Table of Contents >> Show >> Hide

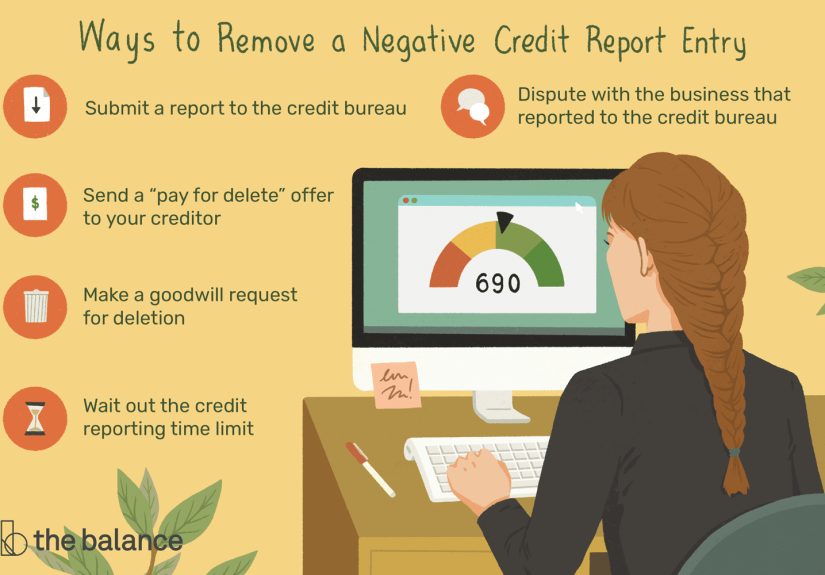

- Start Here: What “Removal” Actually Means

- Step 1: Pull Your Reports the Smart Way (All Three)

- Step 2: Build a “Negative Item Inventory” (Yes, Like a Spreadsheet)

- Strategy #1: Dispute Inaccurate or Incomplete Entries (The Highest-Probability Win)

- Strategy #2: Use Identity Theft Protections to Block Fraudulent Entries (Fast, Powerful, Document-Heavy)

- Strategy #3: Debt Validation for Collections (Confirm It’s Yours Before You Pay a Dime)

- Strategy #4: Fix Date Errors and “Re-Aging” Problems (The Sneaky Ones)

- Strategy #5: Negotiate Accurate Negatives (Goodwill, Pay-for-Delete, and Reality Checks)

- Strategy #6: Special CaseMedical Debt Entries

- Strategy #7: Escalate When You’re Right (and Polite Didn’t Work)

- Strategy #8: Avoid Credit Repair Traps and “Too Good to Be True” Shortcuts

- What to Expect: Timelines, Results, and Sanity Preservation

- Conclusion

- Experiences: What People Commonly Go Through When Cleaning Up Negative Entries (Approx. )

- SEO Tags

A credit report is basically your financial yearbook. Most of it is boring (addresses, account numbers, dates),

but one awkward photo (a late payment, a collection, a charge-off) can feel like it’s taped to your forehead.

The good news: you can remove negative entries when they’re wrong, outdated, incomplete, or tied to identity theft.

The “meh” news: accurate negative info usually can’t be forced off earlybut you still have smart, legal ways to reduce the damage

and sometimes get removals through negotiation.

This guide walks through practical, U.S.-based strategies that work in real lifewithout falling for “miracle” credit repair promises

or turning your mailbox into a war zone. We’ll cover disputes, debt validation, goodwill requests, collections negotiations, and

how to build a clean paper trail that makes bureaus and furnishers take you seriously.

Start Here: What “Removal” Actually Means

People say “remove a negative item,” but that can mean four different outcomes:

- Deleted: The entry disappears entirely (common when it’s not yours, can’t be verified, or is obsolete).

- Corrected/Updated: The entry stays, but key details change (balance, dates, status, payment history).

- Aged Off: The entry drops automatically after the allowed reporting period (often 7 years; some items longer).

- Suppressed/Blocked: The entry is blocked due to identity theft documentation (strongest “fast removal” path).

The strategy depends on which outcome you’re chasing. If the item is inaccurate, you’re in the “delete or correct” lane. If it’s accurate,

you’re mostly in the “negotiate, minimize, or wait it out” lane.

Step 1: Pull Your Reports the Smart Way (All Three)

Your first move is not writing lettersit’s getting the full picture. The three nationwide credit bureaus don’t always show the same accounts

or the same details. You might have an error on one report and a clean record on the others.

Where to get your reports

- AnnualCreditReport.com is the official place to access your reports. It’s also a great “identity theft smoke detector.”

