Table of Contents >> Show >> Hide

- Credit Limit, Explained

- How Credit Limits Work in Real Life

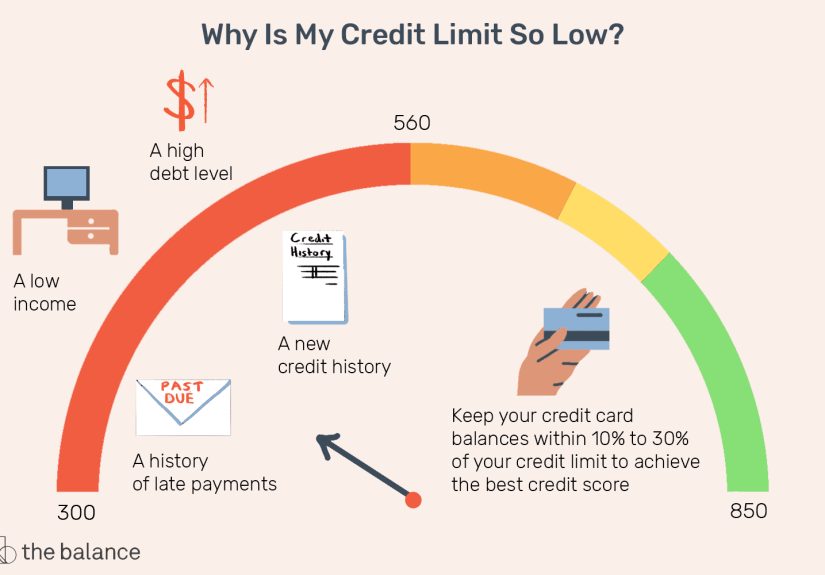

- How Lenders Decide Your Credit Limit

- Why Your Credit Limit Matters for Your Credit Score

- How Credit Limits Can Change Over Time

- How to Request a Credit Limit Increase (or Decrease)

- Common Myths About Credit Limits

- Smart Ways to Manage Your Credit Limit

- Real-Life Experiences and Lessons About Credit Limits

- The Bottom Line

If you’ve ever swiped a credit card, you’ve already met your credit limiteven if you’ve never thought about it. It’s that invisible line between “approved” and “declined,” between “this is fine” and “okay, maybe I went a little too hard on concert tickets and takeout this month.”

Understanding what a credit limit is (and how it works) can help you avoid fees, protect your credit score, and actually make lenders like you more over time. Let’s break it all down in plain Englishno finance degree required.

Credit Limit, Explained

In simple terms, a credit limit is the maximum amount of money a lender allows you to borrow on a revolving accountmost commonly a credit card or line of creditat any one time.

Example: If your credit card has a $5,000 limit, that means you can carry up to $5,000 in purchases, balance transfers, and cash advances (depending on your card’s terms) before the bank either declines new transactions or potentially charges an over-the-limit fee.

You’ll usually see your limit when you’re approved for an account and on your monthly statements or mobile app. It’s not a suggestion; it’s a hard cap.

Revolving Credit vs. Installment Loans

Credit limits apply primarily to revolving credit, like:

- Credit cards

- Personal lines of credit

- Home equity lines of credit (HELOCs)

With revolving credit, you can borrow, pay it down, and borrow againup to your limit.

Installment loans (like car loans, student loans, or mortgages) don’t have a “credit limit” in the same sense. Instead, you borrow a fixed amount up front and repay it over time in set installments. The concept is related, but the vocabulary is different.

How Credit Limits Work in Real Life

Using Your Credit Limit

Every time you use your card, your available credit shrinks by that amount. If your limit is $3,000 and your balance is $600, you have $2,400 in available credit left. Pay off $400 and your available credit goes back up to $2,800.

So your limit is like the ceiling, and your current balance tells you how close you are to bumping your head.

Going Over Your Limit

What happens if you try to go over?

- Your transaction might be declined, especially if it would push your balance significantly over your limit.

- Some issuers may approve small over-limit charges, but they can charge fees or adjust your account terms when that happens, depending on your agreement and local rules.

Even if your bank quietly allows it, regularly flirting with your limit is not a good look to future lendersand your credit score may pay the price.

How Lenders Decide Your Credit Limit

Lenders don’t pick your limit out of a hat. They look at your overall financial picture and try to answer one question: How much can we safely lend this person without losing sleep?

