Table of Contents >> Show >> Hide

- Why “Staying the Course” Keeps Winning

- Market Volatility Is Not a Bug. It Is Part of the Deal.

- The Real Enemy Is Usually Behavior

- What Staying the Course Actually Looks Like

- Why Trying to Time the Market Usually Backfires

- Staying the Course Does Not Mean Ignoring Risk

- Why the Lesson Feels Fresh Every Time

- Conclusion: Boring Often Wins

- Real-Life Experiences: What “Staying the Course Worked Again” Feels Like

- SEO Tags

There are two kinds of investors during a rough market. The first refreshes the portfolio app every 11 minutes, sighs dramatically, and announces that “this time is different.” The second makes coffee, checks the long-term plan, and goes outside like a person with hobbies. History has been unusually kind to the second group.

That is the heart of this story: staying the course worked again. Not because markets are always friendly, tidy, or polite. They are none of those things. Markets throw tantrums, overreact to headlines, and occasionally act like they just discovered espresso. But over and over, disciplined investors who kept a diversified portfolio, continued investing, and resisted the temptation to panic have seen the same pattern play out. The storm was real. The fear was real. The recovery was real too.

For long-term investors, this is not a boring old slogan. It is one of the most useful lessons in personal finance. When volatility spikes, the urge to “do something” gets loud. Sell. Wait. Move to cash. Re-enter later when things feel safer. The problem is that “later” usually shows up wearing sunglasses after prices have already rebounded. By then, the investor who tried to dodge every drop is often left chasing the recovery they just missed.

Why “Staying the Course” Keeps Winning

At its core, staying the course means sticking with a sensible long-term investment plan even when the market starts behaving like a reality show reunion episode. It does not mean ignoring your finances, refusing to rebalance, or pretending risk does not exist. It means making decisions based on goals, time horizon, and asset allocation instead of fear, headlines, or a cousin who suddenly became a macroeconomic genius on social media.

Long-term investing works because markets have historically rewarded patience. Not every day, not every quarter, and certainly not every year. But over long stretches, investors have often benefited from economic growth, innovation, productivity, dividends, and compounding. Those gains rarely arrive in a straight line. They arrive in a messy zigzag that tests your confidence first and your patience second.

This is why disciplined investing matters so much. A plan built for a 15-year or 25-year goal should not collapse because the market had one ugly quarter or one scary month. If your timeline is long enough, volatility is often the admission price for growth. Not fun, not cute, not Instagrammable. But still the price.

Market Volatility Is Not a Bug. It Is Part of the Deal.

One of the biggest mistakes investors make is treating volatility like a system failure. In reality, market swings are a feature of investing in risk assets, not proof that the whole thing is broken. Stocks do not offer higher expected returns because they are emotionally soothing. They offer them because investors must tolerate uncertainty, drawdowns, recessions, bad headlines, election drama, rate anxiety, inflation scares, and the occasional “everything is down at once” week.

That sounds grim, but it is actually freeing. Once you understand that volatility is normal, you stop acting surprised every time it shows up uninvited. Corrections happen. Bear markets happen. Recoveries happen too. Investors who build their strategy around that reality tend to fare better than those who keep trying to outguess every twist in the road.