- Check frequency: Free weekly online reports are available from Equifax, Experian, and TransUnion (handy during clean-up mode).

- Tip: Pull all three reports on the same day when you’re actively disputing so you can compare dates and details.

What to download and save

- The PDF/print view of each bureau report (date-stamped).

- A screenshot or saved page showing “estimated removal date” (if provided).

- Any notices in your inbox/portal related to disputes or results.

Treat these like receipts. If you ever need to escalate (or simply prove a date changed), having “before” and “after” copies matters.

Step 2: Build a “Negative Item Inventory” (Yes, Like a Spreadsheet)

Credit clean-up gets messy when you dispute randomly. Instead, create a simple inventory for each negative entry:

- Bureau(s): Equifax / Experian / TransUnion

- Furnisher: The company reporting it (original creditor, lender, or collection agency)

- Account type: Late payment, collection, charge-off, repo, foreclosure, bankruptcy, inquiry, etc.

- What looks wrong: Not yours, wrong dates, duplicate listing, incorrect balance, wrong status, wrong payment history

- Your evidence: Statements, payment confirmations, identity theft report, police report (if applicable), letters, emails

- Desired outcome: Delete, correct, mark “paid,” remove duplicate, block for identity theft, or age-off confirmation

This inventory keeps you focused and stops you from firing off disputes like confetti. Confetti is festive. Confetti disputes are usually not.

Strategy #1: Dispute Inaccurate or Incomplete Entries (The Highest-Probability Win)

If the negative item is wrong, incomplete, or can’t be verified, you have a solid path to removal. This is where most legitimate “credit repair”

outcomes come frombecause you’re enforcing accuracy, not begging for mercy.

Common credit report errors worth disputing

- Not your account: Similar name, mixed file, or identity theft.

- Duplicate collections: Same debt listed more than once (or by multiple collectors).

- Wrong dates: Incorrect “date of first delinquency” or status dates that make an item appear newer.

- Wrong status: “Open” when it’s closed, “delinquent” when it’s current, “unpaid” when paid/settled.

- Wrong amounts: Inflated balance, incorrect past-due amount, fees that don’t belong.

- Payment history glitches: A payment marked late when you have proof it posted on time.

How to dispute with a credit bureau (without sabotaging yourself)

- Dispute one or two items at a time if they’re complex. Bulk disputes can get sloppy responses.

- Be specific. “This account is inaccurate” is weaker than “This is not my account; opened on X date; I never lived at Y address.”

- Attach proof. Payment confirmations, statements, letters from the creditor, identity documents, etc.

- Choose your channel wisely. Online disputes are fast. Written disputes can create a cleaner paper trail. Pick the one you’ll manage best.

- Keep copies. Save what you sent and what you received backalways.

After you file a dispute, the credit reporting company generally must investigate within about 30 days, and then notify you of results shortly after.

If you send additional information during the process, it may extend the timeline (often up to 45 days).

Also dispute directly with the furnisher (the company reporting it)

Don’t rely only on the bureaus. The furnisher is the source of the data. If the furnisher corrects their records, the bureaus are far more likely to update.

Many banks and lenders have dedicated “credit reporting” or “dispute” addresses and portals.

Practical example: If a credit card shows a 30-day late payment for April, but you have a bank confirmation that the payment posted on March 28,

dispute with the bureau and send the creditor your evidence with a simple request: “Please correct the reported payment history and notify all bureaus.”

Strategy #2: Use Identity Theft Protections to Block Fraudulent Entries (Fast, Powerful, Document-Heavy)

If an account is the result of identity theft, you’re not stuck with “normal” dispute rules. U.S. law provides a process to block identity-theft information

from your credit file when you provide proper documentation.

What usually works best

- Create an Identity Theft Report through IdentityTheft.gov and follow the recovery steps.

- Send proof of identity (as requested by the bureau).

- Identify the specific account(s) you want blocked, with account numbers if possible.

- Ask for a block under FCRA 605B (plain language is fine; you’re not drafting a Supreme Court brief).

This route is especially effective for “I never opened this” situations: fake credit cards, unauthorized personal loans, or addresses you’ve never lived at.

It’s also where you should be extremely honestnever file a false identity theft claim. It can backfire legally and financially.

Strategy #3: Debt Validation for Collections (Confirm It’s Yours Before You Pay a Dime)

Collections accounts are the most frustrating negative entries because they can show up after a debt changes hands and records get messy.

Before you negotiate, validate.

