Table of Contents >> Show >> Hide

- What “underfunded” actually means

- First, split the pension world into three buckets

- What usually happens to underfunded private-sector pensions

- So are private pension retirees safe?

- Why multiemployer pensions looked terrifying, and why many are not falling apart right now

- Public pensions are the big slow-moving story

- Will retirees lose benefits?

- Who ultimately pays for underfunding?

- What workers and retirees should do now

- What this looks like in real life: common experiences with underfunded pensions

- The bottom line

Underfunded pensions sound like one of those phrases designed to make normal people suddenly want a nap. Unfortunately, the topic matters a lot, because it sits at the intersection of retirement security, public budgets, corporate balance sheets, and the universal human desire to not eat instant noodles at age 78.

So what is going to happen to all the underfunded pensions? The honest answer is: not one single thing. Some will recover slowly. Some will be frozen. Some will be rescued by insurance programs or federal aid. Some will keep paying benefits for decades while governments and employers chip away at the shortfall. And a smaller number will end in painful benefit reductions, higher taxpayer costs, or both.

The key is that “underfunded pension” is not a single category. A private pension at a manufacturing company, a multiemployer union pension in construction or trucking, and a state teacher retirement system do not live under the same rules. They do not have the same safety net. And they definitely do not panic in the same way.

If you want the short version, here it is: most underfunded pensions are not about to vanish into a puff of actuarial smoke. But many of them will become more expensive, more restricted, and more politically contested. In other words, the pension promise usually survives, but the path to honoring it can get ugly.

What “underfunded” actually means

A pension is underfunded when the assets set aside to pay future benefits are less than the value of the benefits already promised. Think of it as planning a giant retirement banquet, sending out all the invitations, and then realizing halfway through the shopping trip that the budget only covers breadsticks and hope.

Underfunding does not automatically mean immediate failure. Pension plans are long-term systems. They collect contributions, invest assets, and pay benefits over decades. A plan can be underfunded and still keep paying retirees on schedule for a very long time. The real question is whether the sponsor has enough money, discipline, and political will to close the gap before the gap becomes the whole story.

That gap usually shows up because of some messy combination of weak investment returns, skipped or insufficient employer contributions, overly optimistic assumptions, rising life expectancy, generous benefit expansions from earlier eras, or simple demographic math. If a plan has lots of retirees and fewer active workers paying in, it gets harder to invest its way out of trouble.

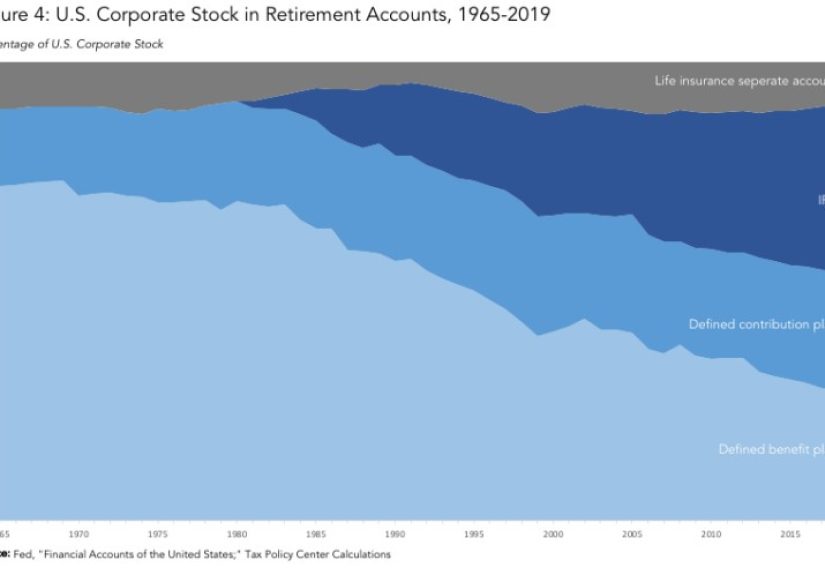

First, split the pension world into three buckets

1. Private single-employer pensions

These are traditional defined benefit pensions sponsored by one company or a related group of companies. They are most common in legacy industries and large established firms. If these plans fail, they may fall under the protection of the Pension Benefit Guaranty Corporation, or PBGC.

