Table of Contents >> Show >> Hide

- The Simple Rule: VC Ownership Is Driven by Fund Math

- Typical VC Ownership Targets by Funding Stage

- The Formula: Investment Divided by Post-Money Valuation

- Why Bigger VC Funds Usually Want More Ownership

- Ownership Is Not the Same as Control

- The Option Pool Shuffle: The Sneaky Dilution Guest

- SAFEs and Convertible Notes Can Change the Real Ownership Picture

- How Much Dilution Is “Normal”?

- What Founders Should Aim to Keep

- Specific Example: A Clean SaaS Cap Table

- What Venture Capitalists Really Want Besides Percentage Ownership

- How Founders Can Negotiate VC Ownership Without Sounding Naive

- Field Notes: Founder Experiences With VC Ownership

- Conclusion: So, What Percentage Ownership Do VCs Want?

Ask a founder what venture capitalists want, and you may hear: “traction, a giant market, clean metrics, and possibly my firstborn dashboard.” But underneath the pitch decks, partner meetings, and polite coffee chats, VCs are usually solving one very practical equation: how much ownership can this fund get for the check it writes?

In plain American English: most venture capitalists do not invest just to “support innovation.” They invest because they need a small number of companies to return a very large amount of money to their fund. That means ownership matters. A lot. If a VC owns too little of a winning startup, even a great exit may not move the fund. If they own too much, founders may become demotivated, future rounds get messy, and the cap table starts to look like a lasagna made by lawyers.

So, what percentage ownership do venture capitalists want in start-ups? The useful answer is: it depends on the stage, fund size, check size, competition, valuation, and how “must-have” the company looks. The practical answer is usually somewhere between 5% and 25% per institutional round, with many lead investors aiming for 10% to 20%.

The Simple Rule: VC Ownership Is Driven by Fund Math

Venture capital is not magic, although some term sheets do appear after midnight and contain clauses that frighten villagers. VC firms raise money from limited partners, then invest that money into start-ups. Their goal is to return the fund several times over. Because most start-ups do not become massive winners, VCs rely on the few breakout companies to carry the portfolio.

That is why a lead investor often cares about ownership more than founders expect. A $1 billion fund cannot get excited about owning 2% of a company unless the exit potential is enormous. If that company sells for $500 million, 2% equals $10 million before dilution, fees, and fund economics. Nice? Yes. Fund-changing? Not for a billion-dollar fund. Now imagine owning 20% of that same company. That is a different conversation, and the spreadsheet suddenly starts wearing sunglasses.

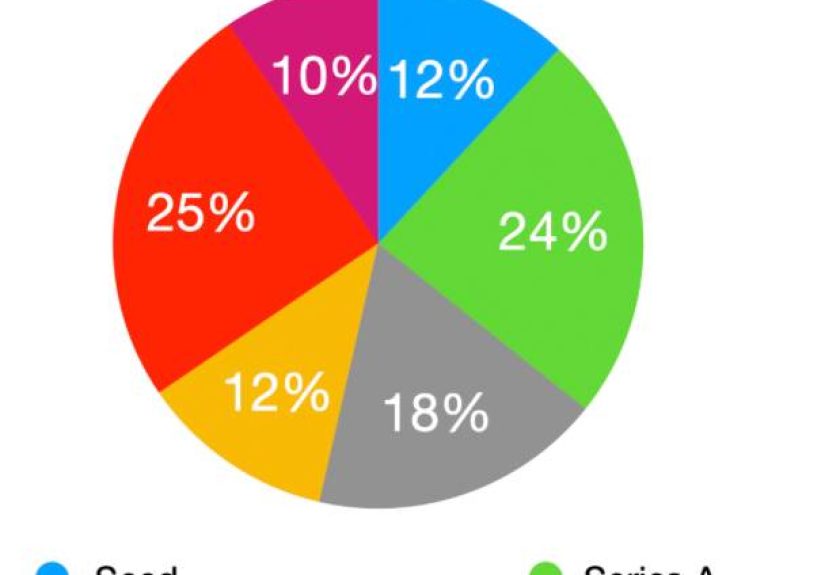

Typical VC Ownership Targets by Funding Stage

There is no universal law saying a VC must own a specific percentage. Still, market patterns are fairly consistent. Founders should think in ranges, not absolutes.

