Table of Contents >> Show >> Hide

- Did the Pandemic Really Make Everyone Richer?

- How the Pandemic Inflated Balance Sheets

- Why “Richer” Doesn’t Always Feel Rich

- A Wealth of Common Sense: What the Headline Really Means

- Practical Money Lessons from a Very Weird Wealth Boom

- Lived Experiences: How the Pandemic Quietly Rewired Our Money Habits

- Wrapping It Up: Richer on Paper, Smarter in Practice

If you had told anyone in early 2020when we were wiping down groceries and baking panic sourdoughthat a few years later economists would be arguing that the pandemic made Americans richer, you probably would’ve been muted on Zoom. And yet, when you look at the numbers on household net worth, savings, and asset prices, that provocative headline from the blog A Wealth of Common Sense isn’t as wild as it sounds.

Of course, “richer” here doesn’t mean everyone suddenly joined the billionaire club. It means that, on average, U.S. households ended up with higher net worth after the COVID shock than they had going in. At the same time, inflation, debt, and inequality have made many people feel anything but wealthy. In other words, the math and the mood don’t always match.

This article unpacks what “The Pandemic Has Made Everyone Richer” really means, why the data supports (and complicates) that idea, and how to turn this strange period into a little more common sense for your own money decisions.

Did the Pandemic Really Make Everyone Richer?

Net worth numbers: what the data actually say

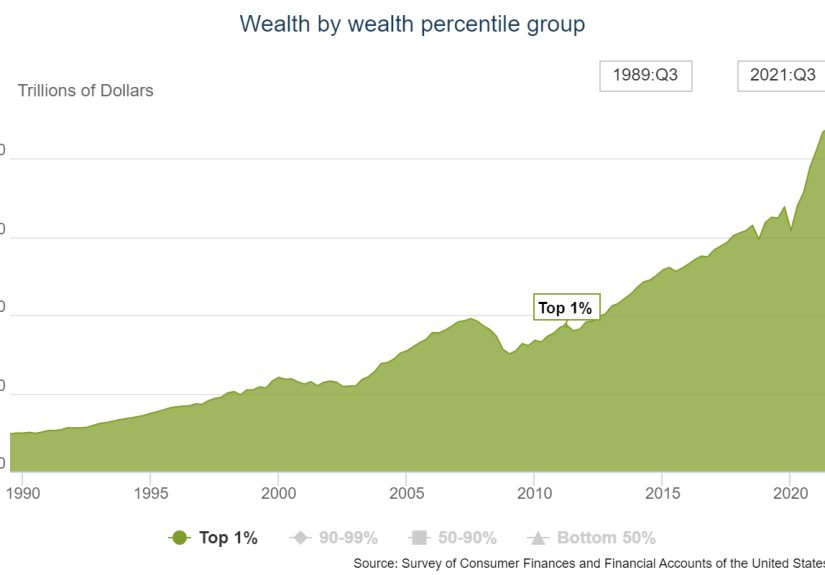

Let’s start with the receipts. Surveys of consumer finances from the Federal Reserve show that median household net worth in the U.S. jumped sharply between 2019 and 2022. In many breakdowns, median net worth rises by around 30% or more over that period, thanks to a mix of higher home values, booming stock markets, and unusually high savings.

Other analyses using the same data find that median net worth climbed from roughly the low $100,000s pre-pandemic to close to $200,000 by 2022. That’s a huge move in a very short timeespecially coming after a once-in-a-century public health crisis.

More recent commentary from Federal Reserve researchers suggests that, even after the inflation spike and market volatility of 2022, average wealth across racial and income groups in 2024 is still higher than it was before COVID hit. In other words, after all that chaos, the baseline for wealth has shifted up rather than down.

The great pandemic savings spike

You might remember the chart that made the rounds in 2020 showing personal savings blasting off like a meme stock. That wasn’t a mirage. The U.S. personal saving rate, which usually hovers around 7%–8% of disposable income, briefly soared into the high teens and even above 30% at the peak of lockdowns.

