Table of Contents >> Show >> Hide

- What Are Average Advisor Fees Charged by Brokerage Firms?

- Why Brokerage Advisor Fees Are Declining

- Typical Advisor Fee Ranges by Service Model

- Are Lower Advisor Fees Always Better?

- The Hidden Costs Investors Should Watch

- How Fee Compression Is Changing Advisor Value

- Examples: What Different Investors Might Pay

- How to Evaluate Advisor Fees Before You Sign

- Experience-Based Insights: What Investors Learn When Comparing Brokerage Advisor Fees

- Conclusion

Advisor fees used to feel like the financial-services version of a hotel resort fee: small-sounding, quietly expensive, and somehow still there after you thought you had paid for everything. Today, that story is changing. Across U.S. brokerage firms, digital advisory platforms, hybrid advisor programs, and traditional wealth-management shops, average advisor fees are under pressure. The old “1% of assets under management” rule is still alive, but it no longer sits alone at the grown-ups’ table.

The broad trend is clear: investors have more low-cost options, brokerages are competing harder, robo-advisors have reset expectations, and clients are asking sharper questions about what they actually receive for an advisory fee. Traditional human advisors still commonly charge around 0.25% to 1% or a little more of assets under management, while robo-advisors often sit closer to 0.25% to 0.50%. Cerulli also reports that asset-based fees now dominate advisor compensation, while commission-based revenue has fallen and is expected to decline further.

What Are Average Advisor Fees Charged by Brokerage Firms?

Most brokerage advisory fees fall into one of three buckets: traditional human advice, hybrid advice, and digital or automated portfolio management. A traditional full-service advisor may charge around 1% annually on managed assets, especially for smaller high-net-worth accounts. Hybrid programs often combine model portfolios, planning tools, and access to human advisors at lower rates. Digital advice, also known as robo-advisory service, usually charges the least because software does much of the portfolio construction, monitoring, and rebalancing.

For example, Vanguard’s Personal Advisor Select and Personal Advisor Wealth Management services use a tiered fee schedule with a maximum average advisory fee of 0.30%, not including fund expense ratios. Fidelity Go charges no advisory fee below $25,000 and 0.35% annually for balances of $25,000 or more, including access to coaching calls. Merrill Guided Investing charges 0.45% annually for its digital program and 0.85% for its advisor-assisted version.

Why Brokerage Advisor Fees Are Declining

1. Robo-Advisors Changed the Price Conversation

Robo-advisors did not eliminate human advisors, but they absolutely changed the way investors think about cost. Once investors saw professionally managed diversified portfolios offered for 0.25%, 0.30%, or 0.35%, paying 1% for basic portfolio allocation began to feel like paying steakhouse prices for a microwaved burrito.

Schwab Intelligent Portfolios, for instance, charges no advisory fee or commissions, although investors still pay indirect costs such as ETF expense ratios and the economic impact of Schwab’s cash allocation model. Morgan Stanley’s Core Portfolios lists an annual advisory fee of 0.30%, separate from underlying fund expenses. These examples show how major brokerage brands now offer low-cost automated or semi-automated advisory choices alongside higher-touch wealth management.

2. Investors Can Compare Fees More Easily

Twenty years ago, many investors did not know whether 1.25% was expensive, normal, or just a mysterious number wearing a suit. Now, fee schedules are easier to find. Brokerage websites, Form CRS documents, SEC brochures, financial media, and comparison tools have made advisory pricing far more transparent. That transparency pressures firms to justify higher fees with better planning, tax strategy, estate coordination, behavioral coaching, or specialized investment management.

The SEC warns that even small fees can significantly affect long-term portfolio value, especially when compounded over decades. That message has become mainstream. Investors increasingly understand that a 1% annual advisory fee is not “just one little percent.” On a $1 million account, it is $10,000 per year before fund expenses, trading costs, or other charges.

3. Brokerages Are Fighting for Mass-Affluent Clients

The mass-affluent investorsomeone with meaningful savings but not necessarily private-bank-level wealthis now a prized client. Big brokerages want these investors early, before they inherit money, sell businesses, roll over 401(k)s, or become the kind of people who use “tax-loss harvesting” in casual conversation.

