Table of Contents >> Show >> Hide

- The Old Picture of “Mom and Pop” Is Outdated

- Why Market Caring Looks Different in 2026

- Yes, Retail Investors Still Show Up When Things Get Interesting

- Younger Investors Changed the Meaning of “Care”

- Why Some Families Feel Less Connected Even While They Own More

- What the Market Means to Ordinary Investors Now

- So, Does Mom and Pop Care About the Market Anymore?

- Experiences From the Real World: How This Question Plays Out in Everyday Life

- SEO Tags

For years, Wall Street loved a tidy little story about ordinary Americans: they got burned, got bored, and quietly left the market to the pros in expensive loafers. It is a dramatic narrative, and like many dramatic narratives, it falls apart the moment you look at real life. Mom and pop investors did not disappear. They changed uniforms.

Today’s household investor may not spend dinner arguing about steel stocks, clipping newspaper quotes, or calling a broker who sounds like he sells yachts on weekends. Instead, they auto-invest through a 401(k), buy broad-market ETFs on a phone, hold a target-date fund they barely think about, and occasionally panic-read headlines about inflation, AI, or interest rates while waiting for coffee. That is still market participation. It is just wearing sweatpants now.

So, does mom and pop care about the market anymore? Yes, but in a different way. The better question is this: do ordinary investors still care about beating the market, watching the market, and feeling emotionally attached to the market in the same way previous generations did? Not exactly. In many homes, the stock market has shifted from being a spectacle to being a system. It is less a hobby than a household utility. More boring. More automatic. Also, in many cases, more effective.

The Old Picture of “Mom and Pop” Is Outdated

The phrase “mom and pop investor” used to conjure up a very particular image: middle-class savers buying a handful of blue-chip stocks, reading the business section, and measuring financial health by what the Dow did that day. That investor still exists, but they are no longer the whole story. The modern retail investor universe is much broader. It includes parents dollar-cost averaging into S&P 500 funds, gig workers using fractional shares, retirees managing IRA withdrawals, and younger traders who came in through meme stocks and stayed for ETFs.

That shift matters because it changes how we interpret attention. If people are no longer obsessively checking ticker symbols, that does not mean they stopped caring. It may simply mean the market became embedded in retirement planning, long-term saving, and wealth-building routines. In other words, the emotional theater went down, but the financial exposure stayed surprisingly high.

Depending on how you measure it, roughly six in ten U.S. households now have stock exposure, especially when retirement accounts and funds are included. That is not a picture of mass indifference. That is a picture of widespread participation. The difference is that much of this exposure is indirect, diversified, and autopiloted. Mom and pop may not be day-trading at breakfast, but they are still invited to the party, and in many cases they already own the punch bowl.

Why Market Caring Looks Different in 2026

1. The 401(k) replaced the broker call

One reason ordinary investors seem less visibly engaged is that retirement accounts now do a lot of the talking. Millions of households own stocks not because they wake up itching to buy shares of an industrial conglomerate, but because their workplace plan funnels money into mutual funds, index funds, and target-date funds every pay period. That creates a quieter form of market participation. People still care deeply when markets swing, but they interact with those swings through quarterly statements, plan menus, and account balances rather than dramatic buy-and-sell decisions.

In practical terms, the market has become part of the plumbing of middle-class life. It helps finance retirement, college goals, and long-term security. When retirement assets reach staggering levels and account for a major share of household financial wealth, it becomes clear that “not caring” is mostly a myth. Plenty of Americans care. They just care through asset allocation, contribution rates, and whether their nest egg can survive another year of expensive groceries.

2. Indexing made investing less exciting and more durable

Another reason mom and pop appear less animated is that passive investing won the popularity contest. Broad index funds and ETFs do not provide the same cocktail-party storytelling as a hot stock tip. You cannot really brag that your thrilling investment strategy is “I bought the whole market and then took a walk.” But that simple approach has become a defining feature of household investing.

For many families, that is a good thing. Passive products lowered costs, simplified decision-making, and reduced the pressure to guess which stock will be tomorrow’s hero. The rise of target-date funds pushed this one step further by packaging diversification and rebalancing into one product. That means a lot of ordinary investors care less about making constant market calls and more about staying invested without doing something spectacularly unhelpful.

In short, mom and pop did not lose interest in investing. They outsourced some of the drama.

3. ETFs turned “investing” into everyday behavior

Exchange-traded funds helped change the culture. ETFs gave households a cheap, flexible way to buy broad indexes, sectors, dividend strategies, bonds, and increasingly specialized themes. For newer investors, ETFs are often the front door to the market. They are easy to understand at a basic level, easy to buy, and easy to fit into an app-based investing habit.