Key Factors Lenders Consider

-

Credit history and payment habits

Issuers look at your credit reports to see how you’ve handled debt in the past: on-time payments, late payments, collections, and how long you’ve been using credit. A long history of responsible borrowing usually leads to higher limits. -

Credit score

Your credit score is basically your financial “GPA.” A higher score generally signals lower risk, which can qualify you for a higher credit limitespecially on unsecured cards. -

Income

Lenders usually ask about your annual income because it speaks to your ability to pay what you borrow. Higher and more stable income can support higher limits. -

Existing debt and debt-to-income ratio (DTI)

If you’re already juggling lots of loans or card balances, a bank may think twice before giving you a big new limit. They’ll often look at how much of your income already goes toward debt payments. -

Type of account

Secured credit cards (where you put down a deposit) often start with limits equal to your deposit. Unsecured cards rely more on your credit profile and income. Business and premium rewards cards may come with higher limits but stricter requirements. -

Lender’s own policies

Each bank has its own risk models, internal limits per customer, and rules (like maximum total exposure across all cards), so your limit can vary a lot from one issuer to anothereven with the same income and credit score.

Why Your Credit Limit Matters for Your Credit Score

Your credit limit doesn’t just determine how much you can spendit directly affects your credit utilization ratio, which is a big factor in your credit score.

Credit utilization = your current card balance ÷ your total credit limits.

Example: If you have one card with a $4,000 limit and a $1,000 balance, your utilization is 25%.

Most experts and credit bureaus recommend keeping your utilization below about 30%, and often even lowerideally under 10%if you’re trying to look especially attractive to lenders.

Here’s why that matters:

- High utilization can signal that you’re relying heavily on credit and might be at higher risk of missing payments.

- Lower utilization tells lenders you’re using credit, but not depending on it to survive.

- Your utilization is recalculated each time your card issuer reports to the credit bureausoften monthlyso your score can move up or down quickly based on your current balances.

When your credit limit goes up but your spending stays the same, your utilization drops, which can help your credit score. When your limit goes downor your spending spikesyour utilization rises, which may drag your score down.

How Credit Limits Can Change Over Time

Your initial limit is not forever. Lenders can adjust it based on your behavior and financial changes.

Credit Limit Increases

Banks may offer automatic credit limit increases when you’ve:

- Used your card regularly

- Paid on time consistently

- Kept balances relatively low compared to your limit

You can also request a credit limit increase. The lender might run either a:

- Soft inquiry, which doesn’t affect your credit score; or

- Hard inquiry, which may temporarily ding your score by a few points.

Many issuers explain in advance whether an increase request will trigger a hard or soft inquiry, so it’s worth checking before you click “Submit.”

Credit Limit Decreases

Lenders can also reduce your limit if they see risk signals, such as:

- Consistently high balances or maxed-out cards

- Missed or late payments

- Negative information on your credit report

- Long periods of inactivity on the card

A lower limit reduces your available credit and may increase your utilization overnighteven if you didn’t spend a dollarso it can impact your score.

On the flip side, you can ask for a lower limit if a big number is too tempting, or if you just want a smaller credit line for budgeting purposes.

How to Request a Credit Limit Increase (or Decrease)

Most major issuers make this pretty simple. You can usually:

- Log into your online banking or card app and look for “Credit limit” or “Manage credit limit,” or

- Call the number on the back of your card and talk to a representative.

You’ll often be asked to confirm:

- Your current income

- Your housing costs (rent/mortgage)

- Your employment status

Lenders may use that updated information, combined with your credit history, to decide whether to approve the change and by how much.

When a Higher Limit Makes Sense

Requesting a higher credit limit can be smart if:

- Your income has increased since you opened the card.

- Your credit score has improved.

- You want to lower your credit utilization without opening more cards.

- You regularly put large, planned expenses on the card but pay them off.

When a Lower Limit Might Be Better

Reducing your limit could be a good idea if:

- You tend to overspend when a big limit is staring at you.

- You want to limit potential fraud exposure.

- You’re trying to keep your total available credit lower before a specific loan application and you know your spending is modest.

Just remember: a lower limit can raise your utilization if your spending doesn’t drop, so you’ll want to adjust your habits alongside the change.

Common Myths About Credit Limits

Myth 1: “Having a high limit is always bad.”

A high limit can be risky if you treat it like free money. But if you keep your spending under control, a higher limit can actually help your credit score by lowering your utilization. The key is behavior, not the number itself.

Myth 2: “You have to carry a balance to keep your limit.”

Nope. You don’t need to carry a balanceor pay interestto keep your account active or your limit intact. Using the card occasionally and paying in full is usually enough. In fact, carrying a large balance can hurt your credit and cost you money in interest.

Myth 3: “Going slightly over your limit is no big deal.”

Even a small over-the-limit charge can lead to declined transactions, fees, or a limit decrease later. It may also be a sign that your budget needs some attention. Better to avoid hitting the ceiling in the first place.

Smart Ways to Manage Your Credit Limit

- Keep your utilization low. Aim to use less than 30% of your total limits, and lower if you’re about to apply for a major loan.

- Set alerts. Most apps let you set balance or spending alerts so you don’t accidentally creep too close to your limit.