Pre-Seed: 5% to 15%

At pre-seed, the company may have little more than a product idea, a prototype, a few early users, or a founder with frighteningly high caffeine tolerance. Investors at this stage may include angels, micro-VCs, accelerators, and small seed funds.

A small pre-seed investor may be comfortable with 2% to 5%, especially if they are not leading the round. A lead pre-seed fund may target 7% to 10%, and some will push toward 15% if they are writing a meaningful check or taking meaningful risk.

Seed: 10% to 20%

Seed investors commonly want enough ownership to justify hands-on involvement and reserve capital for future rounds. A seed lead often targets around 10%, sometimes 15%, and occasionally more if the round is large relative to the company’s valuation.

For example, if a SaaS start-up raises $2 million at an $8 million pre-money valuation, the post-money valuation is $10 million. The investors collectively receive 20% of the company. If one fund leads with $1.2 million of that round, it may own around 12% before future dilution. That is a very normal early-stage venture outcome.

Series A: 15% to 25%

Series A is often where ownership expectations become more serious. By this point, a venture capitalist wants to see more than “people seem to like us.” For SaaS start-ups, investors usually look for early product-market fit, growing revenue, strong retention, a repeatable sales motion, or at least credible evidence that the business can scale.

Many Series A leads want 15% to 20%. Some larger funds prefer 20% to 25%, especially if they are taking a board seat and writing the majority of the round. In very competitive deals, a hot start-up may sell less ownership because investors are fighting to get in. In colder markets, founders may need to sell more equity to raise the same amount of capital.

Series B and Beyond: 5% to 15%

Later rounds usually involve larger checks, higher valuations, and more existing investors. Series B investors may target 10% to 15%. Series C investors may be comfortable with 5% to 10%, especially when the company is already valuable and the check size is large.

At growth stage, ownership is still important, but the investor may care just as much about dollar deployment, downside protection, liquidation preferences, governance rights, and whether the company is on a credible path toward IPO or acquisition.

The Formula: Investment Divided by Post-Money Valuation

The basic ownership formula is wonderfully simple:

Investor ownership = investment amount ÷ post-money valuation

If a VC invests $5 million at a $20 million pre-money valuation, the post-money valuation is $25 million. The investor receives 20% ownership:

$5 million ÷ $25 million = 20%

Simple, right? Naturally, start-up finance then adds SAFEs, convertible notes, option pools, pro-rata rights, liquidation preferences, and enough definitions of “fully diluted capitalization” to make your browser ask for a vacation.

Why Bigger VC Funds Usually Want More Ownership

A small fund and a mega-fund do not think the same way. A $30 million seed fund can generate an excellent return from owning 5% to 10% of a company that exits for several hundred million dollars. A $1.5 billion multi-stage fund usually needs bigger outcomes and more ownership for the numbers to matter.

This is why founders sometimes hear confusing feedback. One investor says, “We would love to own 7%.” Another says, “We need 20% to lead.” Neither is necessarily being unreasonable. They may simply be managing different fund sizes, portfolio strategies, and return targets.

For founders, this matters because the “right” investor is not always the one offering the highest valuation. A huge fund may offer prestige and deep pockets but may also require a larger ownership stake. A smaller specialist fund may write a smaller check, accept lower ownership, and provide more targeted help. The cap table should match the company’s strategy, not just the founder’s ego during fundraising season.

Ownership Is Not the Same as Control

Founders often focus on percentage ownership, but control is a separate issue. A VC can own 15% and still have major influence through board seats, protective provisions, veto rights, information rights, and pro-rata rights. Preferred stock usually comes with rights that common stock does not have.