Why? Money came in, but there was nowhere to spend it. Government relief payments, enhanced unemployment benefits, and child tax credits pushed incomes up for many households. At the same time, travel, dining out, commuting, concerts, and kids’ activities all slammed into a brick wall. The result: an estimated trillions of dollars in “excess savings” accumulated over roughly 18 months.

Those savings didn’t just sit in checking accounts. They paid down debt, funded home down payments, flowed into brokerage accounts, and, yes, helped fuel the boom in Robinhood trading and crypto experiments. Some of that money is gone now, but the net effect on household balance sheets was big and positive.

How the Pandemic Inflated Balance Sheets

Stimulus checks and safety nets

In normal recessions, the government tends to move slowly and cautiously. In 2020, policymakers basically grabbed the fire hose. Multiple rounds of stimulus checks, expanded unemployment insurance, PPP loans to small businesses, pauses on student loan payments, and eviction moratoriums all acted as a massive shock absorber.

For many lower- and middle-income households, this meant that cash flow actually improved for a period of time, even as the economy shut down. That’s wildly unusual in a recession. Some families who had never been able to build a cash cushion suddenly found themselves with a few thousand dollars in the bank.

From a pure balance-sheet perspective, that looks like “getting richer.” From a psychological perspective, it often felt like barely hanging on during a crisis. Both things can be true at the same time.

Housing: your home became a rocket ship

The housing market deserves its own subplot in this story. Ultra-low interest rates and a surge in demand for more spaceto work, study, exercise, and hide from your roommatespushed home prices sharply higher in many parts of the country.

For homeowners, especially those who bought before 2020, this was like being gifted thousands (or hundreds of thousands) of dollars in home equity. Combine that with mortgage refinancing at historically low rates, and you had a stealth wealth event for anyone who owned property.

For renters and first-time homebuyers, though, the same trend turned homeownership into a moving target. Prices jumped faster than savings could keep up. So while the average household got richer on paper, a younger, more renter-heavy group watched the ladder pull further away.

The stock market whiplash (that ended up higher)

Remember those terrifying weeks in March 2020 when markets were melting down? It’s easy to forget that after that crash came one of the fastest recoveries in history. Major stock indexes bounced back within months and then went on to set record highs.

Households who already owned stocks in 401(k)s, IRAs, or taxable accounts benefited the most. The rally in tech stocks and big-cap growth names, in particular, massively boosted the wealth of higher-income families and the ultra-rich. For them, the pandemic wealth effect was a rocket ride.

At the same time, more retail investors than ever opened brokerage accounts, experimented with fractional shares, and dipped into the market during lockdowns. Not everyone became a genius traderfar from itbut the culture around investing shifted, and more people started seeing equities as accessible rather than elite.

Why “Richer” Doesn’t Always Feel Rich

Inflation quietly ate part of the gains

If your net worth rose 30%, but your grocery bill feels like it doubled, your brain doesn’t exactly pop champagne. After the initial shock of the pandemic, inflation surged to levels not seen in four decades. Housing, food, energy, and services all climbed, sometimes painfully fast.

When we say “Americans got richer,” we’re usually talking about nominal net worthdollars, not purchasing power. Adjusting for inflation shrinks those gains. Many households are, in real terms, better off than pre-COVID but not nearly as much as raw numbers suggest.

It’s like getting a raise at work, only to realize that your rent and your favorite takeout spot conspired to steal it back. The spreadsheet says you’re up; your day-to-day life says, “Are we sure?”

Who was left behind (or pushed further behind)

The phrase “everyone richer” makes for a punchy headline, but it glosses over some hard truths. Researchers who slice the data by race, ethnicity, and starting wealth levels find that gains were uneven:

- Households that already had higher net worthespecially white and Asian familiessaw the largest dollar gains from rising home values and stock prices.