2. Multiemployer pensions

These plans are collectively bargained arrangements involving multiple employers and usually a union, often in industries where workers move among employers, such as construction, transportation, and hospitality. They have their own PBGC insurance program and their own headaches.

3. State and local public pensions

These cover teachers, police officers, firefighters, and other state and local workers. They are not insured by PBGC. That is a huge difference. If public pensions are underfunded, the backstop is not a federal pension insurer. It is usually a mix of taxpayers, government employers, employees, negotiated reforms, and legal constraints.

What usually happens to underfunded private-sector pensions

In the private sector, underfunded single-employer pensions tend to follow one of several familiar paths.

The most boring outcome: the sponsor pays more

Sometimes the employer simply increases contributions and keeps the plan alive. This is the least dramatic option and the one retirees would vote for if pension policy were run like a game show. Stronger funding rules, premium costs, and regulatory oversight push companies to address shortfalls rather than pretend they are a future executive’s problem.

The very common outcome: the plan freezes

A frozen pension still pays benefits that workers already earned, but it stops building additional benefits for current workers or closes the plan to new hires. This is one of the main ways companies reduce risk without taking away accrued benefits. It is the corporate version of saying, “We still love tradition, just not enough to keep adding to it.”

The finance-heavy outcome: risk transfer

Some sponsors buy annuities from insurers for retirees or shift chunks of pension obligations off their books. That does not mean retirees necessarily lose benefits, but it does mean the promise changes hands. The company is trying to get out of the pension babysitting business and let an insurer handle the midnight feeding schedule.

The hard outcome: distress termination and PBGC takeover

If a company cannot support the plan and meets legal conditions, the plan may terminate without enough assets to pay all promised benefits. In that case, PBGC steps in for insured private defined benefit plans and pays guaranteed benefits up to legal limits.

This is the part many workers misunderstand. PBGC is a major safety net, but it is not a magical clone of the original plan. It guarantees basic pension benefits subject to legal limits. People with very large promised benefits, certain recent benefit increases, or certain early retirement features may receive less than what the plan originally projected.

That is why underfunded private pensions do not usually end in “everything is gone,” but they also do not always end in “nothing changes.” The most likely result is partial protection, not perfect restoration.

So are private pension retirees safe?

Safer than many headlines suggest, but not invincible.

If you are in an insured single-employer plan, PBGC protection matters a lot. It keeps many retirees from falling into a total-benefit cliff if the employer collapses. Still, the guarantee has limits, and those limits depend on age and payment form. Someone retiring earlier, choosing a survivor option, or receiving a benefit above the guarantee ceiling can be more exposed than they expected.

In plain English: the floor is real, but the floor may sit lower than your original promised payout.

Why multiemployer pensions looked terrifying, and why many are not falling apart right now

Multiemployer pensions were once the scariest corner of the pension map. Many of these plans were battered by industry decline, shrinking employer bases, aging participants, and long-running funding stress. For years, the fear was not just that individual plans would fail, but that the PBGC’s multiemployer insurance program itself would run out of money.

Then came a major policy shift. The American Rescue Plan created Special Financial Assistance, giving severely troubled eligible multiemployer plans a federal lifeline designed to help them pay full benefits through 2051. That changed the immediate story dramatically. For many workers and retirees in these plans, the near-term future went from possible benefit cuts to breathing room.

That does not mean the multiemployer problem has been “solved forever.” It means a specific disaster scenario was delayed or prevented for a large group of plans. Long-term structural issues still exist. Investment risk still exists. Demographic pressure still exists. And 2051 is not the same as “no one will ever need another pension policy debate again.” Washington loves a sequel.