That does not mean VC terms are automatically villainous. Investor protections exist because VCs are putting serious capital into risky companies. But founders should understand that selling 20% of the company is not just selling 20% of the economics. It may also change how major decisions are made.

The Option Pool Shuffle: The Sneaky Dilution Guest

One of the most misunderstood parts of VC ownership is the employee option pool. Investors often require start-ups to create or refresh an option pool before a financing closes. This pool is used to hire future employees, especially senior leaders.

Here is the catch: if the option pool is added before the financing, it usually dilutes the founders more than the new investors. For example, a Series A term sheet may say the investor is buying 20% of the company, but also require a 10% post-financing option pool. Depending on how the math is written, founders may feel more dilution than they expected.

This is why founders should model the round on a fully diluted basis. Do not just ask, “What valuation did we get?” Ask, “After the new money, option pool, SAFEs, notes, and existing grants, what do the founders actually own?” That number is the one that matters when the champagne is gone and the spreadsheet remains.

SAFEs and Convertible Notes Can Change the Real Ownership Picture

Many early start-ups raise money with SAFEs or convertible notes before a priced equity round. These instruments are popular because they are faster and simpler than a full priced financing. But they still convert into equity later, and that conversion can surprise founders who did not model dilution carefully.

Post-money SAFEs make the ownership math clearer because the investor’s ownership percentage is tied to the amount invested divided by the post-money valuation cap. For example, a $500,000 SAFE at a $5 million post-money cap effectively represents 10% ownership before later financing dilution.

The danger is stacking too many SAFEs at low caps. One SAFE may be harmless. Five SAFEs can become a cap table confetti cannon. By the time the Series A arrives, founders may discover that they already sold a large portion of the company before the institutional lead even takes its bite.

How Much Dilution Is “Normal”?

A common rule of thumb is that founders may experience around 15% to 25% dilution in a major priced round. Seed and Series A rounds are often near the higher end because investors are taking more risk and the company still needs to build its team. Later rounds may dilute less on a percentage basis because valuations are higher.

But “normal” depends on context. A capital-efficient SaaS company with strong revenue growth may raise at a higher valuation and sell less equity. A start-up with a big vision but little revenue may need to sell more equity to raise the same cash. A company in a hot AI market may command unusually founder-friendly terms. A company raising during a market downturn may need to accept more dilution, stronger investor protections, or both.

What Founders Should Aim to Keep

Founders do not need to own 100% forever. In fact, owning 100% of a company that cannot grow because it lacks capital is not exactly a luxury yacht problem. Still, over-dilution is real. If founders sell too much too early, they may lose motivation, future investors may worry about incentives, and hiring executives with equity may become harder.

As a practical target, founders should try to avoid giving away massive ownership before the company proves meaningful traction. After seed, a founding team may still want to own a majority if possible. After Series A, many strong companies still have founders with a meaningful combined stake. By later stages, founder ownership may fall substantially, but the goal is for the value of the smaller percentage to become much larger.

Specific Example: A Clean SaaS Cap Table

Imagine two founders start with 100%. They reserve 10% for an employee option pool, leaving the founders with 90% on a fully diluted basis.

They raise a seed round where investors buy 15%. After the round, the rough ownership might look like this:

- Founders: 76.5%

- Seed investors: 15%

- Employee option pool: 8.5%

Later, they raise a Series A where the new investor buys 20%, and the option pool is refreshed. After that financing, the simplified ownership might look more like this:

- Founders: 55% to 60%

- Seed investors: 10% to 13%

- Series A investor: 20%

- Employee option pool: 10% to 15%

This is not a universal template, but it shows the central lesson: dilution compounds. Each round reduces everyone’s percentage unless they invest pro rata. That is why founders should not treat early equity as Monopoly money. The orange properties eventually matter.

What Venture Capitalists Really Want Besides Percentage Ownership

Ownership is important, but VCs also evaluate quality. A great investor may accept a lower percentage in an exceptional start-up because the company has unusual momentum. A weak company may offer 30% and still struggle to raise because investors do not want a large slice of a tiny, melting cake.