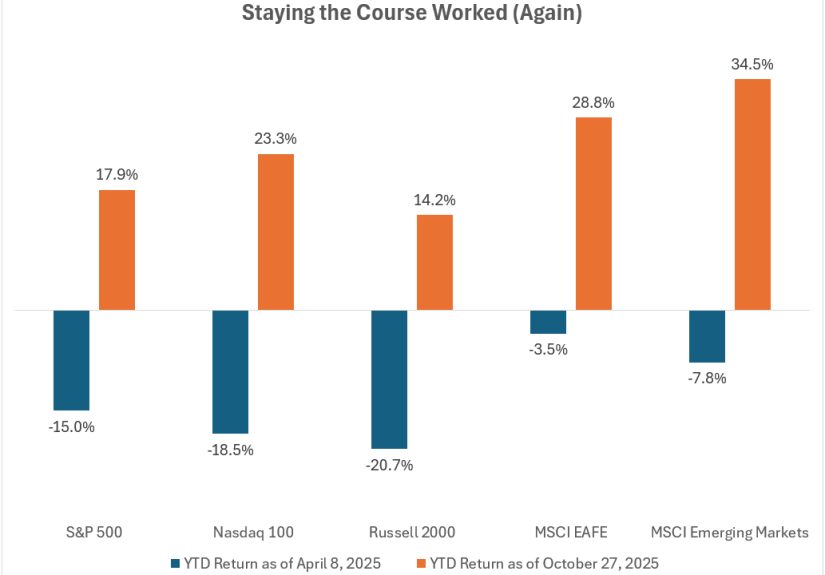

The 2020 and 2022 Reminder

Recent history gave investors a blunt refresher course. In 2020, markets plunged with alarming speed as the pandemic hit. In 2022, inflation, rapid rate hikes, and recession fears pushed stocks lower again. In both cases, the temptation to bail out felt rational in the moment. In both cases, investors who stayed invested were better positioned when markets recovered. That does not mean every portfolio bounced back on the same schedule or that every sector recovered equally. It means the old lesson showed up again in broad daylight: panic is expensive, patience is productive.

By the time recoveries feel “safe,” they are often already well underway. That is one reason timing the market is so hard. The best days frequently cluster near the worst days, which means investors who sell after a sharp drop can miss the powerful rebound that follows. Missing a few of those strong recovery sessions can do real damage to long-term returns.

The Real Enemy Is Usually Behavior

Most investing mistakes do not happen because people cannot do math. They happen because people are human. Fear screams louder than spreadsheets. Losses feel more personal than gains feel rewarding. The portfolio drops 12%, and suddenly the investor who once said, “I’m in it for the long haul,” is googling whether treasury bills can heal emotional wounds.

Behavioral finance has given this pattern plenty of labels, but the plain-English version is simple: people tend to buy confidence and sell discomfort. That is exactly backward. When prices are rising and everyone feels clever, expected future returns may be lower than they look. When markets are falling and nobody wants to hear the word “equities,” long-term opportunities can improve.

Staying the course helps investors avoid turning temporary declines into permanent damage. A market drop hurts. Selling after the drop locks in the pain. Then missing the rebound adds a second injury. It is the investing equivalent of slipping on a wet floor and then deciding to punch yourself in the shin for closure.

What Staying the Course Actually Looks Like

Let’s clear up a common misconception. Staying the course is not the same as doing absolutely nothing forever. Good long-term investors still monitor their plan. They rebalance when allocations drift too far. They keep contributing through dollar-cost averaging. They revisit goals when life changes. They hold enough cash for emergencies so they are not forced to sell investments at the worst possible moment. Calm discipline is not neglect. It is strategy.

1. Keep a Diversified Portfolio

A diversified portfolio spreads risk across asset classes, sectors, and geographies. It does not eliminate losses, but it can reduce the odds that one bad stretch in one corner of the market wrecks your entire plan. Diversification is not exciting dinner-party material, but neither are root canals, and one of those is much more useful.

2. Match Risk to Time Horizon

If you need the money in two years, it should not be riding shotgun in an aggressive stock allocation built for a retirement that is decades away. Time horizon matters. Long-term goals can usually tolerate more short-term volatility than near-term goals can. A smart portfolio is not just about return potential. It is about making sure your investments fit your actual life.

3. Keep Investing Through the Noise

Regular contributions during down markets can feel deeply unglamorous. You buy, the market falls, you buy again, and your reward appears to be more discomfort. But over time, that steady investing can mean purchasing shares at a range of prices, including lower ones. It is not magic. It is just discipline, repeated until it starts looking smart in hindsight.

4. Rebalance Instead of Reacting

When stocks surge or sink, portfolio allocations drift. Rebalancing can bring them back in line with your target mix. That process imposes useful discipline: trimming what has run hot and adding to what has lagged, rather than chasing whatever just made headlines. It is one of the few ways to be methodical when everyone else is improvising emotionally.

Why Trying to Time the Market Usually Backfires

The fantasy is irresistible. Sell before the drop, wait patiently in cash, then buy at the bottom with cinematic precision. Unfortunately, the market does not hand out trophies for dramatic timing attempts. It hands out confusion. Investors must make two perfect decisions, not one: when to get out and when to get back in. Missing either can leave them worse off than if they had simply stayed invested.

Even professionals struggle to forecast short-term moves consistently. The market responds to inflation data, central bank language, earnings, geopolitics, labor trends, valuation shifts, and plain old mood swings. By the time the “all clear” feels obvious, prices may already reflect it. The investor waiting for certainty is often waiting for a bus that already left two stops ago.

This is why “time in the market” tends to beat “timing the market” for ordinary investors. The longer you stay invested in a suitable portfolio, the more chances compounding has to work. The more you jump in and out, the more likely you are to turn volatility into self-inflicted sabotage.