Another wrinkle: PBGC’s multiemployer guarantee is much less generous than many people assume. If a multiemployer plan becomes insolvent outside the rescue framework, the guaranteed benefit is tied to a formula based on years of service and benefit rate, not a lush replacement of the full pension. So the rescue mattered because the underlying guarantee is modest compared with the single-employer system.

Public pensions are the big slow-moving story

When people ask what will happen to underfunded pensions, they are often really asking about public pensions. That is because the numbers are huge, the plans cover millions of workers, and the consequences spill directly into taxes, public services, and labor politics.

Public pensions usually do not implode overnight. They grind. They negotiate. They restructure. They ask for more money. They lower assumptions. They change amortization schedules. They redesign benefits for new hires. They fight in court. They make local politicians discover the word “actuarial” and immediately regret it.

The broad direction in recent years has actually been mixed-to-better, not apocalyptic. Many public systems improved funding after stronger contributions, better discipline, and favorable markets. Several states made supplemental payments, tightened funding policy, and worked to pay pension debt down more systematically.

But improvement at the national level does not erase the weak spots. Some states and localities remain deeply burdened, especially where officials underpaid into plans for years or where pension debt is enormous relative to revenue. In those places, underfunding usually leads to one of four things: higher employer contributions, more taxpayer pressure, changes for future workers, or reduced flexibility in the budget for everything else.

What public plans usually do instead of collapsing

They repair slowly. Common steps include:

- raising government contributions year after year;

- requiring workers to contribute more;

- reducing assumed investment returns to make funding math more realistic;

- changing benefits for new hires, such as later retirement ages or different formulas;

- limiting or revising cost-of-living adjustments in jurisdictions where that is legally allowed;

- stretching out the payoff period for pension debt, which helps today’s budget but can cost more later.

The crucial point is that public pension underfunding usually becomes a fiscal management problem before it becomes a check-stopped-arriving problem. Retirees often continue receiving benefits while governments fight over who pays more to keep the promise credible.

Will retirees lose benefits?

Sometimes, but the answer depends heavily on the pension type and the legal protections involved.

For private single-employer pensions, retirees can lose part of what they expected if PBGC guarantees do not fully cover the promised amount. For multiemployer plans, the rescue framework greatly reduced the risk of near-term cuts in many troubled plans, but the guarantee without rescue is still limited.

For public pensions, accrued benefits for current workers and retirees are often legally protected, sometimes strongly. But “protected” does not always mean every feature is untouchable in every state. Cost-of-living adjustments, future accruals, retirement age rules, employee contributions, and benefits for new hires can all become battlegrounds depending on state law and court rulings.

That means the most common losers are not always current retirees. Often the pressure shifts to taxpayers, younger workers, or future employees who get less generous plans than the people who came before them.

Who ultimately pays for underfunding?

Here is the uncomfortable part: pension underfunding rarely disappears. It gets transferred.

Sometimes shareholders pay, because a company must contribute more cash or face distress. Sometimes taxpayers pay through larger public contributions. Sometimes workers pay through higher payroll deductions or reduced future benefits. Sometimes retirees pay through trimmed features or lower-than-expected payouts after plan failure. Sometimes public services pay because money that might have funded schools, roads, or staffing gets diverted to pension debt instead.

In other words, underfunded pensions are less like a vanishing trick and more like a hot potato. Somebody almost always catches it.

What workers and retirees should do now

If you are covered by a pension, this is not the moment for panic. It is the moment for paperwork and attention. Read the annual funding notice if your plan sends one. Confirm whether your plan is private single-employer, multiemployer, or public. Check whether your plan has been frozen, restructured, or placed in critical or endangered status. Understand what part of your benefit is already accrued and whether there are COLA rules that matter to you.

Also, never assume “pension” means “fully safe no matter what.” That idea belongs in the same museum exhibit as floppy disks and office fax machines. A pension can still be valuable and worth trusting more than a lot of retirement alternatives, but blind faith is not a funding policy.

