Table of Contents >> Show >> Hide

- What Does Rent-to-Own Mean?

- How Does Rent-to-Own Work?

- Lease-Option vs. Lease-Purchase: Same Neighborhood, Different Drama

- Why Do People Choose Rent-to-Own?

- The Biggest Risks of Rent-to-Own

- A Simple Example of a Rent-to-Own Deal

- How to Protect Yourself in a Rent-to-Own Agreement

- When Rent-to-Own Makes Sense

- When Rent-to-Own Is Probably a Bad Idea

- Alternatives to Rent-to-Own

- Final Thoughts

- Experiences Related to Rent-to-Own: What It Feels Like in Real Life

- SEO Tags

Rent-to-own sounds almost magical the first time you hear it. Rent now, buy later, and somehow glide into homeownership without a dramatic movie montage about your credit score. Tempting, right? But like many things in personal finance, the sparkle is real only if you read the fine print with both eyes open.

In the United States, rent-to-own can refer to arrangements for furniture, electronics, and other goods, but when most people ask, “What is rent-to-own?” they usually mean housing. In real estate, it is a deal where you rent a home for a set period while gaining the option, or sometimes the obligation, to buy it later. Some of your money may count toward the purchase. Some of it may not. And that difference matters a lot.

This guide breaks down how rent-to-own homes work, why buyers consider them, what can go wrong, and how to decide whether this path to homeownership is a smart move or just a well-dressed financial headache.

What Does Rent-to-Own Mean?

A rent-to-own agreement is a deal between a tenant and a property owner that combines a lease with a future home purchase opportunity. You move in as a renter, but the agreement includes terms for buying the property later. Think of it as a hybrid: part rental, part potential purchase, part legal document you should absolutely not skim while eating chips.

In many cases, the agreement includes:

- A lease term, often one to three years

- An agreed-upon purchase price, or a formula for setting it later

- An upfront option fee

- A monthly rent amount

- A rent credit provision that may apply part of your payment to the purchase

- Rules about maintenance, taxes, insurance, and deadlines

The basic promise is simple: you rent the home now and get a shot at buying it later. The tricky part is that the contract determines whether that “shot” is flexible, expensive, risky, or all three at once.

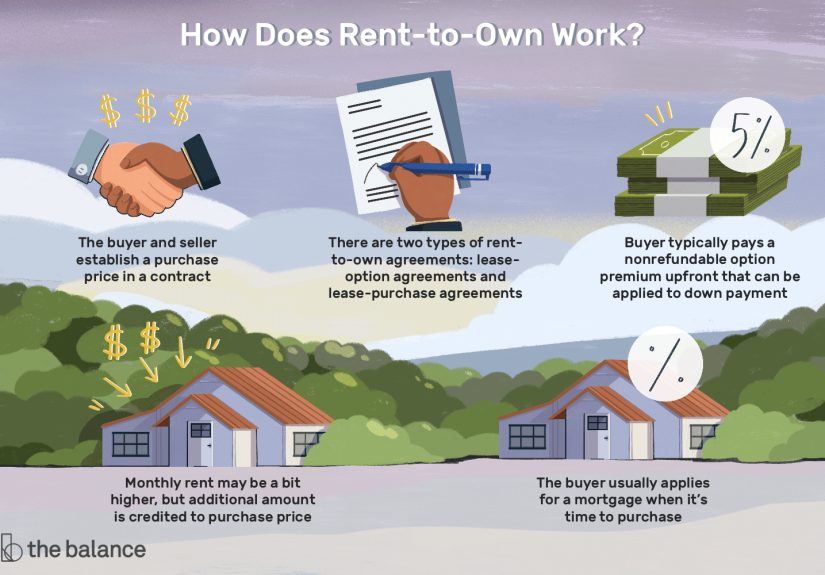

How Does Rent-to-Own Work?

1. You Sign a Lease Plus a Purchase Arrangement

Unlike a standard lease, a rent-to-own contract comes with purchase terms attached. You are not just paying for a place to live. You are also paying for the possibility of ownership down the road.

2. You Usually Pay an Upfront Option Fee

Many rent-to-own deals require an option fee, sometimes called option money. This fee is often nonrefundable. In plain English, that means if you do not end up buying the home, that money may wave goodbye and never come back. Depending on the agreement, the fee may later count toward the purchase price if you complete the deal.

3. Part of Your Rent May Become a Credit

In a classic setup, your monthly payment is a little higher than regular rent because a portion is treated as a rent credit. That credit may go toward your future down payment or purchase price. It sounds helpful, and it can be, but only if the contract clearly says how much is credited, when it applies, and what happens if the sale never closes.

4. You Still Need to Qualify for a Mortgage Later

This is the part many buyers underestimate. A rent-to-own deal does not magically replace mortgage approval. Unless you are paying cash at the end, you still need to qualify for a home loan. That means your income, debt, savings, credit profile, and overall finances still matter when the lease ends.