- Lower-wealth households often did see meaningful percentage increases in net worth, but from very low starting levels. Going from $5,000 to $8,000 is a 60% jump, but it doesn’t suddenly make life comfortable.

- Black and Hispanic households were more likely to carry burdensome debt, face job disruptions, and live in communities with higher health and economic risks.

The upshot: the pie got bigger, but the slices didn’t magically become equal. In some ways, the pandemic actually deepened long-running patterns of inequality, even as it lifted the broad averages.

Debt, rent, and financial fragility

Another reason it doesn’t feel like we’ve all gotten richer: a lot of households are right back to living on the edge. Surveys of household financial well-being show that the share of Americans who say they are “doing okay” financially is lower than it was in 2019. Many report trouble covering basic expenses, managing unexpected bills, or keeping up with rent.

Part of this comes from the unwinding of those pandemic supports. Excess savings have largely been drawn down. Student loan payments resumed. Rents jumped. Credit card balances climbed as people tried to maintain their lifestyle in the face of higher prices.

So yes, the average net worth line is higher. But the emotional reality for many families is that their margin for error feels thinner than ever.

A Wealth of Common Sense: What the Headline Really Means

Ben Carlson’s post “The Pandemic Has Made Everyone Richer” on his blog A Wealth of Common Sense is intentionally provocative. He’s not claiming the pandemic was good or that suffering didn’t happen. Instead, he’s highlighting one of the big paradoxes of modern finance: we measure our gains in relative, not absolute, terms.

If your net worth rose 25%, but your neighbor’s went up 40%, you’re likely to feel behind, even though you’re objectively better off than you were before. That’s human psychology 101. We don’t compare ourselves to our past selves; we compare ourselves to the people in our feed.

The pandemic amplified this effect. Asset owners saw their wealth surge. People in certain industries (tech, finance, knowledge work) could work from home, keep their paychecks, and watch their portfolios grow. Others lost jobs, risked their health on the front lines, or shut down small businesses. When you log on and see memes about “stocks only go up” while you’re juggling three gigs, it doesn’t feel like the same story.

The “common sense” here is not that pandemics are good for wealth. It’s that:, if you want to make sense of your own finances, you have to stop measuring your progress on someone else’s scoreboard. Look at your own before-and-after picture, in both dollars and quality of life.

Practical Money Lessons from a Very Weird Wealth Boom

1. Cash buffers are not optional

One of the clearest lessons from 2020: life can change faster than your HR department. The households that slept the best were the ones with an emergency fundwhether it came from years of saving or from unexpected stimulus windfalls they didn’t immediately spend.

If you came out of the pandemic with a bit more cash than you’d ever had before, that’s not a signal to permanently upgrade your lifestyle. It’s a reminder to build a sustainable buffer: three to six months of essential expenses in savings, more if your income is unpredictable.

2. Ownership matters more than ever

The pandemic wealth boom was largely an asset boom. Homeowners, stock investors, and business owners benefited disproportionately. That doesn’t mean you need to chase every hot investmentwhich is how people turn stimulus checks into very expensive lessonsbut it does mean that owning things that can appreciate over time is your best defense against future shocks.

Practical steps might include:

- Consistently contributing to a 401(k) or IRA, even in small amounts.

- Working toward a realistic homeownership plan if it fits your life, or investing through low-cost index funds if housing is out of reach for now.

- Building a business or side hustle that creates equity, not just hours traded for dollars.

3. Don’t confuse one-time windfalls with permanent income

Stimulus checks, paused loan payments, and temporarily lower expenses created a sense of “extra” money. The trap was assuming that extra would be permanentupgrading cars, signing pricier leases, or locking in subscriptions you didn’t really need.

Common-sense rule: treat windfalls like you treat dessert. Enjoy some, but don’t build your entire diet around it. Use at least half of any unexpected money to strengthen your balance sheetpay down debt, boost savings, or investbefore you let the rest flow into lifestyle upgrades.