If you are close to retirement, get your estimated benefit in writing, understand survivor options, and learn what backstop exists for your plan type. If you are a public worker, watch contribution policy and legal changes. If you are in a private plan, learn PBGC basics. If you are in a multiemployer plan, learn whether your plan has already received or may receive Special Financial Assistance.

What this looks like in real life: common experiences with underfunded pensions

The numbers matter, but pensions are ultimately personal. Underfunding does not feel like a spreadsheet to the people living through it. It feels like uncertainty showing up at the kitchen table and asking for coffee.

Consider a retired factory worker in a private single-employer plan. He spent thirty years assuming the pension estimate in his folder was basically a contract with gravity. Then the company weakens, files for bankruptcy, and the plan lands with PBGC. His benefit does not disappear, which is a huge relief, but it may not match the original promise exactly. He starts asking new questions he never thought he would need to ask in retirement: Should I delay a home repair? Can I still help a grandchild with tuition? Do I really need streaming services, or is old-fashioned boredom about to become a budgeting strategy?

Now picture a mid-career public school teacher. Her pension is not failing tomorrow, but headlines about underfunding and rising contribution costs become part of every state budget debate. She keeps working. Her accrued benefit is probably better protected than internet doom-posters admit. But she notices new hires getting a less generous tier. She hears talk about changing retirement age assumptions and tightening COLA rules. The pension still exists, but it no longer feels like a stone tablet carved on a mountain. It feels like a promise protected by lawyers, payroll deductions, and annual legislative drama.

Then there is the construction worker in a multiemployer plan. For years, he hears that the plan is in trouble and that cuts could eventually hit. Retirement planning starts to feel like building a deck during a thunderstorm. Then federal Special Financial Assistance changes the immediate outlook. Suddenly the conversation shifts from “Will the plan make it?” to “How long does this fix really last?” That is still stressful, but it is a different kind of stress. One is a fire alarm. The other is a weather forecast.

There is also the city budget director, who probably deserves stronger coffee than everyone else. She is not receiving a pension yet, but she is staring at an annual contribution bill that keeps climbing. Every extra dollar sent to close pension debt is a dollar not spent somewhere else. She is not deciding whether pensions matter. She is deciding which other priorities must stand in the hallway while pensions get seated at the table first.

And do not forget the adult children of retirees. Pension uncertainty often lands on families before it lands on policy experts. When a parent worries that a check could shrink, the backup plan is not an abstract federal agency. It is usually family budgeting, caregiving, shared housing, delayed retirement by younger relatives, or a long string of “We’ll figure it out.”

That is why underfunded pensions are never just about finance. They shape when people retire, where they live, whether they can age independently, how much risk families absorb, and how communities allocate public money. The experience is usually not one giant collapse. It is a long negotiation with reality.

The bottom line

Most underfunded pensions are not headed for sudden extinction. The more likely future is uneven and complicated. Private plans will keep freezing, terminating, or de-risking, with PBGC serving as a meaningful but limited backstop. Multiemployer plans have gained critical time because of federal rescue money, though long-term questions remain. Public pensions will mostly keep moving through a slow repair cycle of higher contributions, policy changes, and political fights over who absorbs the cost.

So what is going to happen to all the underfunded pensions? They are going to be paid for, reworked, rescued, trimmed at the edges, argued over in courtrooms and legislatures, and watched anxiously by millions of workers and retirees. Some promises will be honored exactly. Some will be honored imperfectly. Some will be made more expensive than anyone wanted to admit twenty years ago.

That may not be a tidy ending, but it is the honest one. Underfunded pensions do not usually die in one dramatic scene. They live on through restructuring, subsidies, discipline, compromise, and the stubborn refusal of retirement promises to disappear just because the math got uncomfortable.

Note: This article is for informational purposes only and reflects current U.S. pension policy and funding trends as of March 2026. It is not legal, tax, or investment advice.