5. You Buy the Home, or You Don’t

At the end of the lease period, one of two things happens: you purchase the home under the contract terms, or the deal ends. If you do not buy, you may lose your option fee and any rent credits you built up. That is why rent-to-own can feel like a bridge to homeownership or a very expensive life lesson, depending on the outcome.

Lease-Option vs. Lease-Purchase: Same Neighborhood, Different Drama

Not all rent-to-own deals work the same way. The two most common versions are lease-option and lease-purchase.

Lease-Option

A lease-option agreement gives you the right to buy the home later, but not the legal duty to do so. This is the more flexible version. If your finances change, your mortgage falls through, or the home turns out to be a money pit wearing cute shutters, you may be able to walk away. You will likely lose your option fee and credits, but you are generally not forced to buy.

Lease-Purchase

A lease-purchase agreement is stricter. It commits both sides to the future sale. If you cannot get financing when the time comes, you may face serious consequences depending on the contract. This version leaves much less room for a graceful exit.

That distinction is huge. If you remember only one thing from this article, remember this: an option gives flexibility, a purchase agreement adds obligation.

Why Do People Choose Rent-to-Own?

There are a few reasons buyers are drawn to rent-to-own homes, and honestly, some of them make perfect sense.

You Need Time to Improve Your Credit

Maybe your credit score is not disastrous, but it is not exactly mortgage material either. A rent-to-own term can give you time to pay down debt, fix errors on your credit report, build payment history, and look better to lenders later.

You Need More Time to Save

Even with low-down-payment mortgage options, buyers still need cash for down payments, closing costs, moving expenses, inspections, and the hundred tiny home-related purchases that somehow end with you spending $78 on light bulbs and drawer liners. A rent-to-own period can buy time to save.

You Want to Lock in a Home Now

Sometimes a buyer finds a home they love but is not ready to buy immediately. A rent-to-own setup can secure the property before someone else grabs it. If the purchase price is fixed up front and home values rise, that can work in the buyer’s favor.

You Want a Trial Run

Living in a home before buying it gives you something online listings never can: reality. You learn the street noise, the commute, the neighbor with the 6 a.m. leaf blower, and whether the charming old house is actually charming or just drafty with excellent marketing.

The Biggest Risks of Rent-to-Own

Now for the less romantic side of the story.

You Can Lose Money If the Deal Falls Apart

Option fees are often nonrefundable. Rent credits may also disappear if you do not purchase. That means you could spend thousands of dollars for a deal that never becomes ownership.

You Might Still Not Qualify for a Mortgage

A rent-to-own agreement does not guarantee mortgage approval later. If rates rise, your debt grows, your income changes, or lending standards tighten, you may hit the finish line and still not get the loan.

The Home Could Be Overpriced

If the agreed purchase price is too high compared with future market value, you may end up overpaying. That can leave you underwater, meaning you owe more than the home is worth. Not ideal. Very not ideal.

Repairs and Maintenance Can Shift to You

Some agreements put maintenance, insurance, taxes, or repair costs on the tenant-buyer. That means you could be paying renter-style monthly costs while handling owner-style responsibilities, even before you officially own the property.

Title Problems and Liens Can Wreck the Deal

If the seller does not actually have clean title, or if there are liens or an existing mortgage problem, your future purchase can become messy fast. In some risky alternative financing setups, buyers make payments for years without holding legal title.

Scams Exist

Rent-to-own attracts plenty of legitimate sellers, but it also attracts scammers who love upfront fees almost as much as they love disappearing. If someone pressures you to wire money, refuses documentation, or wants you to skip professional review, that is not a “fast-moving opportunity.” That is a red flag wearing dress shoes.

A Simple Example of a Rent-to-Own Deal

Suppose a home is priced at $300,000.

- Option fee: 3% of the price = $9,000

- Monthly rent: $2,200

- Monthly rent credit: $300

- Lease term: 24 months

After two years, your rent credits add up to $7,200. If your option fee also applies toward the purchase, you may have $16,200 credited toward the home.

That sounds great, but here is the catch: you still need to qualify for a mortgage for the remaining amount, and you may still owe closing costs. If you cannot buy, you may lose much or all of the extra money you put in.

How to Protect Yourself in a Rent-to-Own Agreement

Read Every Clause Like It Owes You Money

Because it might. Make sure the agreement clearly states:

- The purchase price or pricing formula

- The exact option fee

- Whether the option fee is refundable

- How much rent is credited

- Who handles repairs, taxes, insurance, and maintenance

- What happens if a payment is late

- What happens if you cannot get financing

- When and how you must exercise the purchase option

Verify Ownership and Order a Title Search

Confirm that the seller actually owns the property and can legally sell it. A title report can reveal liens, ownership issues, or other problems hiding behind a nice front porch.

Get a Home Inspection

Do not skip the inspection because you are “only renting for now.” If you are seriously considering ownership, inspect the place like a buyer. Roofs, HVAC systems, plumbing, and foundations do not care about your optimism.