That has created a fascinating split in retail behavior. On one side, many households use ETFs as boring, brilliant building blocks for long-term wealth. On the other, some investors use them tactically to express short-term views on AI, rates, energy, crypto, or whatever the internet is yelling about this week. Same wrapper, very different vibes.

The important point is that this does not signal apathy. It signals adaptation. The modern retail investor is just as likely to use the market as a tool as they are to treat it like a scoreboard.

Yes, Retail Investors Still Show Up When Things Get Interesting

If anyone still doubts household interest in the market, they should look at what happens during volatility. Retail investors have repeatedly shown that they do, in fact, pay attention when headlines get loud enough. During sharp selloffs, speculative frenzies, and big thematic runs, individual investors often return in force. Recent years have shown record or near-record retail trading activity, large inflows into U.S. equities, and a willingness among individuals to buy dips, rotate into ETFs, or chase major narratives like artificial intelligence.

That is the paradox: ordinary investors may not look as emotionally attached to the market in calm periods, but they are absolutely still capable of becoming extremely engaged when the stakes feel immediate. In some households, “I do not really follow the market” mysteriously transforms into “Should we buy more now?” the second the S&P 500 has a miserable week.

This behavior suggests that mom and pop still care, but episodically. They are not always tuned in minute by minute. They are more event-driven. Big drops, big rallies, political shockwaves, rate moves, and hot sectors bring them back into the conversation fast. The market may no longer be a daily ritual for everyone, but it remains a powerful emotional trigger.

Younger Investors Changed the Meaning of “Care”

The generational divide also matters. Younger investors often interact with markets through apps, social media, short-form content, and communities that treat finance as part education, part entertainment, part identity. That can look different from traditional engagement, and frankly, sometimes it looks a little chaotic. But it still counts as caring.

What has changed is the source of confidence. Older investors often grew up trusting advisors, employer plans, and conventional diversification. Younger investors are more likely to self-educate, compare products online, and mix disciplined investing with bursts of speculation. Some of that behavior is smart. Some of it is pure chaos with a chart attached. But the broader trend is clear: retail investors are not detached from markets. They are embedded in a new information environment.

This has benefits and risks. Access is easier. Costs are lower. Research is everywhere. But so are hype, misinformation, and the seductive belief that every opinion with a microphone is wisdom. That means modern market caring is often noisier, faster, and more public than it used to be. The result is not indifference. It is overstimulation with a brokerage login.

Why Some Families Feel Less Connected Even While They Own More

Here is where the story gets subtle. Many Americans may own more market exposure than previous generations, yet feel less personally connected to the market’s daily movement. Why? Because ownership is often indirect. When your money lives inside a retirement plan, a balanced fund, or an automatic ETF contribution, you are participating without constantly making choices. Ownership becomes real, but abstract.

There is also the simple fact that life is expensive and distracting. Households juggling childcare, housing costs, healthcare bills, student loans, and job uncertainty are not necessarily eager to spend their free time studying valuation multiples. For a lot of families, the market matters most as a long-term outcome, not a daily experience. They care whether they are on track, not whether a semiconductor stock popped 7% before lunch.

That is why the old test for engagement no longer works. We should not ask whether ordinary investors watch CNBC all day or swap stock tips at the barbecue. We should ask whether they are allocating savings to market-linked assets, whether they increase contributions when confidence improves, whether they panic during drawdowns, and whether they see investing as necessary to financial progress. By that standard, mom and pop still care quite a bit.

What the Market Means to Ordinary Investors Now

It is less about excitement

For many households, investing has matured from a thrill-seeking activity into a practical necessity. The market is no longer viewed mainly as a casino for the bold or a mystery box for the rich. It is a tool for keeping up with inflation, building retirement security, and creating options later in life.

It is more about systems

Automatic contributions, target-date funds, broad ETFs, and robo-style habits have turned investing into a repeatable process. That makes retail participation more stable, even if it feels less cinematic.

It is still about emotion

Let us not get too cute here. People still feel market swings in their bones. Bull markets make households feel smarter, safer, and wealthier. Bear markets turn confident savers into amateur philosophers with a thousand-yard stare. The emotional component never left. It just lives underneath a layer of automation now.

So, Does Mom and Pop Care About the Market Anymore?

Yes. Just not in the old-fashioned, ticker-tape way.

Mom and pop still care because the market now touches retirement, emergency resilience, long-term wealth, and the basic math of staying financially afloat. They care through 401(k)s, IRAs, mutual funds, ETFs, and target-date funds. They care when volatility offers opportunity. They care when a selloff shrinks account balances. They care when inflation makes cash feel lazy and when compounding starts to look like one of the few respectable ways to get ahead.