- Make multiple payments. Paying down your balance mid-cycle can keep your reported utilization lower.

- Match your limit to your habits. If you’re a disciplined spender, a higher limit can work in your favor. If you know you’re tempted, a moderate limit plus a strict budget may be safer.

- Review your accounts regularly. Check your statements and your credit reports to make sure everything is accurate and no surprise changes have been made to your limits.

Real-Life Experiences and Lessons About Credit Limits

Numbers are helpful, but credit limits start to make real sense when you see how they play out in everyday life. Here are a few “I’ve been there” style examples that might sound familiar.

Case 1: The Surprise Score Drop After a Vacation

Alex has a $6,000 limit on a travel rewards card and usually keeps the balance under $1,000. One month, a big vacation hits: plane tickets, hotel, rental car, mealsthe card balance jumps to $4,500. Alex still plans to pay it off before interest, but when the credit report updates, the utilization shoots to 75% on that card.

Result? The credit score dips noticeably, even though Alex has never missed a payment. This isn’t a punishment; it’s simply the scoring model reacting to the higher short-term risk of a big balance relative to the limit. Once that balance is paid down, the score usually rebounds. The lesson: you can be responsible and still see temporary score swings when your utilization spikes. Planning extra payments before the statement date can help keep those swings smaller.

Case 2: The Quiet Credit Limit Increase

Jordan opened a beginner cash-back card two years ago with a $1,000 limit. At the time, that felt huge. Jordan used the card for groceries and gas, paid on time every month, and rarely let the balance go above $300. One day, an email arrives: “Congratulations! We’ve increased your credit limit to $3,000.”

Nothing about Jordan’s daily life changed, but behind the scenes, the bank saw a strong payment history, stable usage, and a higher reported income on a recent update. Jordan’s utilization instantly dropped even further, which helped the credit score a bit. The key takeaway: quiet, boring consistencysmall purchases, on-time paymentsoften leads to bigger limits without you even asking.

Case 3: Lowering the Limit to Protect a Budget

Sam is working on getting out of debt and tends to overspend when the available credit is high. Their card has a $10,000 limit, but Sam never needs that much. After a few months of slipping into old habits, Sam calls the issuer and asks to reduce the limit to $3,000.

That lower limit forces Sam to be more intentional about purchases. It also means Sam has to keep an eye on utilizationusing $1,500 of a $3,000 limit (50%) looks riskier than using $1,500 of a $10,000 limit (15%). But for Sam’s mental health and budgeting, the trade-off is worth it. The experience shows that “best for your score” is not always the same as “best for your behavior.” Sometimes, designing your environment so you can’t easily overspend is the smarter long-term move.

Case 4: Asking for a Limit Increase Before a Big Purchase

Taylor wants to renovate a home office and plans to buy furniture and tech using a rewards card, then pay it off over the next few months. The total cost will be around $2,500, but Taylor’s current limit is $3,000, which would push utilization uncomfortably high and risk hurting the credit score right before applying for an auto loan.

So Taylor requests a credit limit increase. The issuer does a soft inquiry, sees good income and strong history, and bumps the limit to $7,000. Now that same $2,500 project represents about 36% utilization instead of over 80%. Taylor still has to manage payments carefully, but the higher limit helps preserve the credit score while earning rewards. The big takeaway: timing matters. If you know a large purchase is coming and you can handle it responsibly, a higher limit requested in advance can reduce the impact on your score.

Case 5: Learning the Hard Way About Maxing Out

Casey once assumed that if the bank gave a $5,000 limit, it meant it was completely fine to use all of it. Over a few months, the balance climbed close to $5,000 and stayed there. Minimum payments kept the account technically “current,” but the utilization sat near 100% the entire time.

When Casey checked a credit score, it was much lower than expected. The score wasn’t reacting to the limit itselfit was reacting to the high utilization and the risk signal that Casey might be stretched thin. It took time, higher payments, and some careful budgeting to dig out. The experience underlined a crucial truth: your credit limit is not a goal; it’s the outer fence. Healthy use usually means staying well inside that fence and paying attention to what your balance looks like when the bank reports it.

All of these examples share one theme: your behavior around your credit limit matters more than the number printed on your statement. Knowing how your limit is set, how it affects your score, and how to ask for changes puts you in controlrather than letting the card control you.

The Bottom Line

Your credit limit is simply the maximum amount a lender is comfortable letting you borrow on a revolving account at one time. But it influences far more than just how much you can spendit affects your credit utilization, your credit score, and even your future borrowing options.

Use it thoughtfully: keep utilization low, ask for increases when your financial situation improves, don’t be afraid to decrease it if you need guardrails, and focus on on-time payments. When you understand how your credit limit works, it stops being a mystery number and starts becoming a tool you can use to build the financial life you want.