Talk to a Real Estate Attorney

This is one of those moments where paying for professional help can save you much more later. A real estate attorney can explain obligations, spot abusive terms, and help you negotiate clearer language.

Work With a HUD-Approved Housing Counselor

If your goal is homeownership, a HUD-approved housing counselor can help you assess your credit, budget, affordability, and readiness to qualify for a mortgage. Many counseling services are low-cost or free, and they can also point you toward down payment assistance and first-time buyer programs.

When Rent-to-Own Makes Sense

Rent-to-own can make sense when all of the following are true:

- You are close to mortgage-ready but need more time

- You have stable income and a realistic savings plan

- The contract is transparent and professionally reviewed

- The home is fairly priced

- You understand exactly what money is at risk

- You genuinely want that specific home, not just any home someday

In other words, rent-to-own works best as a strategic bridge, not a desperate leap.

When Rent-to-Own Is Probably a Bad Idea

Step back if:

- You cannot reasonably expect to qualify for a mortgage within the lease term

- You do not have emergency savings

- The seller resists inspection, title review, or attorney involvement

- The contract is vague, rushed, or packed with penalties

- The monthly payment already strains your budget

Sometimes the smartest homebuying move is not buying yet. Not glamorous, but very financially attractive.

Alternatives to Rent-to-Own

Before signing a rent-to-own contract, compare it with other paths to homeownership.

- FHA loans: Some buyers may qualify with down payments as low as 3.5%.

- State and local assistance programs: Many areas offer help with down payments or closing costs.

- Traditional renting while you save: Sometimes boring is beautiful.

- Credit counseling and pre-purchase counseling: These can improve your chances of getting a safer mortgage later.

A rent-to-own agreement is not the only back door into homeownership. Sometimes the front door is just a few months of planning away.

Final Thoughts

So, what is rent-to-own? It is a housing arrangement that lets you rent a property now with the option, or obligation, to buy it later. For some buyers, it can be a practical way to build time, save money, and prepare for a mortgage. For others, it can turn into an expensive detour filled with lost fees, repair costs, contract traps, and shattered expectations.

The key is not whether rent-to-own sounds clever. It is whether the numbers, the contract, the home, and your financial reality all line up. If they do, rent-to-own may be a useful step toward homeownership. If they do not, the best move may be to keep renting, strengthen your finances, and come back to buying when the timing is truly on your side.

Because in real estate, hope is nice. But hope plus due diligence is a much better deal.

Experiences Related to Rent-to-Own: What It Feels Like in Real Life

On paper, rent-to-own looks tidy. In real life, it often feels emotional, hopeful, and a little nerve-racking. Many people are drawn to it because they are close to buying, but not quite there. They may have decent income but weak credit, enough rent money but not enough cash for a down payment, or a strong desire to stop moving from lease to lease. Rent-to-own can feel like finally getting a foot in the door instead of staring through the window.

One common experience is relief at the beginning. A buyer finds a house in a neighborhood they love, signs the agreement, and feels like progress is finally happening. They start painting bedrooms in their mind before they have even bought a paint sample. That emotional shift is powerful. The home stops feeling temporary. Even though they are still renters legally, they begin living like future owners. That can be motivating. It can also make people less objective than they should be.

Another frequent experience is budget pressure. Buyers often discover that rent-to-own is not cheaper than regular renting. In fact, it is usually more expensive month to month. There is the higher rent, the option fee, possible repair responsibilities, and the quiet realization that the future mortgage still has to be affordable too. People sometimes say the arrangement helped them become disciplined savers. Others say it felt like trying to jog uphill while carrying groceries.

There is also the strange middle-ground feeling of responsibility without full control. In many rent-to-own situations, the tenant-buyer starts caring about the property like an owner but does not yet have the legal protections or final authority of one. If the roof leaks, emotions rise quickly. If the furnace groans like it is auditioning for a horror movie, the question becomes: who pays? That gray area can create stress, especially when the contract is vague.

For buyers who succeed, the experience can be deeply satisfying. They use the lease term to pay off debt, correct credit report mistakes, build savings, and prepare for underwriting. By the time the purchase date arrives, they are not just hoping to qualify for a mortgage. They are ready. In those cases, rent-to-own can feel like a structured runway into ownership.

For buyers who do not succeed, the hardest part is often not just the lost money. It is the lost momentum. Walking away from a home you pictured as yours can sting. Losing an option fee or rent credits makes it worse. That is why the strongest real-world lesson is simple: treat rent-to-own like a serious purchase strategy, not a casual rental with a fun bonus feature.

The people who tend to have the best experiences are the ones who go in with a plan. They know their credit score, understand their budget, talk to a lender early, review the contract with a professional, and keep one eye on the dream and the other on the math. That combination may not be glamorous, but it is usually what turns rent-to-own from a risky gamble into a workable path.