What “debt validation” does

When a debt collector contacts you, they must provide certain information about the debt and your rights. Once you receive that validation information,

you generally have a window (commonly 30 days) to dispute the debt in writing and request verification.

What to ask for in a validation request

- The amount claimed and how it was calculated (principal, interest, fees).

- The name of the original creditor.

- Documentation showing you owe the debt (not just a spreadsheet line item).

- Proof the collector has the right to collect (especially if the debt was sold).

Mini-scenario: You see a $1,240 collection from a company you’ve never heard of. Before you “pay to make it go away,” request validation.

If the collector can’t substantiate the debtor it’s clearly not yoursyou’re in removal territory.

Strategy #4: Fix Date Errors and “Re-Aging” Problems (The Sneaky Ones)

Negative items don’t report forever. Most negative info typically has a time limit. But the clock depends on the correct delinquency timeline.

If a date is wrong, an item can linger longer than it shouldor look newer than it is.

What to watch for

- Date of first delinquency confusion: The seven-year reporting window often ties back to the delinquency that led to the negative status.

- Debt sold ≠ debt “restarts”: A collector buying a debt does not magically reset the original delinquency date.

- Fresh “last activity” dates: Your credit report timeline shouldn’t jump forward because someone called you or mailed you.

If you see a collection reporting with a delinquency date that doesn’t match the original account’s history, dispute it as an incorrect date.

Include older statements, prior bureau reports, or creditor letters showing when the delinquency actually occurred.

Strategy #5: Negotiate Accurate Negatives (Goodwill, Pay-for-Delete, and Reality Checks)

If the negative item is accurate, your goal shifts from “prove it’s wrong” to “ask for a discretionary removal.”

This can worksometimes. Just don’t treat it like a guaranteed coupon.

Option A: Goodwill letters for late payments

A goodwill letter is a polite request to remove an accurate late payment as a courtesyusually after you’ve re-established a strong on-time pattern.

It tends to work best when:

- You have a long history of on-time payments before and after the incident.

- The late payment was caused by a one-off event (move, autopay error, medical emergency, etc.).

- You’re now current and ideally paid down (or paid off).

Goodwill language that sounds human: “I’ve been a customer for 6 years and this late payment was an exception during a move.

My history otherwise is on-time. Would you consider a one-time courtesy adjustment to the reported late payment?”

Option B: Pay-for-delete for collection accounts

Pay-for-delete means you offer payment (often in full, sometimes negotiated) in exchange for the collector deleting the collection tradeline from your credit reports.

Important truths:

- Not every collector agrees. Some will refuse, period.

- Get it in writing before you pay, when possible.

- The original creditor history may remain even if a collector deletes their entry.

Practical example: If you have a $300 non-medical collection that’s dragging your score, and you’re trying to qualify for an apartment soon,

a pay-for-delete request can be worth attemptingespecially if the collector is willing to confirm deletion terms in writing.

Option C: Settlement updates (helpful, but not “removal”)

Even when an item can’t be deleted, getting it updated matters. For example:

- “Unpaid collection” → “Paid collection” (or “Settled”).

- Incorrect balance → $0 after payment.

- Wrong status → “Closed” once resolved.

This won’t erase history, but it can reduce lender concerns, improve manual underwriting outcomes, and help your profile look stable again.

Strategy #6: Special CaseMedical Debt Entries

Medical debt is its own weird universe: insurance delays, billing errors, and “wait, I owe what?” moments.

The credit reporting landscape has changed significantly in recent years.

What to do if medical debt is on your reports

- Confirm the details: Who owns it? Is it paid? Is it under the relevant reporting thresholds?

- Dispute billing errors aggressively: Medical bills are notorious for coding and insurance processing issues.

- Document everything: EOBs (explanations of benefits), provider statements, payment receipts.

If you suspect the medical collection is inaccurate or should not be reporting based on current reporting practices,

dispute it with the bureaus and request the provider/collector correct or withdraw the reporting.

Strategy #7: Escalate When You’re Right (and Polite Didn’t Work)

Sometimes you do everything correctly and still get the dreaded “verified” response. That doesn’t always mean the item is accurate; it can mean the furnisher

responded in a way the bureau accepted. When that happens, you have escalation tools.

Escalation options that stay legal and effective

- Send a second dispute with stronger evidence: include a clearer explanation, add missing documentation, correct any inconsistencies.

- Dispute with the furnisher again: ask for their specific basis for reporting and what records they relied on.

- Add a consumer statement: a short statement can be attached to your file (best used sparingly).

- File a complaint: if the bureau or furnisher isn’t resolving a legitimate problem, you can submit a complaint with the CFPB.