Staying the Course Does Not Mean Ignoring Risk

There is an important nuance here. Staying the course is wise only when the course itself makes sense. If your portfolio is wildly too aggressive, badly concentrated, or mismatched to your goals, then sticking with it is not discipline. It is stubbornness in nicer clothing.

A sound investment plan starts with a few practical foundations: a realistic emergency fund, manageable debt, clear goals, and an allocation you can actually live with during downturns. If a 20% market decline will make you abandon ship every time, your plan may need adjustment. The best portfolio is not the one with the highest theoretical return. It is the one you can hold through the full market cycle without emotionally detonating.

This matters especially for retirees and near-retirees. Sequence-of-returns risk is real. Investors drawing income from their portfolios need a strategy that balances growth with liquidity and stability. For them, staying the course may involve cash reserves, bond exposure, bucket strategies, flexible withdrawals, and a more careful rebalancing process. Discipline still matters. The design just needs to fit the mission.

Why the Lesson Feels Fresh Every Time

The funny thing about market history is that it keeps repeating the same emotional script with slightly different costumes. One year it is inflation. Another year it is recession fears. Another year it is geopolitics, rate cuts, trade tensions, or an AI boom that suddenly looks too boomy. The details change. The investor temptation remains familiar: “Maybe I should just get out until things calm down.”

And yet, staying the course keeps working because the human mistakes keep repeating. Investors still overreact. Headlines still amplify fear. Short-term uncertainty still feels bigger than long-term progress. So each cycle becomes another chance to relearn the same durable truth: good plans do not become bad plans just because markets are nervous.

Conclusion: Boring Often Wins

“Staying the course worked again” is not a flashy headline because the strategy itself is not flashy. It is patient. It is disciplined. It is slightly boring in the best possible way. And that is exactly why it works so often.

Long-term investing is less about heroic predictions and more about durable habits. Keep a diversified portfolio. Match your investments to your goals and time horizon. Continue investing through volatility. Rebalance when necessary. Avoid emotional decisions. Repeat. That may not sound thrilling, but neither does quietly building wealth while other people are panic-refreshing market apps.

In investing, the person who stays calm does not always look brilliant in the moment. Usually, they look inactive. Maybe even dull. Then five or ten years later, they look like the only adult in the room. Once again, staying the course worked.

Real-Life Experiences: What “Staying the Course Worked Again” Feels Like

Ask people what staying invested feels like in real life, and almost none of them will call it comfortable. They will call it frustrating, nerve-racking, annoying, and occasionally ridiculous. That is because real investing does not happen in a textbook. It happens while bills are due, headlines are loud, and everyone around you suddenly has a strong opinion about what the Federal Reserve should do next.

One common experience goes like this: an investor sets up automatic contributions, picks a diversified mix of funds, and feels smart for about six months. Then the market drops. Contributions keep going in, but the account balance looks worse, not better. It feels like throwing water into a leaky bucket. The emotional temptation is immediate: pause contributions, wait for better conditions, and “be smart.” But months later, after the rebound arrives, those same purchases made during the downturn often become some of the best entries in the account. It never felt clever in real time. It only looked clever later.

Another experience is the retirement saver who opens a 401(k) during a strong market and begins to believe investing is mostly a pleasant upward escalator. Then a correction arrives and the escalator turns into a staircase made of Legos. Suddenly, every paycheck contribution feels like a test of character. Yet many workers who kept contributing through ugly periods later discovered they had accumulated more shares at lower prices. When the market recovered, the math finally caught up with the discipline.

Then there is the near-retiree experience, which is different and more emotionally loaded. For someone five years from retirement, volatility can feel less like a temporary inconvenience and more like a personal insult. In those moments, staying the course does not mean pretending everything is fine. It means leaning on a better-designed plan: cash reserves for short-term needs, bonds for ballast, stocks for longer-term growth, and a withdrawal strategy that does not force bad selling at bad times. For these investors, discipline is not denial. It is preparation paying off.

Many investors also describe the social side of staying the course. During sharp market swings, somebody always knows somebody who “went to cash at exactly the right time.” These stories spread with the speed and reliability of urban legends. Meanwhile, the person who quietly kept investing and rebalancing has no dramatic tale to tell at the barbecue. They just have a process. Years later, that process usually ages better than the legend.

Perhaps the most honest experience is this: staying the course rarely feels rewarding while you are doing it. It feels repetitive. It feels uncertain. Sometimes it feels like you are choosing patience simply because all the alternatives look worse. Then time passes. Markets recover. The account stabilizes, then grows. And what once felt like inaction reveals itself as one of the most productive decisions you made. That is the strange magic of disciplined investing. In the moment, it feels ordinary. In hindsight, it often looks wise.