To win them, firms offer lower minimums and lower advisory fees. J.P. Morgan’s public pricing page lists maximum advisory fees of 1.45% for several advisory programs, but also describes online investing as a low-cost option and shows $0 online stock and ETF trades through Chase.com. Fidelity’s managed account pricing shows ranges from 0.20% to 0.49% for Strategic Disciplines and 0.50% to 1.04% for Wealth Services, based on large minimums. The market is no longer one-size-fits-all; it is a menu.

Typical Advisor Fee Ranges by Service Model

Traditional Human Advisor: About 0.75% to 1.25%

Traditional advisory relationships still commonly revolve around assets under management, or AUM. The advisor manages the portfolio and may also provide retirement planning, tax-aware withdrawal strategies, insurance reviews, estate-planning coordination, and emotional support when the market behaves like a caffeinated raccoon.

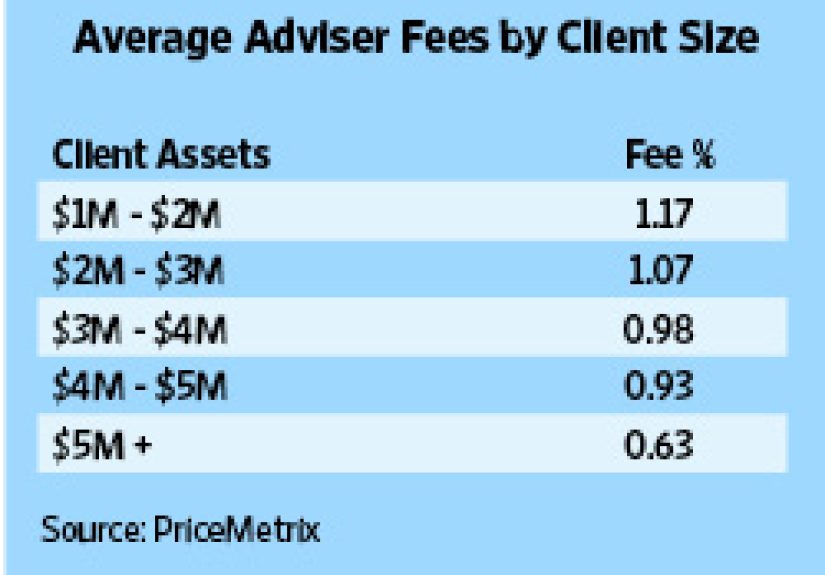

A 1% AUM fee remains a familiar benchmark, but many advisors use breakpoints. NerdWallet gives an example of a tiered schedule where the first $1.5 million is billed at 1.00%, the next $1.5 million at 0.80%, the next $2 million at 0.60%, and assets above $5 million at 0.50%. Under that example, a $3 million client would pay $27,000 per year, or an effective rate below 1%.

Hybrid Advisor: About 0.30% to 0.85%

Hybrid advice is the middle lane. Investors get digital portfolio management plus some level of human access. This model is especially attractive for people who want guidance but do not need a deeply customized family-office experience. The fee is usually lower because technology handles much of the investment engine, while advisors focus on planning questions and decision support.

Vanguard’s maximum 0.30% advisory fee, Fidelity Go’s 0.35% rate for larger balances, and Merrill Guided Investing with Advisor at 0.85% illustrate how wide the hybrid pricing range can be. The key question is not simply “Which is cheapest?” but “How much human advice do I actually get, and is it the kind I need?”

Digital Advisor or Robo-Advisor: About 0% to 0.50%

Digital advisors are usually the lowest-cost option. They are best suited for investors with straightforward goals, comfort using online tools, and limited need for custom tax, estate, or business-owner planning. A robo-advisor can build a diversified portfolio, rebalance automatically, harvest tax losses in some taxable accounts, and keep the investor from chasing whatever stock is trending because someone on the internet used too many rocket emojis.

