed on TV. It does, however, tend to

keep you from making the same expensive mistake in six different outfits.

1) Match your money to your timeline

If you need the money in the next 1–3 years, it probably shouldn’t be riding the rollercoaster of stockswhether the

market is at an all-time high or an all-time “please make it stop.” Short timelines demand stability.

2) Stop asking “Is this the top?” and start asking “Is this my plan?”

A disciplined asset allocation (stocks, bonds, cash, and possibly diversifiers based on your goals) is designed for

moments like this. The market hitting a record doesn’t automatically change your need for growth, income, or liquidity.

3) Consider dollar-cost averaging if you’re nervous

If you have a lump sum and you’re terrified of investing it right before a drop, spreading purchases over time can

reduce regret. It’s not about maximizing returns; it’s about making the plan emotionally sustainable so you actually

stick with it.

4) Rebalance like a grown-up

All-time highs can push your portfolio out of alignment. If stocks ran up and now you’re taking more risk than you meant to,

rebalancing trims what’s grown and adds to what’s laggedan automatic “buy lower, sell higher” behavior without trying to

predict tomorrow.

5) Don’t confuse “being cautious” with “being in cash forever”

Waiting for the “perfect” moment is a classic trap. Research on market timing repeatedly finds that the cost of waiting

often outweighs the benefiteven if you somehow nail the timing once in a while. The market’s strongest days tend to cluster

around its worst days, and missing rebounds can do lasting damage to long-term results.

6) Diversify beyond the headline index

Diversification doesn’t guarantee profits and it doesn’t prevent losses, but it can reduce the odds that one narrow theme

(one sector, one country, one “Magnificent” something) becomes your entire personality and your entire risk.

Common “All-Time High” Mistakes (And the Simple Fixes)

- Mistake: Selling everything because “it can’t go higher.”

Fix: Keep your allocation; rebalance if needed; stay diversified. - Mistake: Buying whatever just went up the most because you “don’t want to miss out.”

Fix: Use a checklist: fundamentals, valuation, position size, and whether it fits your plan. - Mistake: Going all-in with borrowed money because records feel like guaranteed wins.

Fix: Avoid leverage you can’t survive. Markets can stay irrational longer than your margin can stay open. - Mistake: Refreshing your portfolio 37 times a day (rookie numbers, but still).

Fix: Set rules: monthly check-ins, automatic contributions, and a rebalancing schedule.

Conclusion: Scary + Normal = Investable

All-time highs are scary because they’re visible. They’re loud. They make your brain imagine gravity.

They’re also normal because markets are not designed to hover politely below yesterday’s ceiling. Over time, progress

tends to push prices upwardinterrupted by corrections, bear markets, and the occasional headline that makes you consider

taking up gardening instead.

The most reliable response to record highs isn’t a dramatic exit. It’s a boring plan executed consistently:

diversify, rebalance, invest with your timeline in mind, and resist the urge to turn “a new high” into “a new personality.”

Friendly reminder: This article is educational and not individualized investment advice. If you’re making major decisions,

consider talking with a qualified professional who can factor in your goals, taxes, and risk tolerance.

of “All-Time High” Experiences (That Weirdly Keep Repeating)

Experience #1: The 401(k) panic button. Someone sees their retirement account hit a personal record (yay!) and immediately

wants to “lock it in” (uh-oh). The impulse is understandable: it took monthsor yearsto get there, and the mind treats gains

like a fragile cake. But when you zoom out, the better move is usually to keep contributing and let the plan do its job.

Retirement investing is a long game, and long games involve lots of “highest ever” moments on the way up.

Experience #2: The lump-sum paralysis. A bonus, inheritance, or house sale creates a pile of cash. The market is at a record,

and suddenly that money feels like a hot potato. People often split into two camps: (a) invest all of it today and stress

about it tomorrow, or (b) wait for a crash that may or may not show up on their preferred schedule. A middle pathinvesting

on a scheduledoesn’t guarantee the best return, but it often guarantees something more valuable: you actually get invested.

Experience #3: The “I knew it!” moment after the first dip. If the market falls 3–5% shortly after hitting a high, investors

feel oddly validated. The brain loves being right. The problem is that tiny dips happen constantly and don’t prove anything

about the next year. Treating every wobble as confirmation that you should abandon your plan is like canceling your gym

membership because you got sore after your first workout. That soreness is not a scandal. It’s the process.

Experience #4: The temptation to chase the loudest story. Record highs often come with a narrative: AI, rate cuts, “the new era,”

“this time is different,” and so on. Some stories are real and transformative. Others are just marketing with better lighting.

The repeating pattern: investors concentrate too much in whatever is currently “obvious,” then discover that obvious trades

can reverse quickly. The antidote is position sizing, diversification, and remembering that even great themes can be overpriced.

Experience #5: The quietly powerful habit of rebalancing. This one is less dramatic but more effective. After a strong run,

someone notices their portfolio drifted from (say) 60/40 to 75/25. Rebalancing feels counterintuitive because it asks you

to trim what’s winning and add to what’s boring. Yet over time it can help manage risk and enforce discipline. It’s the closest

thing many investors have to an emotional seatbeltuncomfortable at first, appreciated during turbulence.

Experience #6: The realization that “normal” includes uncomfortable. People want a strategy that feels good every week.

Unfortunately, markets did not sign that contract. The most common “aha” moment is accepting that discomfort doesn’t mean

something is broken. It often means you’re participating in the risk that makes long-term growth possible.