The goal is not to “fight harder.” The goal is to communicate more clearly, with better proof, through channels that create accountability.

Strategy #8: Avoid Credit Repair Traps and “Too Good to Be True” Shortcuts

If someone promises they can remove all negative itemseven accurate oneswhile you do nothing, that’s not a strategy.

That’s a red flag wearing a trench coat and fake mustache.

Red flags to run from

- Upfront fees: Legit credit repair services generally can’t demand payment before work is completed under federal protections.

- “New identity” pitches: CPNs, credit profile numbers, or “fresh file” hacks can be illegal and dangerous.

- Fake disputes: telling you to dispute everything as “not mine” when it is yours.

- Guaranteed outcomes: no one can guarantee deletions for accurate, timely information.

You can do nearly everything in this article yourself for the cost of stamps and patience. If you hire help, choose nonprofit credit counseling

for budgeting and debt managementdifferent lane, often more trustworthy.

What to Expect: Timelines, Results, and Sanity Preservation

Credit clean-up isn’t instant. But it’s not mysterious either. Here’s a realistic flow:

- Week 1: Pull reports, build inventory, gather evidence.

- Weeks 2–3: Submit targeted disputes and/or validation requests.

- Weeks 4–7: Investigations complete, results arrive, updates post (timing varies).

- Weeks 8+: Escalate where needed, negotiate collections, and keep positive credit habits steady.

If you’re doing this for a near-term goal (mortgage, rental, car loan), focus on the highest-impact items first:

identity theft accounts, wrong late payments, duplicates, and collections you can validate or resolve cleanly.

Conclusion

Removing negative credit report entries is less about “credit hacks” and more about accuracy, documentation, and timing.

When an item is wrong, you dispute it with evidence and persistence. When it’s tied to identity theft, you use the strongest protections available

to block it. When it’s accurate, you shift to negotiationgoodwill letters, strategic settlements, and pay-for-delete attemptswhile your positive habits

quietly rebuild trust in the background.

Think of your credit report like a kitchen: you don’t fix it by yelling at the fridge. You fix it by throwing out expired stuff,

labeling what’s yours, and cleaning up the spills with receipts. (Okay, maybe your kitchen doesn’t have receipts. But your credit life should.)

Experiences: What People Commonly Go Through When Cleaning Up Negative Entries (Approx. )

Most people expect credit report clean-up to feel like clicking “unsubscribe” and moving on with life. In reality, it often feels more like canceling a gym membership:

doable, but you’ll want screenshots, timestamps, and maybe a calming playlist.

One common experience is the “mixed file surprise.” Someone pulls their reports and sees an account they swear they never openedoften with a similar name

or a previous address they once shared with a relative. The first wave is panic (“Is this identity theft?”), but the second wave is relief when they realize it’s a data mix-up.

The win usually comes from being specific: disputing the account as “not mine,” attaching proof of identity, and highlighting mismatched details (wrong middle initial, incorrect employer,

an address they’ve never lived at). When the bureau deletes it, the feeling is equal parts victory and “why was this my job, exactly?”

Another common storyline is the “late payment that shouldn’t be late.” This is often a posting issue: autopay failed after a card number changed,

a payment was scheduled on a holiday, or the bank processed it but the creditor posted it a day later. People who succeed here tend to do two things:

(1) they pull proof from their bank (a confirmation number, a posted date, a statement), and (2) they contact the creditor directly, not just the bureau.

The emotional arc is predictable: confidence → frustration after a “verified” response → success once a human at the creditor sees the evidence and agrees to correct the reporting.

It’s not always fast, but it’s often fixable.

Collections create their own category of experiences: confusion, annoyance, and negotiation fatigue. Many people describe the first discovery as,

“I never even got a bill.” Sometimes that’s because the debt changed hands, the address was old, or the bill was tangled in insurance processing (especially medical).

The smartest turning point is usually a debt validation request. When validation comes back thin or inconsistent, people feel empowered to dispute with the bureaus.

When validation is solid, people move to negotiationsometimes offering a quick payment in exchange for deletion, sometimes settling and focusing on getting the balance to $0 and

preventing future surprises.

The biggest lesson people tend to learn is that organization beats intensity. The folks who get results aren’t necessarily the angriest or loudest;

they’re the ones who keep a simple log: what they sent, when they sent it, what they received, and what changed on each report. Credit clean-up is rarely glamorous,

but when a negative entry disappears (or finally corrects), it feels like getting your name cleared in the group chat. Quietly satisfying. Very worth it.