Bankrate notes that robo-advisor fees commonly range from 0.25% to 0.50%, compared with around 0.25% to 1% or more for human advisors. Schwab’s no-advisory-fee model and Fidelity’s no-fee tier below $25,000 show how brokerages use digital advice to attract early-stage investors.

Are Lower Advisor Fees Always Better?

Not automatically. Lower fees are wonderful when the service fits the investor’s needs. But a low fee for the wrong service can be expensive in disguise. For example, a 0.30% digital platform may be a great bargain for a simple IRA rollover, but it may not be enough for a business owner juggling concentrated stock, estate-tax planning, charitable giving, and a retirement income strategy. In that situation, a higher advisory fee could be worthwhile if the advisor delivers measurable planning value.

Kitces research highlights that AUM fees often cover more than investment management. On average, 59% of a client’s AUM fee is attributed to investment management and 41% to financial planning and other advisory services. That means investors should not compare fees as if every advisor is selling the same product. Some are selling portfolio management. Others are selling an ongoing financial decision system.

The Hidden Costs Investors Should Watch

Fund Expense Ratios

An advisory fee is only one layer. Investors may also pay expense ratios on mutual funds or ETFs inside the account. A platform charging 0.30% with funds averaging 0.10% has an all-in investment cost of about 0.40%, before any other fees. A platform charging 0.85% with funds averaging 0.35% has an all-in cost closer to 1.20%. The headline advisory fee is the front door; the all-in cost is the whole house.

Cash Drag

Some low-fee or no-fee advisory platforms earn revenue indirectly from cash allocations or affiliated products. Schwab clearly explains that its Intelligent Portfolios program does not charge an advisory fee partly because Schwab Bank earns revenue from the cash allocation. That does not make the service bad; it simply means investors should understand the tradeoff.

Program, Custody, and Transaction Costs

Wrap programs may bundle investment advice, brokerage services, administrative costs, and trading into one fee. That sounds tidy, but investors should still ask what is included and what is not. The SEC describes wrap fee programs as bundled arrangements that can include investment advice, brokerage, administrative expenses, and other services for a single fee. In plain English: “one fee” does not always mean “only fee.”

How Fee Compression Is Changing Advisor Value

Fee compression does not mean advisors are disappearing. It means the job description is getting harder. Advisors can no longer charge premium prices merely for choosing a diversified fund portfolio. Index funds, model portfolios, and automated allocation tools have made basic portfolio construction cheaper and easier. The advisor’s value is increasingly judged by planning depth, tax coordination, withdrawal strategy, behavioral coaching, and the ability to help clients make better decisions under stress.

Cerulli’s data shows the industry moving more heavily toward fee-based compensation, with asset-based fees representing 72.4% of advisor compensation and commission-based revenue down to 23%. That shift gives clients more predictable pricing, but it also forces advisors to prove that their ongoing fee is justified year after year.

Examples: What Different Investors Might Pay

Example 1: The Beginner Investor

A 28-year-old investor with $18,000 may use a digital platform with no advisory fee or a very low annual cost. At this stage, the most valuable service may be automatic investing, diversified portfolios, goal tracking, and avoiding panic-selling. Paying 1% for full-service advice may not make sense yet unless the investor has unusual planning needs.

Example 2: The Mid-Career Family

A family with $350,000 across taxable accounts, IRAs, and old 401(k)s may benefit from hybrid advice. A 0.30% to 0.60% advisory fee could provide portfolio management plus access to planning conversations about college savings, insurance, retirement contributions, and tax-efficient investing. The fee should be compared against the value of better decisions, not just investment performance.

Example 3: The Pre-Retiree With $1.5 Million

A pre-retiree with $1.5 million may need more customized help: Social Security timing, Roth conversions, Medicare planning, tax-aware withdrawals, estate coordination, and risk management. A 0.75% or 1% fee may be reasonable if the advisor delivers comprehensive planning. But the client should still negotiate, compare tiers, and ask whether the fee declines as assets grow.