4. Mind the inflation gap

As prices rise, the hurdle rate for your money rises too. Keeping all your savings in cash felt safe during the early pandemic, but over time inflation quietly erodes that pile. The post-pandemic period has been a real-time lesson that “no risk” on paper can still mean “very real risk” to your future purchasing power.

That doesn’t mean dumping everything into volatile assets. It does mean thinking in layers: enough cash for near-term needs, then longer-term money in investments that have a shot at beating inflation over time.

Lived Experiences: How the Pandemic Quietly Rewired Our Money Habits

Beyond charts and net worth tables, the pandemic left behind a strange mix of financial instinctssome helpful, some not so much. Here are a few of the most common experiences people report, and what they can teach us going forward.

From “spend what’s left” to “save first”

Many households got a crash course in what it feels like to have a real cash cushion. Maybe it came from a tax credit, a stimulus check, or simply spending less on commuting and travel. For a lot of people, that was the first time they had more than a paycheck or two in the bank.

The emotional shift was huge: fewer sleepless nights, less panic when the car needed repairs, a sense that maybe you could handle a surprise bill. That experience converted some lifelong “spend what’s left” people into “save first” people. Instead of hoping money would remain at the end of the month, they started paying themselves firstautomatic transfers into savings or retirement as soon as the paycheck hit.

If you felt how good that buffer was, that’s your cue to formalize it. The feeling of safety wasn’t a fluke; it was the byproduct of an intentional habit you can keep even when the crisis headlines fade.

Re-evaluating what’s worth paying for

Lockdowns forced everyone to confront a weird question: “What do I actually miss spending money on?” For some, it turned out they didn’t miss $15 cocktails, but they really missed visiting family. Others realized a home office was worth more than a new car. Parents discovered that paying for childcare wasn’t a luxuryit was the foundation that kept everything else working.

Those realizations are a gold mine. They’re a built-in values audit. The smartest post-pandemic budgets aren’t just tighter; they’re more intentional. They funnel money toward the things that genuinely improved life during a hard time, and they starve the expenses that turned out to be mindless habits.

The rise (and hangover) of DIY investing

With more time at home and more cash in accounts, millions experimented with investing apps, options trading, crypto, and speculative growth stocks. Some hit lucky streaks. Others learned that volatility can be very educational and very expensive.

The lasting benefit is that investing is no longer a mysterious black box for many people. They understand how markets move, what it feels like to see a portfolio drop, and why “get rich quick” is usually just “get stressed faster.” The next level of maturity is shifting from adrenaline-driven trades to boring, consistent, long-term investingindex funds, diversified portfolios, and clear goals.

Seeing money as resilience, not just consumption

Finally, the pandemic reframed what wealth is for. It’s not just a high score on a financial dashboard; it’s resilience. It’s the ability to handle a job loss, care for a sick relative, move to a safer place, or take time off when you’re burned out.

When you view money as resilience, decisions change. The question stops being “What can this buy me right now?” and becomes “How does this make my life safer, freer, or more flexible in the long run?” That’s the real wealth of common sense the pandemic left behindif we’re willing to keep it.

Wrapping It Up: Richer on Paper, Smarter in Practice

So, did the pandemic make everyone richer? In a narrow, technical sense, yes: median and average household net worth are higher than they were before COVID. Savings spiked, assets boomed, and government support created a one-time, bizarre wealth experiment.

But the headline doesn’t tell the whole story. Inequality widened, inflation took a bite out of gains, and many families remain financially fragile even as the charts trend upward. The real opportunity isn’t to argue with the graphs; it’s to use this weird episode as a catalyst.

If you can come away from the pandemic era with a stronger emergency fund, a deeper commitment to owning long-term assets, a more intentional budget, and a healthier relationship with risk, then you’ve gained something more valuable than a temporary bump in net worth. You’ve gained a durable kind of wealth: the ability to navigate uncertainty with a little more confidence and a lot more common sense.