What changed is the style of caring. The old retail investor often cared loudly, actively, and stock by stock. The modern household investor often cares quietly, automatically, and portfolio by portfolio. One version watched the market. The other lives inside it.

And that may be the biggest shift of all. Mom and pop did not leave Wall Street. Wall Street moved into mom and pop’s paycheck, retirement plan, phone app, and monthly anxiety rotation. Charming, really.

Experiences From the Real World: How This Question Plays Out in Everyday Life

Talk to enough ordinary investors and a pattern emerges. The classic stock-picker still exists, but the more common experience today is a family that interacts with the market in short bursts. A couple in their forties may not follow earnings season closely, yet they know exactly when their 401(k) balance drops because it changes how retirement feels in their imagination. When the market is up, they talk about being “on track.” When it is down, they tell themselves not to look and then look anyway. That is not indifference. That is modern investor behavior in its natural habitat.

Consider the experience of a middle-income household that mostly owns broad funds through work plans and an IRA. They are not chasing penny stocks or building spreadsheets at midnight. Their version of caring is deciding whether to raise contributions by 1%, whether to keep buying during a rough year, and whether to move idle cash from a bank account into something with better long-term potential. They do not talk about “alpha.” They talk about college, retirement, and whether they can someday stop answering emails on vacation. The market matters because it is attached to freedom.

Now look at a younger investor who started with meme stocks during the pandemic. Maybe the first trades were impulsive, social, and a little too dependent on rocket-ship emojis. But many of those investors did not simply vanish. Some learned hard lessons, shifted into ETFs, and kept investing. Their experience is not a story of leaving the market; it is a story of graduating from speculation to structure. They may still make the occasional spicy trade, but a growing share of their money goes into index funds, retirement accounts, and recurring contributions. In other words, the market became less of a game and more of a habit.

Retirees provide another revealing experience. Many older households care deeply about the market, but not because they want excitement. They care because sequence of returns, dividend income, withdrawal timing, and portfolio stability suddenly feel very personal. A bad market year is no longer just a red number on a screen. It can shape spending choices, gifting plans, and peace of mind. These investors often prefer balance over bravado. They still follow the market, but they tend to care less about winning cocktail-party arguments and more about preserving dignity, income, and optionality.

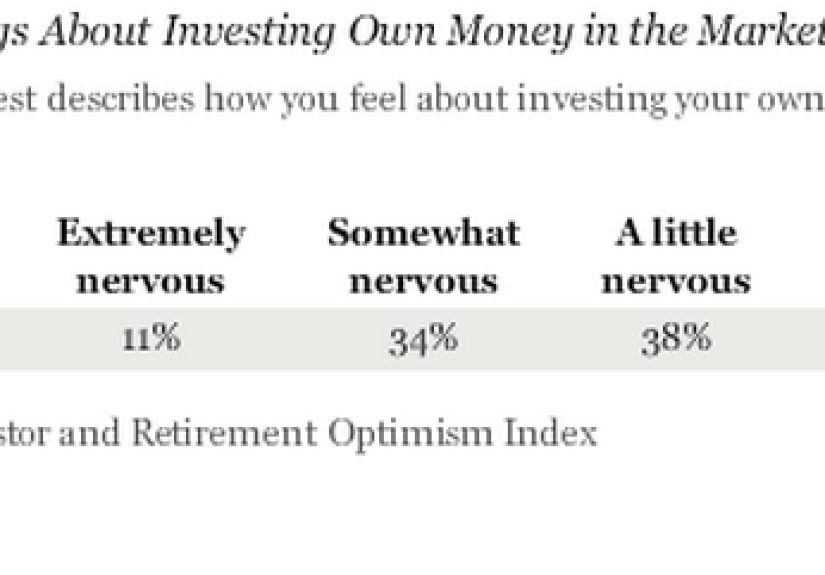

Then there is the broad emotional truth shared across generations: people pay the most attention when uncertainty rises. In calm periods, investing can feel like background music. During a selloff, it becomes the lead singer. Families who never mention the market start asking whether this is a buying opportunity or a warning sign. Younger investors search for ideas, older investors call advisors, and everyone suddenly becomes very interested in whatever the Federal Reserve is doing. The market still has that power. It can turn passive owners into active worriers in a single ugly week.

So the lived experience behind this topic is not that ordinary Americans stopped caring. It is that they now care in more practical, portfolio-based, goal-driven ways. They may not wear the old “mom and pop investor” costume anymore, but they are still very much in the scene. They are contributing, reallocating, worrying, holding, and occasionally overreacting like the rest of humanity. Which, for the record, is one of the most authentic market signals of all.