How to Evaluate Advisor Fees Before You Sign

Start by asking for the total annual cost in dollars, not just percentages. A 0.85% fee sounds small. On $750,000, it is $6,375 per year. That may be worth it, but it should not be invisible. Next, ask what services are included: investment management, financial planning, tax planning, estate coordination, retirement income planning, charitable giving, insurance review, and access to a dedicated advisor.

Then ask how the advisor is paid. Fee-only, fee-based, commission-based, and wrap-fee arrangements are not interchangeable. Finally, ask what would make the fee go down. Some firms reduce the percentage as assets increase. Others offer discounts through banking relationships, loyalty programs, or negotiated pricing. In a world of declining advisor fees, silence is expensive. Polite questions can save real money.

Experience-Based Insights: What Investors Learn When Comparing Brokerage Advisor Fees

One of the biggest real-world lessons investors discover is that fee shopping feels simple until the service menus start talking back. At first glance, the cheapest advisor looks like the obvious winner. Then the investor realizes one platform includes only automated portfolio management, another includes access to a rotating team of financial coaches, another offers a dedicated advisor, and another provides deeper planning but charges more. Suddenly, comparing advisor fees feels less like comparing apples to apples and more like comparing apples, apple pie, and a suspiciously expensive fruit basket.

A practical experience many investors share is the “percentage shock” moment. A 1% fee feels harmless until it is converted into dollars. On $100,000, it is $1,000 per year. On $500,000, it is $5,000. On $2 million, it is $20,000. That conversion changes the conversation. Investors become less focused on whether the advisor is friendly and more focused on whether the advisor is producing enough value to justify the annual cost. Friendliness is lovely; retirement cash-flow planning is lovelier.

Another common experience is realizing that cheaper platforms work beautifully until life becomes complicated. A young professional investing through a robo-advisor may be perfectly happy paying 0.25% or 0.35%. The portfolio is diversified, the app is easy, and the account does not require a conference call every time the S&P 500 sneezes. But when that same person gets married, buys a home, receives equity compensation, has children, or starts caring for aging parents, the need for personal advice grows. At that point, the question becomes whether to upgrade to hybrid or full-service advice.

Investors also learn that the best advisors explain fees without flinching. A confident advisor can say, “Here is what you pay, here is what you receive, here is what is not included, and here is when a lower-cost option might be better.” That honesty builds trust. A vague advisor who dodges fee questions is a red flag wearing polished shoes. Transparent pricing is not just good manners; it is part of the value proposition.

Many investors who compare brokerages also discover that the lowest headline fee may come with tradeoffs. A no-advisory-fee robo platform may hold more cash than the investor expects. A low-cost hybrid advisor may not offer a dedicated planner. A full-service advisor may provide excellent planning but use higher-cost funds. None of these models is automatically wrong. The investor’s job is to understand the deal before signing, not after the first quarterly statement arrives like a tiny financial plot twist.

The most valuable habit is reviewing fees annually. Portfolios grow, service needs change, and brokerage pricing evolves. An investor who needed high-touch advice during a retirement transition may later need only periodic planning. Another investor who began with a robo-advisor may eventually need a human expert. Advisor fees are declining, but the smartest investors do not simply chase the lowest number. They match the fee to the job. That is how cost control becomes wealth management instead of coupon clipping with a brokerage login.

Conclusion

Average advisor fees charged by brokerage firms are declining because investors have more choices, technology has lowered the cost of portfolio management, and large financial institutions are competing aggressively for advisory relationships. The traditional 1% AUM fee still exists, especially for comprehensive human advice, but it now competes with hybrid programs around 0.30% to 0.85% and digital platforms that may charge 0% to 0.50%.

The smartest move is not automatically choosing the cheapest advisor. It is understanding the full cost, the services included, the advisor’s compensation model, and the value delivered. If an advisor helps you avoid costly tax mistakes, plan retirement income, manage risk, and stay calm during market chaos, the fee may be money well spent. If the service is just basic portfolio allocation, lower-cost brokerage advisory options may do the job perfectly well.

Note: This article is educational content, not personal investment, tax, or legal advice. Investors should review each brokerage’s current fee schedule, Form CRS, advisory brochure, and program disclosures before making a decision.