VCs typically consider:

- Market size: Can this become a very large company?

- Growth rate: Is revenue or usage expanding fast enough?

- Retention: Do customers stay, expand, and love the product?

- Founder quality: Can this team recruit, sell, adapt, and survive chaos?

- Capital efficiency: How much money is needed to reach the next milestone?

- Exit potential: Can the company realistically return venture-scale outcomes?

How Founders Can Negotiate VC Ownership Without Sounding Naive

The best founders do not say, “I refuse dilution.” That sounds like saying, “I want to build a rocket, but I dislike fuel.” Instead, sophisticated founders discuss milestones, round size, valuation, option pool needs, and investor role.

Good questions include:

- What ownership percentage do you need to lead this round?

- Is that target based on your fund model or this specific check size?

- How much of the round do you expect to take?

- Will the option pool increase be pre-money or post-money?

- Do you require a board seat?

- How do you think about pro-rata participation in future rounds?

These questions make founders look prepared, not difficult. Investors respect founders who understand the math. They may not give you everything you want, but at least they will know you did not wander into the term sheet wearing financial flip-flops.

Field Notes: Founder Experiences With VC Ownership

One common founder experience is the shock of discovering that valuation is not the only number that matters. A founder may celebrate a $20 million valuation, then realize the investor wants a large option pool refresh before the financing. On paper, the headline valuation looks great. In practice, the founder’s ownership drops more than expected. The lesson is simple: always model the fully diluted cap table after the round, not just the glamorous number that looks good in a press release.

Another frequent experience is choosing between a higher valuation and a better investor. Suppose one VC offers a $40 million pre-money valuation but wants limited involvement, while another offers $35 million but has deep SaaS operating experience, strong recruiting networks, and a history of helping companies raise Series B. The cheaper money may not be cheaper if the more helpful investor increases the odds of reaching the next milestone. Ownership should be evaluated alongside value-add, not in isolation.

Founders also learn that small early checks can become expensive if they are not managed carefully. A few angel checks on post-money SAFEs may feel harmless when the company is young. But if those SAFEs stack up at low valuation caps, the conversion can absorb a surprising amount of the cap table. The founder who thought they sold “just a little” may later discover that the “little” became a rather chunky raccoon sitting on the Series A.

In SaaS specifically, the best ownership negotiations often come from having clean metrics. If a company can show strong net revenue retention, low churn, efficient customer acquisition, and a credible path from $1 million to $10 million in ARR, investors may compete more aggressively. Competition gives founders leverage. Leverage improves valuation. Better valuation reduces dilution. This is why the best fundraising strategy is usually not clever negotiation language; it is building a business investors are afraid to miss.

Finally, experienced founders understand that dilution is not automatically bad. Selling 20% of a company to hire a world-class team, accelerate product development, and capture a large market can be the right decision. Selling 20% because the company has no plan, no metrics, and no budget discipline is less charming. The difference is whether the capital increases the company’s value faster than it reduces the founder’s percentage. In other words, dilution is acceptable when it buys speed, quality, and probability of success. It is painful when it merely buys time.

Conclusion: So, What Percentage Ownership Do VCs Want?

Most venture capitalists want enough ownership to make the investment meaningful for their fund. For small funds, that may be 5% to 10%. For seed leads, it is often 10% to 15%. For Series A leads, it is commonly 15% to 25%. For later-stage investors, the percentage may drop, but the dollar amount rises.

The founder’s job is not to avoid dilution at all costs. The founder’s job is to sell the right amount of equity to the right investors at the right time, while keeping the company attractive for employees, future investors, and the founding team. Venture capital is a trade: ownership for acceleration. Make sure the acceleration is real.

Note: This article is for educational publishing purposes and should not be treated as legal, tax, or investment advice. Founders should work with qualified startup counsel before signing financing documents.